The bottom line: Consumer inflation surge continues in line with expectations

- The good news and bad news for the May report on consumer inflation can be encapsulated in the headline data: Inflation has surged to a three-year high, but it was no worse than expected.

- The latter provides the slimmest of silver linings as consumers grapple with the shock of soaring gas prices in recent months, adding to a list of goods and services that continue to see steady price hikes that are well above what consumers had become accustomed to prior to the pandemic. Since then, a succession of developments has contributed to a most significant and persistent inflation environment in decades and forced the Fed to attempt to deftly turn its policy knobs to address a very fluid macro backdrop.

- Higher energy prices are the primary catalyst behind elevated inflation today, but they’re certainly not the sole source. Beyond the energy complex, the story becomes much more nuanced though. The Fed’s interpretation of the underlying forces and its best course of action will have investors’ attention heading into next week’s FOMC decision.

By the numbers: Higher, but not unexpectedly so

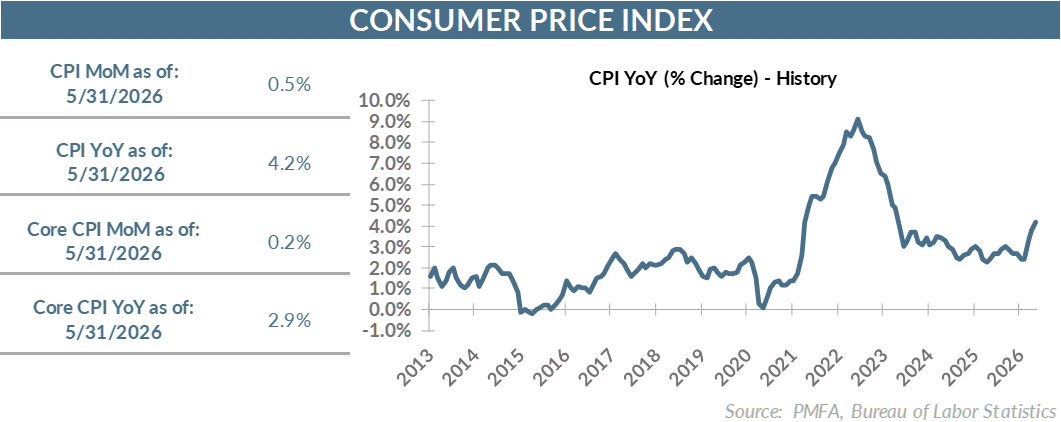

- The consumer price index rose 0.5% in May, which was closely aligned with the consensus forecast coming into the release of the report this morning. Surging energy prices remain a key catalyst behind the recent acceleration in upward price pressures.

- Core CPI, which excludes food and energy, edged up by a much tamer 0.2%, modestly better than the 0.3% forecast.

- Stepping back from the single-month rates of change, the magnitude of the upward push in trailing one-year inflation can’t be missed. Headline CPI popped to 4.2% for the 12 months ended in May, its highest point in over three years, when the economy was working through the impact of the COVID-19 era global inflation surge.

- Core inflation at 2.9% over the past year has been better anchored but still reflects the flowthrough effects of energy-, tariff-, shelter- and wage-related price pressures over the past year.

Broad thoughts: Underlying sources of inflation muddy the picture for the Fed

- The primary catalyst behind the most recent reacceleration in inflation is unquestionably the conflict in the Middle East and the resulting disruption in the flow of crude oil from the region. That’s readily apparent energy prices, which have risen by nearly 24% over the past year.

- Even that sizable increase doesn’t fully reflect what most Americans are feeling though, given the average household’s primary litmus test being prices at the pump. Gasoline prices have soared by over 40% in the past year, with most of that coming since March. That’s challenging already tight spending budgets for many American households.

- There’s still more to the broad inflation story than higher energy costs.

- Shelter inflation — the largest component of the consumer price index and the largest monthly outlay for most families — increased by 3.4% over the past 12 months. That’s certainly better than has been the case over much of the past several years but, given its sizable representation in the CPI, it still puts a sturdy floor under consumer prices.

- Other segments of the service sector are also putting up price increases well above 3%, lifted in part by the tight labor markets of the past several years and the flowthrough effect from solid wage growth.

- That being said, policymakers may find some elements of the report to be more reassuring than alarming. Core goods inflation continues to flatten, edging down by 0.1% in May to just 1.1% over the trailing 12 months. New vehicle prices have flattened, while used vehicle prices have eased over the past year.

- Collectively, the weakening in goods inflation is a positive sign that the worst of the tariff-induced pop in goods prices has filtered through and has, as expected, largely reflected a one-time adjustment rather than a long-term structural source of upward pressure on consumer prices.

- Conversely, shelter inflation picked up moderately last month despite indications from other data sources that rent rates have continued to recede. That should help to tame shelter CPI in due time, but that’s been trickling through the government data more slowly than anticipated.

- What this will mean for both Fed policy and its near-term tone is an open question, particularly as new FOMC Chair Warsh takes the lead on setting the tone emanating from the central bank.

- Certainly, the considerable impact of oil prices could begin to resolve with a sustainable rollback in tensions in the Middle East and the resumption of crude oil flow. Given recent developments, a further flaring in near-term tensions further dim that potential for now.

- The likelihood of a shift in policy in the coming months still seems quite low, but market expectations have increasingly leaned in the direction of a more hawkish Fed later this year.

- The combination of inflation that’s already well above the central bank’s target, and still rising, and the surprising reacceleration in hiring against a low unemployment backdrop is expected to force the Fed’s hand on rates. While still not a foregone conclusion, the futures market is now pricing in a probable rate hike by December by a nearly 2-to-1 margin.

- Boil it all down, and the inflation picture is a muddy one. Surging energy prices have lifted headline inflation to a three-year high; core measures, while better restrained, have also edged higher and remained above the Fed’s stated target.

- Long-term inflation expectations remain well anchored, suggesting that the market still believes that the Fed’s on a reasonable path with the tools and the ability to rein in inflation over time.

- How long will policymakers be willing to stand pat on rates and lean on their collective ability to convey a measured tone on inflation in hopes that other developments and forces will cause inflation to roll over in an acceptable time frame? That’s the question — and one that takes on an additional dimension of uncertainty. That will be a key focus next week as investors parse the FOMC’s policy statement, updated projections, and Chair Warsh’s press conference message.

Past performance does not guarantee future results. All investments include risk and have the potential for loss as well as gain.

Data sources for peer group comparisons, returns, and standard statistical data are provided by the sources referenced and are based on data obtained from recognized statistical services or other sources believed to be reliable. However, some or all of the information has not been verified prior to the analysis, and we do not make any representations as to its accuracy or completeness. Any analysis nonfactual in nature constitutes only current opinions, which are subject to change. Benchmarks or indices are included for information purposes only to reflect the current market environment; no index is a directly tradable investment. There may be instances when consultant opinions regarding any fundamental or quantitative analysis may not agree.

Plante Moran Financial Advisors (PMFA) publishes this update to convey general information about market conditions and not for the purpose of providing investment advice. Investment in any of the companies or sectors mentioned herein may not be appropriate for you. You should consult a representative from PMFA for investment advice regarding your own situation.