The bottom line: Surprise cooldown in nonfarm payrolls should temper expectations, but not be a cause for alarm

- Three consecutive months of solid nonfarm payroll gains had provided some reassurance that the labor economy was emerging from its challenging seesaw pattern of alternating monthly gains and losses that had characterized the labor economy over the preceding year.

- One unexpectedly soft print doesn’t undo that improvement but is a reminder that monthly data on the labor economy can be volatile and is subject to revision.

- The jobs picture probably isn’t as strong as the previously reported job gains intimated, but it’s also likely not as challenging as the June report and its accompanying revisions suggest.

- Further, with inflation pressures set to ease on the back of a sharp reduction in oil prices, consumers are breathing a little easier. That could provide a modest lift in spending and an additional source of support for growth that wasn’t as robust in Q1, which should in turn support hiring in the coming months.

- It’s not a labor economy that’s firing on all cylinders, but that shouldn’t be surprising at this stage of the cycle. Peak hiring is firmly in the rearview mirror, but jobs are still being created at a decent clip, and layoffs are contained in an economy that’s operating at or near full employment.

By the numbers: Soft report ends string of encouraging nonfarm payroll gains

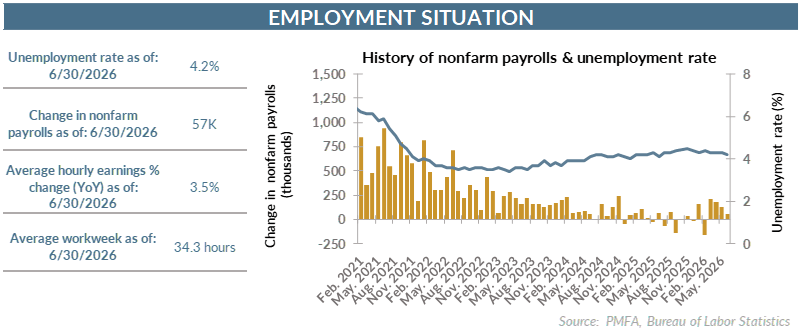

- Nonfarm payrolls increased by a tepid 57,000 in June — roughly half the consensus forecast for a gain of 110,000. The unexpectedly weak report also slashed 74,000 from previously reported job gains for April and May.

- Combined, the lackluster June gain and downward revisions resulted in a net reduction in nonfarm payrolls of 15,000 — hardly what economists were hoping for.

- The unemployment rate edged down to 4.2%, fractionally below the May reading. That’s indicative of an economy that’s still running close to full employment, although it comes with a notable asterisk. Labor force participation dropped by 0.3% to 61.5% in June, suggesting that, at least at the margins, potential workers are quietly dropping out of the labor force.

- Looking beyond the one-month change, data over the past year confirms the trend. Participation has declined by nearly a full percentage point over the past year, with the estimated scale of the workforce shrinking by 720,000 over that period despite an increase of nearly 1.6 million in the pool of potential workers. Absent that reduction in participation, and unemployment would be above 5%.

- Average hourly wages edged higher, rising by 0.3% in June and 3.5% over the past year.

Broad thoughts: Good, not great, hiring backdrop reinforces the case for the Fed to stand pat for now

- The June jobs report is a poignant reminder of the need to step back from shorter-term point in time measures of the economy and focus on trends.

- Without question, reported job gains were disappointing — and exacerbated by large revisions that meaningfully trimmed previously reported gains. Even so, the average gain over the last three months is far from catastrophic, particularly in the context of an economy that’s well into the current growth cycle. The average monthly gain of 112,000 since April is still solid against the backdrop of an economy that’s operating at or near full employment and several years into its expansion.

- Other underlying components of the report tend to reinforce that view. June hiring, while more subdued than anticipated, was still spread fairly well across the major economic sectors. Construction and manufacturing both added workers — certainly not indicative of a stumbling economy. Service sector hiring was fairly widespread, with a large reduction in leisure and hospitality jobs being a surprising outlier. Many had forecast additional hiring needed to support the draw of travelers from abroad and within the U.S. flocking to World Cup venues. That either didn’t materialize or was more than offset by losses elsewhere. Government payrolls also edged up in June for the second consecutive month.

- Across the two private sector pillars, more than half of the industries reported net hiring — a marked improvement compared to one year ago.

- The breadth of job gains across goods producers, service providers, and the public sector, although not as strong as expected, still suggests that the labor economy is on a generally healthy footing, albeit one that lacks the robustness of the peak hiring boom of a few years ago. It’s not one without its warts though.

- Teenage unemployment remains quite high, with fewer entry-level jobs available for those looking for summer work or lacking prior work experience. It’s a reality that was exacerbated by last month’s decline in leisure and hospitality jobs — a mainstay for less experienced workers. Softer hiring there will disproportionately impact teenage workers, which is a reality that’s evident in unemployment close to 15% for workers in that age range.

- Markets reacted positively to the weaker-than-anticipated jobs report as the potential for a Fed rate hike was recalibrated lower. A labor market that regathered significant hiring momentum could have amplified the case for a rate hike, with inflation also still running high. Indications that hiring might not be as robust as previously reported dims that case at the margin.

- Other macro factors should also help to keep the Fed on hold. The recent sharp decline in oil prices should set up broader inflation measures to ease in the coming months, further diminishing the need for higher rates. Recent surveys indicate that inflation expectations have already started to recede, providing more leeway for the Fed to adopt a patient approach.

- For now, the market is still pricing in a rate hike before year end; whether the data will ultimately push policymakers in that direction remains to be seen. In the meantime, Fed Chair Warsh appears to be all in on jawboning inflation expectations lower, reaffirming that the change in leadership at the Fed doesn’t alter the central bank’s commitment to — or focus on — using its policy levers to reestablish price stability. In “Fed speak,” that’s a commitment to return to 2% inflation. Can the Fed deliver on that pledge with more success than in recent years? That remains to be seen.

Media mentions:

Our expert was recently quoted on this topic in the following publications:

Past performance does not guarantee future results. All investments include risk and have the potential for loss as well as gain.

Data sources for peer group comparisons, returns, and standard statistical data are provided by the sources referenced and are based on data obtained from recognized statistical services or other sources believed to be reliable. However, some or all of the information has not been verified prior to the analysis, and we do not make any representations as to its accuracy or completeness. Any analysis nonfactual in nature constitutes only current opinions, which are subject to change. Benchmarks or indices are included for information purposes only to reflect the current market environment; no index is a directly tradable investment. There may be instances when consultant opinions regarding any fundamental or quantitative analysis may not agree.

Plante Moran Financial Advisors (PMFA) publishes this update to convey general information about market conditions and not for the purpose of providing investment advice. Investment in any of the companies or sectors mentioned herein may not be appropriate for you. You should consult a representative from PMFA for investment advice regarding your own situation.