The opportunity zone (OZ) incentive was created to attract investment in specific low-income census tracts. Investor benefits include deferral of capital gains invested in a qualified opportunity fund (QOF), exclusion of 10% of deferred capital gains invested in a QOF for at least five years, and exclusion of gains upon exit from the QOF investment after a more than 10-year hold. The 10-year gain exclusion applies to both gains from appreciation as well as depreciation recapture. Since depreciation isn’t recaptured upon exit to the extent that the OZ 10-year exclusion applies, utilizing a cost segregation study can supercharge a QOF investor’s after-tax internal rate of return (IRR), as explained below.

What is cost segregation?

- Cost segregation allows a taxpayer that purchases, constructs, or renovates real estate used in a business to accelerate depreciation deductions into earlier years of a building’s useful life. The process can provide an added bonus in OZs because depreciation recapture isn’t required at the time of a sale to the extent that the 10-year exclusion applies. The process combines engineering, construction, and tax expertise to maximize the value of depreciation tax deductions.

- Instead of depreciating an entire building over 27.5 years (residential) or 39 years (commercial), a cost segregation study identifies personal property within the structure as well as land improvements around the building that can be depreciated over shorter and more accelerated recovery periods.

- In addition, cost segregation helps identify qualified improvement property (QIP) and qualified production property (QPP), which can result in immediate expensing (via bonus depreciation) of a significant portion of the cost of rehabilitating a commercial or mixed-use property.

- In general, an accounting or consulting firm that specializes in cost segregation should be engaged to perform the cost segregation analysis and issue a report that satisfies the Internal Revenue Service (IRS) documentation requirements.

How can cost segregation supercharge OZ after-tax IRR?

- Outside of OZs, the value of cost segregation is derived from the following:

- Timing differences. Accelerating depreciation deductions makes them more valuable due to the time value of money.

- Tax rate differences. In certain situations, accelerated depreciation deductions may be taxed at a lower rate when the timing difference reverses upon sale of the property.

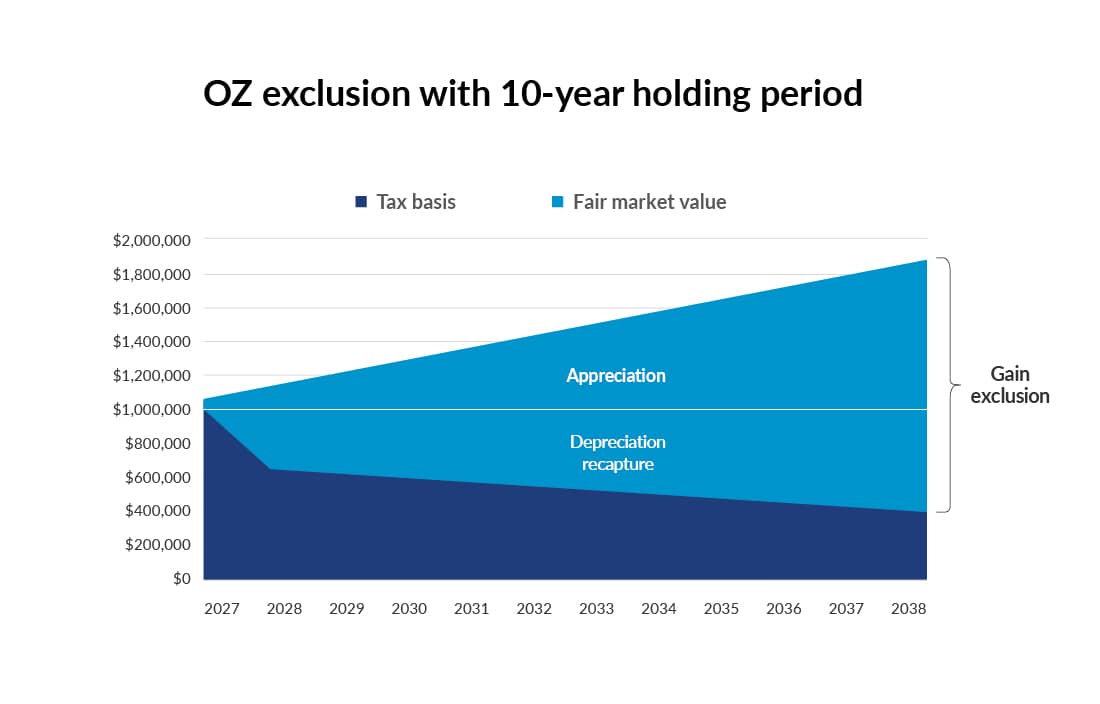

- In OZs, the value of cost segregation is enhanced because depreciation isn’t required to be recaptured upon sale to the extent that the 10-year exclusion applies. This dynamic effectively creates a permanent difference that’s not achievable outside of an OZ. Exhibit 1 shows the impact of the OZ 10-year gain exclusion on an investment with a $1 million basis when depreciation recapture isn’t subject to tax.

- To the extent that depreciation is accelerated to the period prior to a sale of the building from the period after the sale, a cost segregation study can effectively create deductions out of thin air for a QOF investor, which translates to substantial permanent tax savings. For example, if a QOF sells a commercial building in Year 11, any depreciation deductions that the cost segregation study accelerates from Years 12 through 39 into Years 1 through 11 will become a permanent additional tax deduction which wouldn’t otherwise be available without a cost segregation study.

- A cost segregation study can often identify shorter depreciable lives on approximately 20–30% of the real estate. That percentage can be significantly higher for rehabilitated commercial and mixed-use buildings.

- A cost segregation study can also help a building become eligible for OZ tax benefits that would otherwise not have been available. In particular, existing buildings generally must be substantially improved to qualify for OZ tax benefits, which means that additions to the basis of the building must exceed the building’s adjusted basis at the start of the 30-month measurement period. A cost segregation study can help reduce the purchase price allocated to the building, lowering the bar for the substantial improvement test.

Here’s how a cost segregation study can benefit QOF investors

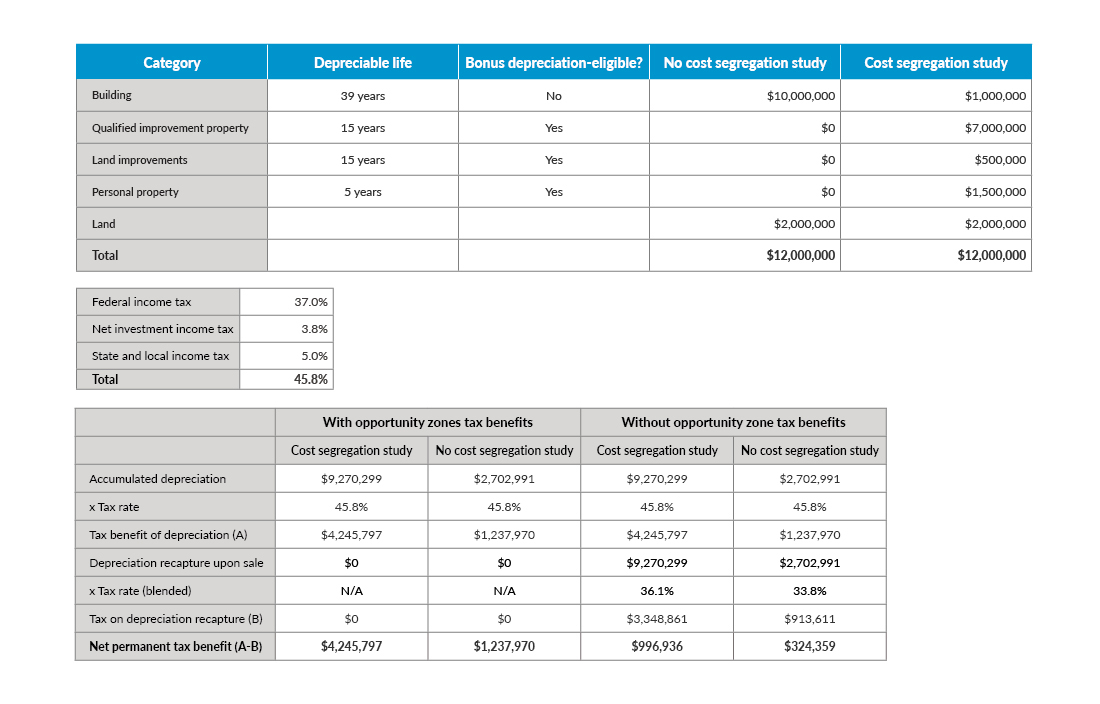

Cost segregation is most impactful in projects involving the rehabilitation of nonresidential real property in an opportunity zone. To illustrate the potential benefits of a cost segregation study for such property, assume the following results of the cost segregation study:

Based on the assumptions outlined above, a cost segregation study generates $6,567,308 of additional depreciation deductions over the holding period of the property which aren’t required to be recaptured upon the sale of the property, assuming the investors qualify for OZ tax benefits and the sale occurs more than 10 years after their investment into the QOF. Such additional deductions result in permanent tax savings of $3,007,827. Please note that the above example ignores the time value of money associated with the additional depreciation deductions. Consequently, the value of a cost segregation study is greater than illustrated above.

It’s important to note that the tax benefits of a cost segregation study for any particular project will depend on certain facts and circumstances, such as the nature of the physical improvements made to the building, whether the project is new construction versus rehabilitation, and whether the building is residential rental property versus nonresidential real property.

Tax planning considerations

A cost segregation study can significantly enhance the after-tax IRR of an investment in a QOF, but maximizing the benefit of the cost segregation study requires proactive planning with your tax advisor and special attention to numerous technical nuances. Consider the following:

- Tax basis. To maximize the benefits of cost segregation, it’s important to structure the transaction so that the QOF investors will have sufficient tax basis to benefit from the accelerated deductions. QOF investors don’t immediately receive tax basis for their capital contributions. So, it’s important to consider how structuring debt can provide basis for QOF investors.

- Substantial improvement test. As mentioned above, existing buildings must be substantially improved to qualify for OZ tax benefits. While a cost segregation study on the purchase price of the building can help a building pass the substantial improvement test, a cost segregation study on the rehabilitation costs could be detrimental to the substantial improvement test. However, such negative impacts can potentially be mitigated by utilizing certain aggregation provisions in the OZ regulations to apply the substantial improvement test. As a result, it’s important to consult your tax advisor to help you consider the impact of a cost segregation study on the substantial improvement test.

- Timing of cost segregation study. Cost segregation studies can be conducted upon purchase of a property, upon completion of a construction/rehabilitation project, or at any point during the holding period. The timing of a cost segregation study can potentially impact the QOF investor’s ability to take advantage of valuation discounts to reduce the amount of deferred gain required to be recognized at the end of the deferral period. Your tax advisor can help you determine the optimal point in the QOF lifespan to perform a cost segregation study.

- Interplay with other incentives. If a project is using other incentives like historic tax credits, it’s important to consult a tax professional to understand how a cost segregation study may impact other incentives and to determine the strategy that optimizes the aggregate value of all tax benefits.

- Tax-exempt use restrictions. The benefit of a cost segregation study may be reduced for certain projects that have either tax-exempt owners or tax-exempt tenants. Your tax advisor can help you determine the extent to which such restrictions may apply, and if there may be opportunities to mitigate the impact of such restrictions.

- Interplay with interest deduction limitations. After 2017 tax reform, many real estate projects are subject to limitations on their ability to deduct interest expenses. In certain situations, an election can be made by the property owner, that mitigates the impact of such interest deduction limitations. To maximize the benefit of a cost segregation study, it’s critically important to consult your tax advisor regarding the potential interplay between the interest deduction limitations and the ability to claim bonus depreciation.

To learn more about how a cost segregation study could accelerate deductions and generate tax savings for opportunity zone properties, please contact your tax advisor to discuss the specific facts and circumstances of your investments.