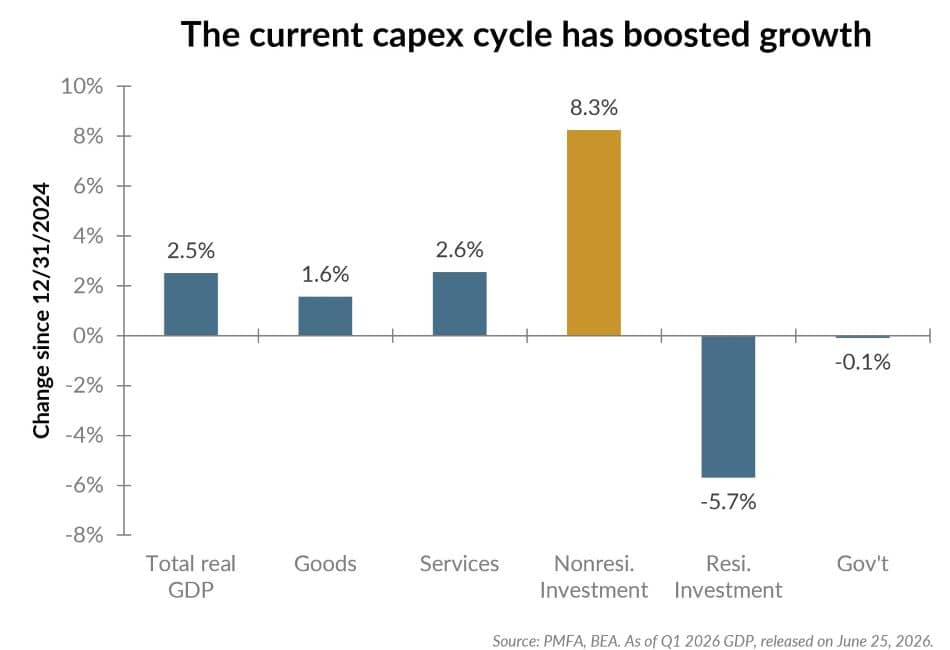

Recent GDP data underscores an important shift in the underlying sources of economic growth, with business spending becoming a more meaningful driver of activity. Since the end of 2024, real GDP has advanced 2.5%, but the strongest component by far has been nonresidential (business) investment, up 8.3%. That stands in contrast to declining residential investment and essentially flat government spending. It also represents a striking change in leadership in a consumer-driven economy.

That strength in business investment is especially important because it’s helped offset a consumer backdrop that remains uneven. The University of Michigan’s consumer sentiment index improved in June but remains subdued, with high prices still weighing on household finances and crimping real (inflation-adjusted) spending growth. Consumer contributions to real GDP growth were weak in Q1, although recent retail sales results have been good, even after accounting for the lift provided by higher gasoline prices. Put simply, the economy is being carried forward despite consumer caution not due to robust growth in household spending.

The near-term implications are constructive. Capital investment is supporting output, employment, and income growth despite uneven consumption. The emerging risk is that expectations for technology-related demand outrun realized adoption and profitability, turning today’s investment tailwind into a potential source of overinvestment.

At some point, consumers are likely to need to take the growth baton back from business investment. For now, though, it’s an important catalyst keeping the expansion on track.

Past performance does not guarantee future results. All investments include risk and have the potential for loss as well as gain.

Data sources for peer group comparisons, returns, and standard statistical data are provided by the sources referenced and are based on data obtained from recognized statistical services or other sources believed to be reliable. However, some or all of the information has not been verified prior to the analysis, and we do not make any representations as to its accuracy or completeness. Any analysis nonfactual in nature constitutes only current opinions, which are subject to change. Benchmarks or indices are included for information purposes only to reflect the current market environment; no index is a directly tradable investment. There may be instances when consultant opinions regarding any fundamental or quantitative analysis may not agree.

Plante Moran Financial Advisors (PMFA) publishes this update to convey general information about market conditions and not for the purpose of providing investment advice. Investment in any of the companies or sectors mentioned herein may not be appropriate for you. You should consult a representative from PMFA for investment advice regarding your own situation.