Illinois enacted Public Act 104-0468 (Senate Bill 3019) on June 16, adding more than 1,600 pages to the state’s tax and regulatory landscape. The bill includes three new levies on digital activity, while changes to net operating losses, dispositions of qualified small business stock, pass-through entity taxation, hotel marketplaces, and tax incentives will affect a broader range of taxpayers. The digital provisions generally begin Jan. 1, 2027. Each depends on information that many businesses don’t currently collect in a tax-ready form, including user location, customer location, monthly user counts, and the value of digital assets associated with individual services.

Net operating loss limitation

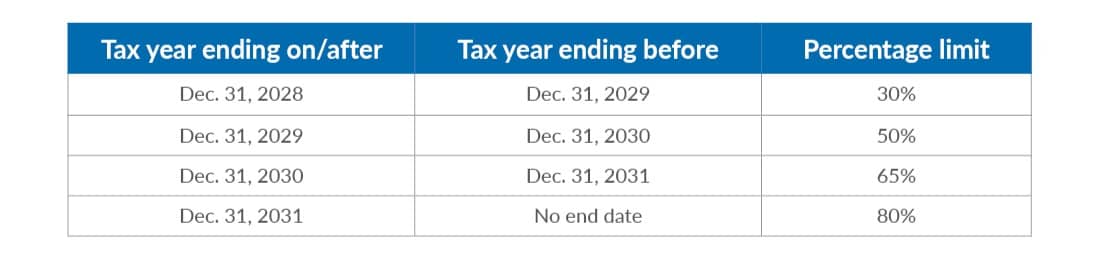

The legislation continues Illinois’ corporate NOL limitation but begins a gradual transition toward the federal limitation. For taxable years ending on or after Dec. 31, 2027, and before Dec. 31, 2028, the Illinois NOL carryforward deduction for C corporations is limited to the greater of $500,000 or 15% of net income computed without regard to the NOL deduction. The limitation increases in subsequent years as follows, where the applicable taxpayer limitation is the greater of $500,000 or the stated percentage:

The NOL limitation doesn’t impact other taxpayers, such as S corporations, partnerships, or individuals.

Corporate taxpayers may consider updating cash-tax forecasts, deferred-tax calculations, valuation allowances, and transaction models. The scheduled phase-in provides eventual relief, but it doesn’t eliminate near-term cash taxes for C corporations holding Illinois losses.

Section 1202 decoupling

For tax years ending on or after Dec. 31, 2026, Illinois requires an addition modification for gains excluded from federal gross income under IRC Section 1202 for individuals, partnerships, trusts, and estates. Because the change applies to taxable years ending on or after Dec. 31, 2026, taxpayers with Section 1202-eligible transactions occurring earlier in 2026 should evaluate the effect of the Illinois addback on their remaining estimated tax payments.

Pass-through entity (PTE) tax elections for partnerships

For taxable years ending on or after Dec. 31, 2026, a partnership may elect either the existing Illinois-sourced income method or a full distributive share method. Under the latter, a partnership computes and pays tax on the full distributive share of net income attributable to each Illinois-resident partner, while apportioned business income is used solely to determine the tax attributable to nonresident partners. The election is annual, applies to all partners, and is irrevocable for the year. The election doesn’t apply to S corporations.

Targeted advertising services tax

Beginning Jan. 1, 2027, providers with more than $1 million of Illinois targeted-advertising receipts during the preceding four quarters are subject to a 10% tax on gross receipts from services provided in Illinois.

“Targeted advertising services” includes programmatic advertising delivered through a digital interface or “any other method of delivery” using personal information about the people receiving the advertisement. The definition reaches banner, search engine, interstitial, social media, native, rewarded, and other comparable advertising. Advertising on a digital interface owned or operated by or for a news media entity is excluded.

Illinois receipts are determined by the location of the person receiving the advertisement. Providers must consider the totality of technical and nontechnical information within their possession or control. An Illinois home address, mailing address, internet protocol address, or other data showing an Illinois place of primary use creates a rebuttable presumption of Illinois location, with the burden placed on the provider.

Monthly returns and payments are due electronically on or before the 20th day of the following month.

Social media fee

Beginning Jan. 1, 2027, social media platforms must report the average number of monthly Illinois users and pay a graduated monthly fee based on Illinois users from whom the platform collects data. The first 100,000 users are outside the fee schedule. The monthly fee is then calculated as follows:

- More than 100,000 but not more than 500,000 Illinois users: 10 cents for each user above 100,000.

- More than 500,000 but less than 1 million Illinois users: $40,000 plus 25 cents for each user above 500,000.

- More than 1 million Illinois users: $165,000 plus 50 cents for each user above 1 million.

The law generally defines a social media platform as a website or internet medium that permits users to create accounts, generate and share content, view content created by others, and primarily serves as a medium for users to interact with content generated by other users.

Administration is by the Secretary of State, rather than the Department of Revenue.

Failure to pay the appropriate amount is 100% of the unpaid fee and is applied each month until paid.

Digital assets tax

Beginning Jan. 1, 2027, Illinois will impose a 0.2% tax on Illinois customers receiving a digital asset from a digital asset broker. Brokers maintaining a place of business in Illinois must collect the tax, while remote brokers are brought within the regime once Illinois gross receipts from covered services reach $100,000 during the preceding four quarters.

The tax is imposed on the value of the digital asset and covered activities include individual occurrences of exchanging, transferring, or storing a digital asset.

For electronic and telephone transactions, the Illinois location is presumed from customer account information, including mailing and home addresses, internet protocol address, and other data showing place of primary use. Sales taking place in person are determined by the physical location. The digital asset broker bears the burden of proving that a customer isn’t located in Illinois. The return is due monthly and must be filed and paid electronically.

Other changes

- The act extends several incentive programs, including the Illinois R&D credit through tax years ending prior to Jan. 1, 2037, the angel investment credit through 2032, and various affordable housing, historic redevelopment, apprenticeship, theater, and energy credits.

- Beginning July 1, 2026, hotel marketplace facilitators with at least $100,000 of Illinois gross rental receipts during the preceding 12 months are treated as hotel operators for state hotel tax and local hotel taxes administered by the department. Facilitators assume collection, remittance, reporting, and audit responsibility for marketplace transactions.

- The act expands the Sports Wagering Act to include “exchange wagers,” including certain prediction market contracts tied to sporting contests or events. It imposes a transaction tax of 1.75% on each exchange wager, increasing to 3.5% after the first five million exchange wagers conducted by a licensee during a fiscal year. The act also establishes licensing and taxation requirements for fantasy contest operators.

- Beginning on July 1, 2026, fantasy contest operators are subject to a 15% tax on their adjusted gross fantasy contest receipts.

- The act prohibits the Department of Commerce and Economic Opportunity from issuing new data center certificates of exemption after July 1, 2029. Certificates in effect on that date are preserved.

Proposals to watch in future sessions

Several significant revenue proposals didn’t pass, including mandatory worldwide combined reporting, decoupling from IRC Section 174A, repeal of the manufacturing consumables sales tax exemption, and an immediate pause on data center incentives. Their failure to pass means they have no present effect. They are nevertheless useful as indicators of the state’s policy interests and the revenue options that may return in later sessions.

The FY2027 budget preserves and funds the Illinois Independent Tax Tribunal. There was a proposal that the tribunal would be folded into the Department of Revenue.

Key takeaways

Taxpayers and advisors may want to:

- Evaluate anticipated NOL utilization in forecasts and valuation allowances, calculate the Illinois effect of Section 1202 gain and any resulting estimated payment implications, and compare both PTE tax-base methods for electing partnerships.

- Identify entities and revenue streams potentially covered by the new digital taxes.

- Monitor regulations, forms, and litigation involving the new taxes, as well as proposals that may return in future sessions.