The bottom line: A step toward normalization, but a long way from the target

- The June report on consumer inflation delivered all that was hoped for and a little bit more.

- The sharp decline in energy prices against an easing of tensions in the Middle East — even if tenuous — provided more relief to headline inflation than had been anticipated. It’s less clear whether that can be replicated in July’s data, given the recent flareup around the Strait of Hormuz and resulting spike in crude oil prices in recent days.

- Even so, the path back to the Fed’s 2% inflation target remains a challenging one, and it’s not likely to be accomplished either as smoothly or as rapidly as consumers or policymakers would prefer.

- One month doesn’t make a trend, and the recent reversal in oil prices will make further positive progress in the coming months a tougher proposition.

- Further, despite the improvement, various indicators still clearly signal that consumer inflation continues to be well above the Fed’s target. Consequently, the case for a rate hike in the coming months remains on the table.

- The recent disinflationary impulse is encouraging, but there’s a long way to go to get back to an inflation climate that Fed policymakers will deem acceptable.

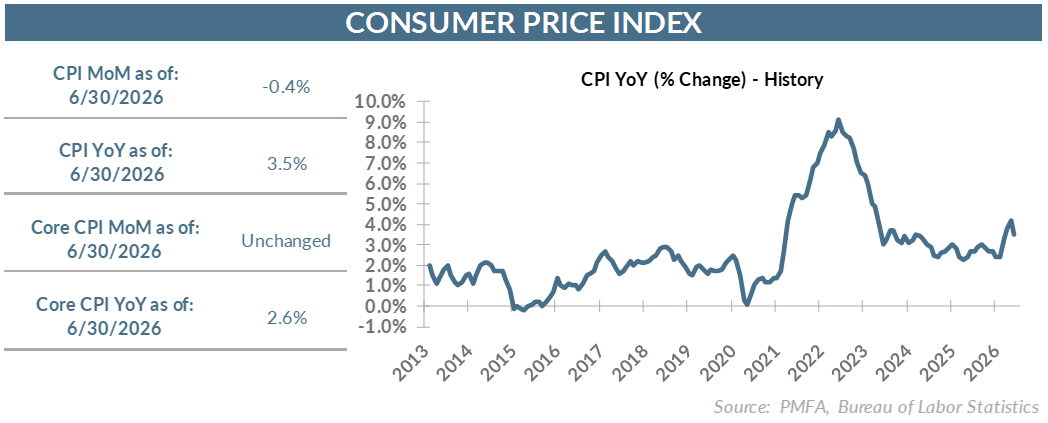

By the numbers: Better than expected

- The consumer price index fell 0.4% in June, a much larger decline than the consensus forecast for a more muted dip of -0.1%.

- The sharp decline in energy prices was the key catalyst behind the better-than-expected result.

- Core CPI, which excludes food and energy, was flat in June, also coming in fractionally better than the 0.2% forecast heading into the report.

- The June pullback also filtered through to the 12-month index reading, which dipped to 3.5% for the headline number at 2.6% for core inflation.

New Fed leadership recommits to price stability, but the specifics remain unclear

- At the margins, the report seems to give the Fed more time to evaluate the timing of its next move.

- The wild card is the change in leadership at the Fed, with new Fed Chair Kevin Warsh striking a very hardline tone on inflation out of the gate and an unambiguous statement of resolve that policymakers will achieve price stability.

- What will be required to accomplish that goal and the potentially painful side effects of the necessary policy medicine remain to be seen.

- Warsh has signaled clearly that there are changes coming from within the Fed. The immediate change in communication style was evident in the brevity of the first FOMC statement under his leadership and at his accompanying press conference.

- What comes next in terms of actual policy execution will require some patience on the part of the markets and Fed watchers. Warsh is unlikely to provide much, if any, guidance in his congressional testimony this week. His style likely won’t be as intentionally ambiguous as the one adopted by former Fed Chief Alan Greenspan, but early indications are that he may lean more toward Greenspan’s preference or opaqueness than has been the case under recent Fed leadership.

- Warsh’s message will likely reiterate the one he delivered at the post-FOMC meeting press conference — a firm restatement of the Fed’s resolve, an unrelenting focus on finally reining in inflation, and a commitment that the Fed will take appropriate steps to adapt as needed to accomplish those goals.

- The market is still pricing in at least one rate increase before the end of the year, but today’s better-than-expected inflation news may have pushed back the timing of any move, giving policymakers more time to assess incoming data and chart the path they deem appropriate on a timeline they’re comfortable with.

Past performance does not guarantee future results. All investments include risk and have the potential for loss as well as gain.

Data sources for peer group comparisons, returns, and standard statistical data are provided by the sources referenced and are based on data obtained from recognized statistical services or other sources believed to be reliable. However, some or all of the information has not been verified prior to the analysis, and we do not make any representations as to its accuracy or completeness. Any analysis nonfactual in nature constitutes only current opinions, which are subject to change. Benchmarks or indices are included for information purposes only to reflect the current market environment; no index is a directly tradable investment. There may be instances when consultant opinions regarding any fundamental or quantitative analysis may not agree.

Plante Moran Financial Advisors (PMFA) publishes this update to convey general information about market conditions and not for the purpose of providing investment advice. Investment in any of the companies or sectors mentioned herein may not be appropriate for you. You should consult a representative from PMFA for investment advice regarding your own situation.