First, the bottom line: Pockets of weakness, pockets of strength

- June retail results provide a mixed picture of where consumers are spending, with clear pockets of weakness offsetting other pockets of strength.

- The June report suggests that consumers are spending but are perhaps taking a more discerning approach to where they’re spending and how they’re prioritizing their choices.

- That’s a very different story than one that suggests that consumers are unambiguously in trouble, struggling to keep up with an extended period of rising prices.

- Lower-income households are undoubtedly still feeling the pinch of inflation and the need to find creative ways to stretch their dollars further.

- At the most macro level, consumers still appear to be pulling their weight as a key growth engine for the economy.

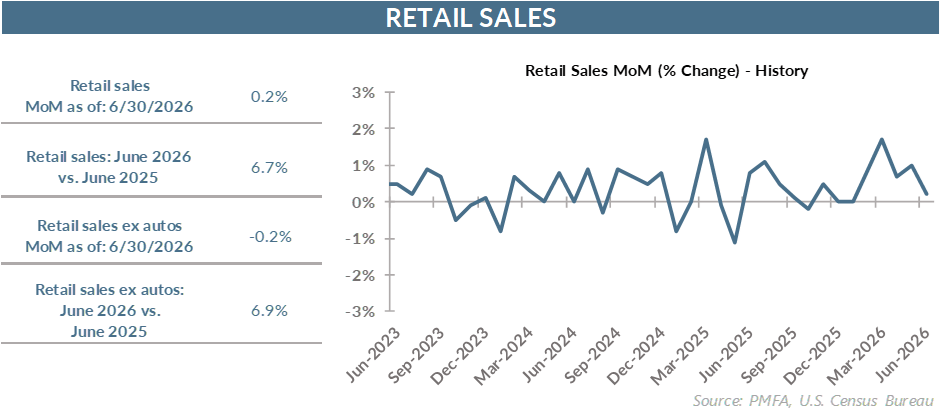

By the numbers: Falling gas prices mask solid underlying gain in June

- Retail sales rose by 0.2% in June — falling well short of the consensus forecast for a blowout 1.4% gain.

- Underlying the tepid headline gain is a much more nuanced story — one that’s neither universally positive nor negative.

- Gas station sales fell by 5.3% as falling prices at the pump provided relief to consumers but provided a hit to sales measured in nominal terms. Ex-gas stations, the adjusted retail sales gain for June of 0.7% looks quite solid.

Higher prices contribute to a more discerning consumer

- As a key data point providing insight into the health of the consumer and household finances, the retail sales report is important. The fact that it’s measured in nominal terms, however, doesn’t always tell the whole story. That’s clearly the case in the June data.

- For as much as consumers felt the sting of higher gas prices in recent months, they finally felt some relief as fuel prices tumbled since late May on hopes of easing tensions in the Middle East and improved flow of crude oil.

- Falling fuel prices weighed on headline sales data, but a smaller bill at the pump was a source of relief for consumers and provided at least a little more cushion in household spending budgets.

- The sting of higher gasoline prices faded in June, although a partial reversal is already being seen with tensions in the Middle East ratcheting up again in the past week.

- Beyond the volatility in fuel prices, there are other stories seemingly at play across the retail sector.

- Nonstore retailers were a big winner; the 1.9% gain for the part of the retail economy closely aligned with online shopping suggesting that consumers weren’t shy about spending on goods that were priorities. The strong monthly result was also juiced by Amazon’s Prime Day incentives, which was extended to several days in late June.

- Automobile sales also put up strong numbers, gaining 2.0% for the month on the heels of a solid 1.1% gain in May. Dealer incentives have sweetened the opportunity for potential buyers, who have responded positively in recent months.

- More broadly, the story for retailers was mixed, with most sectors seeing very little change for the month.

- Beyond the short-term ebb and flow of spending, the secular shift in consumer preferences remains clear: online commerce continues to grow at a strong clip. The environment for brick-and-mortar retailers looks very different, illustrating the bifurcated nature of the retail market and the ease of shopping with a click rather than a car ride.

Past performance does not guarantee future results. All investments include risk and have the potential for loss as well as gain.

Data sources for peer group comparisons, returns, and standard statistical data are provided by the sources referenced and are based on data obtained from recognized statistical services or other sources believed to be reliable. However, some or all of the information has not been verified prior to the analysis, and we do not make any representations as to its accuracy or completeness. Any analysis nonfactual in nature constitutes only current opinions, which are subject to change. Benchmarks or indices are included for information purposes only to reflect the current market environment; no index is a directly tradable investment. There may be instances when consultant opinions regarding any fundamental or quantitative analysis may not agree.

Plante Moran Financial Advisors (PMFA) publishes this update to convey general information about market conditions and not for the purpose of providing investment advice. Investment in any of the companies or sectors mentioned herein may not be appropriate for you. You should consult a representative from PMFA for investment advice regarding your own situation.