First, the bottom line

- The economy had much to absorb this year, particularly related to trade policy and tariffs; that process is ongoing as the effects of higher import levies filter through the economy, but thus far, the economy appears to be weathering changing conditions with relative success.

- Volatility in headline GDP data from Q1 to Q2 exaggerated the underlying trends, though. Arguably, underlying trend growth wasn’t as weak in Q1 as the negative GDP print suggested, but the strong rebound in top-line growth in Q2 also appears rosier than the reality in recent months. That pace of growth isn’t likely to be sustained in the latter half of the year.

By the numbers: Growth rebounds, but the story remains nuanced

- Revisions to previously reported data on the strength of the economy in Q2 didn’t meaningfully change the narrative but did put a little more polish on the quarter.

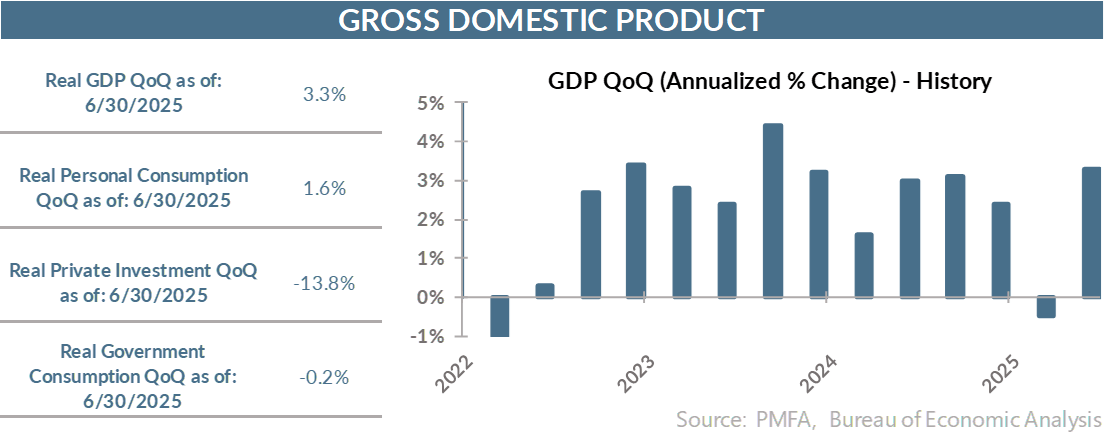

- GDP bounced back strongly in Q2, as the U.S. economy grew at a brisk 3.3% clip — a marked reversal from Q1’s 0.5% contraction. Additional data provided a bit more bounce in the rebound from the previously reported 3.0% quarterly gain.

- Beyond the modest improvement in headline growth, the story wasn’t much different, though. A surge in imports by companies and consumers looking to front-run anticipated tariffs washed through the economy and skewed the growth story over the first half of the year. In reality, the economy softened but wasn’t sinking in Q1 as the negative GDP print might have suggested. Conversely, Q2’s growth surge overstates the underlying trend and isn’t likely to be sustained.

- Volatility in trade flows and business inventory levels weighed heavily on growth early in the year before reversing course, acting as a tailwind in recent month, whipsawing GDP data in the process.

- Underlying the headline GDP data is a more nuanced picture of the state of the economy. Consumer spending growth slowed in the first half of the year. Even so, upwardly revised consumption growth of 1.6% in the second quarter suggests a bit more confidence, continued ability, and improving willingness of consumers to spend.

- That doesn’t mean that it’s business as usual for the average household. Spending on services this year has grown at its weakest pace in several years. Further, spending on goods has gathered some momentum in recent months, but the pace of growth remains slower than in recent years.

- New home construction is also having a hard time getting off the ground, weighed down by surging material and labor costs and mortgage interest rates that are much higher than homebuyers had become accustomed to in the post-Global Financial Crisis era. The combination has been a one-two gut punch to potential buyers and made housing affordability a major challenge across much of the United States.

- Residential investment has been negative in four of the last five quarters, weighing moderately on overall economic growth, but providing an important indicator that the lingering impact of surging inflation and higher interest rates since 2022 remains a challenge for many Americans.

- Business investment remains a relative bright spot that’s provided a meaningful boost to the economy, as the race to invest in the infrastructure needed to tap into the AI boom continues. Although the productivity gains expected from AI will take some time to become evident, the immediate impact of investment in hardware and software is already apparent.

Fed policy: A shift in tone signals rate cuts may finally be in sight

- Today’s GDP report provides a bit more clarity on the recent past, but the focus remains on the delicate balance between elevated inflation and a softening labor market. Of particular note is what that balance means for the outlook for interest rates in the coming months.

- Federal Reserve Chair Jerome Powell threw an additional lifeline of hope to investors looking for a September rate cut at his Jackson Hole speech last week.

- At this point, investors are betting on a probable quarter-point cut at the Fed’s September meeting, with additional easing anticipated before year-end.

- A September cut increasingly looks baked in the cake; whether policymakers will deliver additional easing in the months that follow is less certain, but Powell’s acknowledgment of the growing risk to the job market appears to open the door to additional rate cuts even though most measures of inflation remain above the central bank’s comfort zone. Policymakers will have to thread the needle on squaring their policy decisions with these two competing forces to provide reassurance that they have their eye on the ball and are committed to keeping inflation under wraps and inflation expectations in check.

- Investors embraced the tone of Powell’s comments last week, with stocks surging on the potential for an easier interest rate backdrop before year-end.

- Whether or not lower interest rates can provide a spark to ignite stronger job creation remains to be seen. Concerns about the impact of tariffs and the near-term economic outlook were real, but the term “recession” has been seldom used in corporate earnings calls over the last quarter. Further, small business surveys continue to note the difficulty that employers have in finding qualified workers.

- There’s no question that job openings and hiring has slowed in recent years, but a lack of labor supply will also put a practical cap on job creation, a reality that may be further exacerbated by a reduced flow of immigrants into the labor force. That may present a challenge that lower interest rates alone may not be sufficient to overcome.

Media mention:

Our experts were recently quoted on this topic in the following publication:

Past performance does not guarantee future results. All investments include risk and have the potential for loss as well as gain.

Data sources for peer group comparisons, returns, and standard statistical data are provided by the sources referenced and are based on data obtained from recognized statistical services or other sources believed to be reliable. However, some or all of the information has not been verified prior to the analysis, and we do not make any representations as to its accuracy or completeness. Any analysis nonfactual in nature constitutes only current opinions, which are subject to change. Benchmarks or indices are included for information purposes only to reflect the current market environment; no index is a directly tradable investment. There may be instances when consultant opinions regarding any fundamental or quantitative analysis may not agree.

Plante Moran Financial Advisors (PMFA) publishes this update to convey general information about market conditions and not for the purpose of providing investment advice. Investment in any of the companies or sectors mentioned herein may not be appropriate for you. You should consult a representative from PMFA for investment advice regarding your own situation.