First, the bottom line: The loss of economic momentum in Q4 was worse than believed

- Following two consecutive strong readings for the second and third quarters, the economy was expected to soften heading into year-end. It’s now increasingly clear that the economy not only slowed but stumbled into the finish line.

- The government shutdown was certainly a major factor in the loss of momentum, but a sharp decline in consumption growth also played a role.

- A lackluster Q4 GDP print was expected; nevertheless, a report this soft is a surprise. It also does nothing to push back against the increasingly negative tone surrounding the economic narrative. Job creation has been choppy but lackluster at best, and inflation now appears poised to reaccelerate on the back of surging energy prices, should they be sustained.

- The fact that growth slowed to a crawl in Q4 helps to explain the soft labor market but also reinforces that the economy has moved into a riskier area and has less cushion, leaving it more exposed to a potential downdraft.

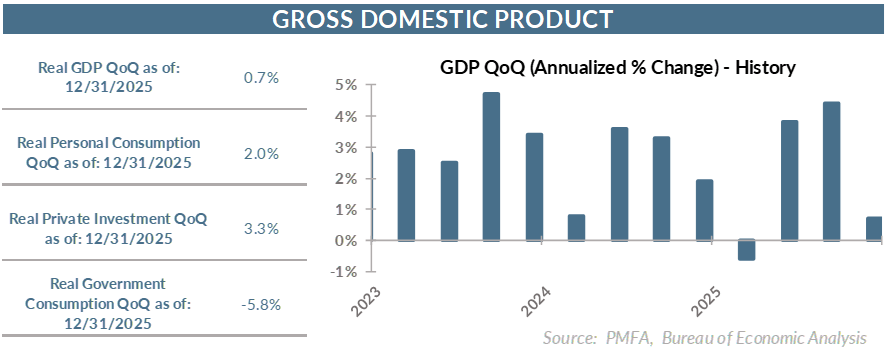

By the numbers: Q4 GDP report held little good news

- The second reading on Q4 GDP was an unambiguous setback, with data revisions slashing growth estimates for the quarter from a previously reported 1.4% to just 0.7%.

- Federal government spending plunged by 16.7% in Q4, with nondefense spending falling by nearly 25% as the extended shutdown took a large bite out of government consumption. That alone shaved nearly 1.2 percentage points off growth, without which a much more palatable 2% growth pace might have been within reach.

- The slowdown wasn’t just a government story though. Most measures of consumer sentiment have been quite restrained, as many households continue to grapple with the effect of a multiyear surge in prices. While inflation has receded considerably, wage growth has slowed and hiring has stalled, leaving fewer workers successfully changing jobs to enhance their income potential. The combination has continued to pinch consumer budgets and spending.

- Not surprisingly, consumption momentum also slowed considerably, from 3.5% growth in Q3 to just 2% in Q4. Spending on goods advanced by just 0.4%, while services held up better, growing by 2.7% for the quarter.

- A small silver lining: The Fed’s preferred inflation measure embedded in the GDP report eased modestly in Q4. Core PCE, which excludes food and energy, edged down to 2.7%, but remained solidly above the Fed’s 2.0% target.

Broad thoughts: Risks abound as more than a whiff of stagflation is in the air

- Looking ahead, a mixed bag of factors is poised to influence the trajectory of the economy in the coming months. A sharp reversal in government spending should provide a solid boost to Q1 growth. A boost could also come from larger tax refund checks that could provide additional fuel for household spending. All else being equal, both have been expected to act as growth tailwinds in Q1 and ripple into the months ahead.

- Conversely, the near-term impact of surging oil prices and significant uncertainty about the geopolitical roadmap raise both practical constraints on household spending and the risk that an already-subdued consumer mood will turn gloomier. Even with a little extra cash on hand, consumers are likely to be a bit more hesitant to spend on discretionary goods and services, particularly if there are indications that higher energy prices may stick for some time.

- Higher gasoline prices act as a tax on consumers that will dampen the anticipated positive impact of larger tax refunds in the near term. The biggest question is how durable the recent increase in energy prices will prove to be; the answer hinges largely on whether or not an off-ramp for the conflict can be found and how quickly the flow of oil can be resumed. Recent developments, including the mining of the Strait of Hormuz, are much more reflective of a further escalation in the conflict than an easing in tensions.

- The near-term path for the economy looks increasingly bumpy, while the window of risk has opened wider. That’s going to up the ante for Fed policymakers.

- Monetary policy remains slightly restrictive — a justifiable position given the elevated state of inflation and fears of a potential second wave rising anew. That stands at odds with an economy that’s growing below potential and a labor market that’s perilously close to grinding to a standstill.

- Slower growth, stalling job creation, and higher inflation? That’s more than a whiff of stagflation in the air — that risk is now center stage for policymakers.

- It’s a delicate balancing act that will test the mettle of a Federal Reserve that’s had to navigate an inordinate number of challenges in recent years. It also provides plenty for investors to think about as they consider their next steps and optimal positioning.

Media mentions:

Our experts were recently quoted on this topic in the following publications:

Past performance does not guarantee future results. All investments include risk and have the potential for loss as well as gain.

Data sources for peer group comparisons, returns, and standard statistical data are provided by the sources referenced and are based on data obtained from recognized statistical services or other sources believed to be reliable. However, some or all of the information has not been verified prior to the analysis, and we do not make any representations as to its accuracy or completeness. Any analysis nonfactual in nature constitutes only current opinions, which are subject to change. Benchmarks or indices are included for information purposes only to reflect the current market environment; no index is a directly tradable investment. There may be instances when consultant opinions regarding any fundamental or quantitative analysis may not agree.

Plante Moran Financial Advisors (PMFA) publishes this update to convey general information about market conditions and not for the purpose of providing investment advice. Investment in any of the companies or sectors mentioned herein may not be appropriate for you. You should consult a representative from PMFA for investment advice regarding your own situation.

.jpg?la=en&h=307&mw=480&w=480&hash=44A92388F3F9E8FE565D440232F38669)