First, the bottom line: It’s a weak report

- Silver linings are hard to find in an unambiguously weak February jobs report. Job creation slowed considerably last year, but the January report provided a spark of hope that conditions might be stabilizing. That emergent sense of relief now appears likely to have been short-lived.

- The labor economy has been characterized by a “no hire, no fire” backdrop for some time. Jobless claims have been rangebound for some time and low enough to alleviate the concerns that slowing job creation would otherwise justify.

- With nonfarm payrolls growth barely breaking even over the past three months, any signs of a meaningful uptick in unemployment claims could be a cause for alarm. “No hire” is still clearly intact; the question is whether “no fire” can or will persist for very long with hiring so close to stalling out completely.

By the numbers: Unemployment held in check by labor force contraction

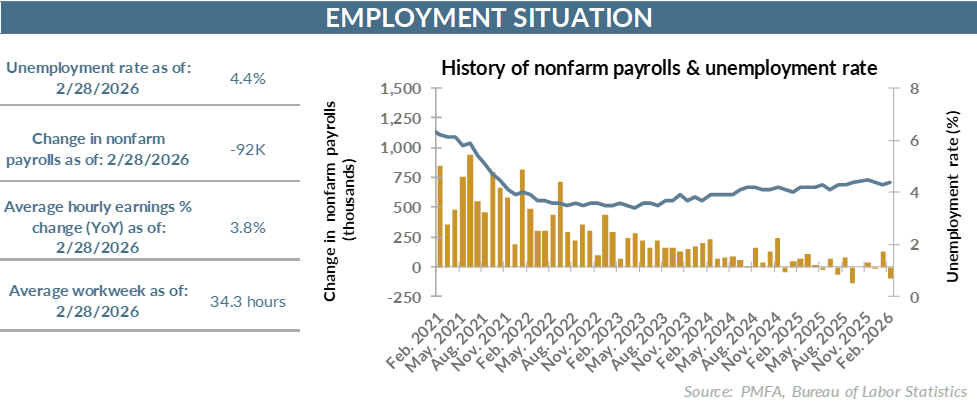

- Nonfarm payrolls unexpectedly declined by 92,000 in February — far softer than an expected gain of 58,000, confirming the recent sluggish hiring trend.

- Downward revisions to previously reported gains also hang heavily over the data. January’s payroll gain was nudged modestly lower, but December’s weak increase was revised sharply lower to a loss of 65,000 jobs. The three-month average nonfarm payroll gain now stands at less than 6,000 per month.

- The unemployment rate edged up to 4.4%, a modest increase that was mitigated in part by very sluggish growth in the estimated size of the labor force. The household survey suggests that the number of employed individuals has declined by nearly 850,000 since November. Over that same time frame, labor force participation slipped from 62.5% to 62.0%, with about 1.2 million people exiting the labor force.

- Had labor force participation held steady, the unemployment rate would have topped 5% last month.

- Boil it all down, and you’re looking at a choppy stream of data in recent months that suggests hiring is perilously close to stalling.

Broad thoughts:

- Hiring is weak — whatever the reasons or explanation, there’s little to point to an imminent rebound in job creation. That’s partially a supply-side story as the labor force itself isn’t growing; with fewer available workers, the pool of candidates isn’t terribly deep. It’s also a demand story though, as hiring has been curtailed in response to a loss of economic momentum and uncertainty on multiple fronts, keeping employers in a wait-and-see mode.

- It’s also not a result of a few pockets of weakness. Declining payrolls were pervasive across most sectors of the economy in February, spanning the public and private sectors and across goods and services.

- Even the healthcare sector, a stalwart source of job creation over the past year, turned negative in February, as a number of strikes across the country temporarily sidelined more than 30,000 healthcare workers. Their subsequent return should provide a decent base to build on for March, but fewer job postings and weaker hiring demand will limit the near-term upside in job creation.

- The slowdown in hiring follows a much weaker-than-expected GDP report for Q4 and provides another indication that economic momentum has slowed considerably in recent months.

- That’s also reinforced by today’s release of the January retail sales report, which also pointed to a softening up in spending.

- Retail sales declined in January, with declining car sales weighing notably on the retail sector. Take car sales out of the equation though, and retail results were still flat for the month.

- Consumer angst about affordability and elevated inflation has weighed heavily on measures of the collective consumer mood for some time. Layer on growing cracks in labor conditions, and it can’t be surprising that consumers are tightening up their spending habits. That doesn’t bode well for an economy that remains predominantly consumer-driven.

Past performance does not guarantee future results. All investments include risk and have the potential for loss as well as gain.

Data sources for peer group comparisons, returns, and standard statistical data are provided by the sources referenced and are based on data obtained from recognized statistical services or other sources believed to be reliable. However, some or all of the information has not been verified prior to the analysis, and we do not make any representations as to its accuracy or completeness. Any analysis nonfactual in nature constitutes only current opinions, which are subject to change. Benchmarks or indices are included for information purposes only to reflect the current market environment; no index is a directly tradable investment. There may be instances when consultant opinions regarding any fundamental or quantitative analysis may not agree.

Plante Moran Financial Advisors (PMFA) publishes this update to convey general information about market conditions and not for the purpose of providing investment advice. Investment in any of the companies or sectors mentioned herein may not be appropriate for you. You should consult a representative from PMFA for investment advice regarding your own situation.

.jpg?la=en&h=307&mw=480&w=480&hash=44A92388F3F9E8FE565D440232F38669)