First, the bottom line: An economy not hitting on all cylinders

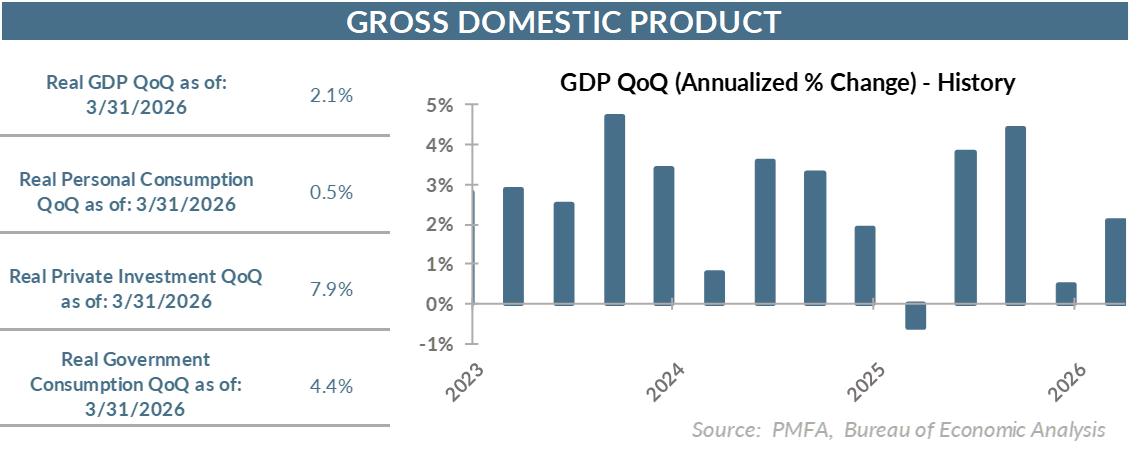

- On the surface, the headline growth number for Q1 appears almost goldilocks at a 2.1% pace, looking neither too hot nor too cold.

- It’s how that growth was achieved that sheds light on the underlying cracks in the economy in the early months of the year.

- Consumers are bearing the brunt of higher prices, which is challenging their spending capacity. That’s a reality that’s been reinforced by the sharp rise in interest rates since 2022 and further intensified by the surge in energy prices earlier this year.

- The result? Paltry growth in consumption that extends to both goods and services and investment in new homes that has been contracting for over a year.

- It also goes a long way toward explaining why the collective consumer mood is exceptionally glum — and unusually so outside of recessionary periods.

By the numbers: Business investment and government spending carried the day

- Today’s revisions to Q1 GDP delivered an upside surprise, although it didn’t necessarily change the narrative about the overall state of the economy.

- Fine-tuned data on the balance of trade provided a lift to previously reported GDP estimates, pushing Q1 growth up from 1.6% to 2.1%.

- Much of that increase was a direct byproduct of downward revisions to import data. Imports function as a drag on the domestic economy; as such, a reduction in imports can prop up GDP growth.

- Business investment was still a key underpinning for the growth engine, with AI-related investment leading the charge.

- A rebound in government spending in the aftermath of last fall’s government shutdown also provided a boost.

- Less rosy was the overall consumer backdrop, as households continue to absorb the impact of higher prices. Measures of consumer sentiment remain quite poor despite generally constructive labor conditions and an expanding economy. The degree of consumer negativity outside of a recessionary climate is notable. While not solely a result of inflation, higher prices straining household spending budgets is unquestionably a major factor weighing on confidence.

- A less confident consumer tends to be more restrained in spending, and that was clearly the case in Q1. Personal consumption expenditure growth was mediocre — its 0.5% gain for the quarter extending to both goods and services.

- Affordability challenges were also readily apparent in the 7.8% annualized contraction in housing investment. That marked the fifth consecutive quarterly decline and the worst single-quarter result since late 2022.

- Beyond the generally weak consumer backdrop, today’s report also reconfirmed the corrosive effects of rising inflation on the economy. The PCE price index surged to 4.6% for the quarter, while the core PCE — which strips out more volatile food and energy prices — increased by 4.4%.

- Albeit concerning, that data is backward looking and already very much outdated. The recent, sharp decline in oil prices is expected to provide near-term relief for consumers and help to rein in headline inflation numbers in coming months.

- How quickly a sustained decline in energy prices may also seep into core inflation remains to be seen, as other factors, most notably service sector and housing inflation, play a greater role.

- Neither measure of inflation is remotely close to the Fed’s stated 2% inflation target, raising the stakes for a Federal Reserve already amid a leadership change and a re-evaluation of its operations and analytical framework.

- At his inaugural press conference last week, new Fed Chair Warsh stressed that the Fed would get inflation under control. Investors heard that message loud and clear. Now it’ll be up to the Fed to try to deliver on that promise.

- Inflation has been a challenge that has vexed monetary policymakers in recent years, and one that might require some reframing of the goal, a rethinking of the approach, or a more aggressive stance on rate policy to ultimately overcome. We’ll undoubtedly hear much more from the Fed regarding those considerations as the rest of the year unfolds.

Past performance does not guarantee future results. All investments include risk and have the potential for loss as well as gain.

Data sources for peer group comparisons, returns, and standard statistical data are provided by the sources referenced and are based on data obtained from recognized statistical services or other sources believed to be reliable. However, some or all of the information has not been verified prior to the analysis, and we do not make any representations as to its accuracy or completeness. Any analysis nonfactual in nature constitutes only current opinions, which are subject to change. Benchmarks or indices are included for information purposes only to reflect the current market environment; no index is a directly tradable investment. There may be instances when consultant opinions regarding any fundamental or quantitative analysis may not agree.

Plante Moran Financial Advisors (PMFA) publishes this update to convey general information about market conditions and not for the purpose of providing investment advice. Investment in any of the companies or sectors mentioned herein may not be appropriate for you. You should consult a representative from PMFA for investment advice regarding your own situation.

.jpg?la=en&h=307&mw=480&w=480&hash=6A627DBF766882E4EE1BC9926E34CB08)