The bottom line? It’s still a “no fire” economy

- Did the Fed’s so-called “insurance” rate cuts work, or did the wobble in the labor markets last year stabilize organically as tariff-related worries subsided? Both likely played a role.

- Whatever the drivers, the steady state of claims suggests that layoffs remain low and within a range consistent with a healthy labor economy, at least in terms of the persistence of the “no fire” characterization that has held firm in recent years.

- Low layoffs are only part of the story though; despite signs of improvement in the pace of hiring, it remains a challenging environment for some parts of the workforce to find the type of job they’re looking for.

By the numbers: Solid and steady

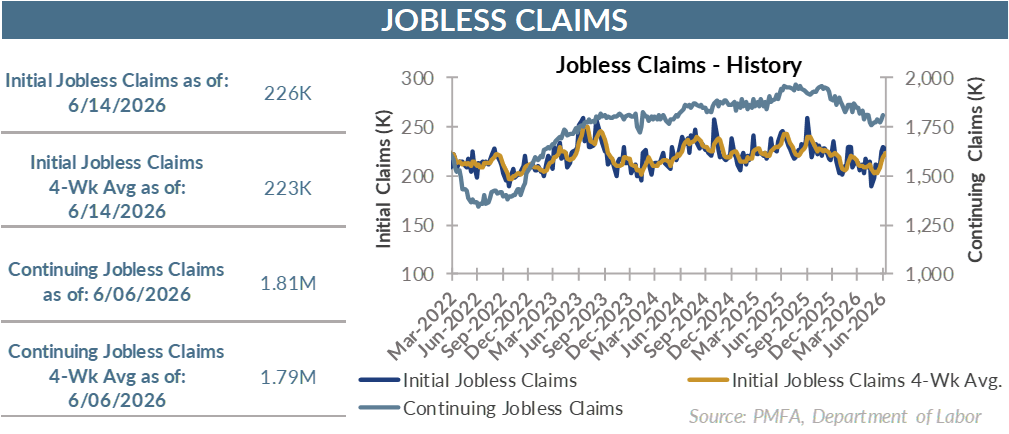

- Initial jobless claims eased last week, dipping to 226,000 for the week ended June 13 from a revised 230,000 for the prior week. Even with that decline, the 4-week moving average rose by 4,000 to 223,250 for the period.

- Continuing claims rose to 1.81 million, landing above forecasts for a relatively steady reading of 1.79 million.

What’s the story? Low layoffs are only one part of a more complex backdrop

- The moderate volatility in some of the recent data notwithstanding, continuing claims have declined meaningfully over the last year, down nearly 150,000 on a 4-week moving average basis. The recent acceleration in nonfarm payroll growth over the past three months also suggests a bit of a resurgence in hiring that provides a bit more stability to the outlook.

- The fact that job creation remains fairly concentrated in a narrow group of service-related sectors does create an asterisk that should be acknowledged, but improvement in construction and manufacturing provide some reassurance that the improvement isn’t limited to healthcare and hospitality, which have accounted for a large part of overall job creation of late.

- Viewed broadly, aggregate data on the labor market is consistent with an economy that remains on a solid growth footing, albeit one that’s being held up to a greater degree by business investment and consumption by the upper half of income earners. It’s also reflective of an aging population and an increased demand for healthcare services that accompanies that demographic trend.

- Those factors help to explain where the hiring needs are stronger … and where they aren’t. The reality is more nuanced though for individuals who are looking for employment, particularly those seeking entry-level roles.

- Certain sectors — most notably tech — that not long ago had a seemingly relentless need for more talent have hit the brakes hard on hiring, leaving a large cohort of young college graduates on the sidelines looking for an opportunity or considering a different path. That’s a reality that can easily be lost in the top-line data, illustrating the bifurcation under the surface that has kept the unemployment rate for newly minted degree holders frustratingly high.

- Beyond technology, it’s also notable in other sectors in which a combination of factors has slowed the pace of hiring considerably. The disruptive effects of AI tools are also apparent in the slower pace of hiring for entry-level jobs, despite its adoption still being in its early stages.

- Add it all up, and the “no fire” environment is still an apt description, providing relative assurance for those currently employed that they’re in a relatively good spot.

- For those looking for work, the story is a bit more muddled — a varied picture depending on their experience, their chosen field, and disparate hiring appetites across various parts of the economy.

Past performance does not guarantee future results. All investments include risk and have the potential for loss as well as gain.

Data sources for peer group comparisons, returns, and standard statistical data are provided by the sources referenced and are based on data obtained from recognized statistical services or other sources believed to be reliable. However, some or all of the information has not been verified prior to the analysis, and we do not make any representations as to its accuracy or completeness. Any analysis nonfactual in nature constitutes only current opinions, which are subject to change. Benchmarks or indices are included for information purposes only to reflect the current market environment; no index is a directly tradable investment. There may be instances when consultant opinions regarding any fundamental or quantitative analysis may not agree.

Plante Moran Financial Advisors (PMFA) publishes this update to convey general information about market conditions and not for the purpose of providing investment advice. Investment in any of the companies or sectors mentioned herein may not be appropriate for you. You should consult a representative from PMFA for investment advice regarding your own situation.