Revised electronic health record regulations are here

On October 16, 2015, the Center for Medicare and Medicaid Services (CMS) issued a final rule that revised the regulations over the Electronic Health Record (EHR) Incentive Program. In addition to modifying the measures needed to meet meaningful use, the final rule modified the reporting period for the program. The key concept changes are summarized below:

Key concepts for the EHR Incentive Programs in 2015 through 2017 (Modified Stage 2)

- Restructured Stage 1 and Stage 2 objectives and measures to align with Stage 3:

- 10 objectives for eligible professionals, including one consolidated public health reporting objective with measure options

- 9 objectives for eligible hospitals and CAHs, including one consolidated public health reporting objective with measure options

- Starting in 2015, the EHR reporting period changes from the federal fiscal year to a calendar year for all providers

- Changed the EHR reporting period in 2015 to 90 days to accommodate modifications to meaningful use

- Modified Stage 2 patient engagement objectives that require “patient action”

- Streamlined the program by removing redundant, duplicative, and topped out measures

- CQM reporting for both EPs and eligible hospitals; CAHs remain as previously finalized

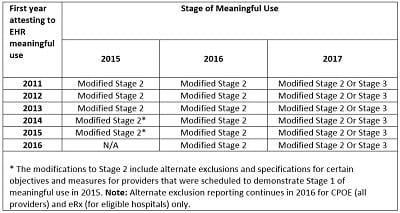

The most significant change with respect to the reimbursement and financial reporting implications is the change in the reporting period. Previously, the reporting period for the EHR Incentive Program corresponded with the federal fiscal year. Under the newly issued final rule, this has been changed to a calendar year reporting period starting with the 2015 year to be consistent with other periods of reporting. CMS recognized that this transition would create timing issues with hospitals; therefore, it modified the reporting period for 2015 to be a 90-day attestation anytime between October 1, 2014, and December 31, 2015. The attestations related to the 2015 EHR reporting period must be filed between January 1, 2016, and February 29, 2016. For subsequent years, the reporting period will be the calendar year in which the attestations must be filed between January 1 and February 28 of the subsequent year. The following table summarizes the stage of the program that each entity would be in depending on the year the hospital began participation.

This change has had implications for both financial reporting and reimbursement that need to be addressed. The following sections outline these implications:

Reimbursement implications

Prospective payment system (PPS) hospitals that attest for the first time within the 2015 year will not be subject to negative payment adjustments for the federal fiscal 2016 or 2017 years. PPS hospitals that have attested to meaningful use prior to 2015 and continue to attest in 2015 will not be subject to the negative payment adjustments for the 2017 federal fiscal year. Critical access hospitals (CAHs) that attest within the 2015 year will not be subject to negative payment adjustments in the 2015 federal fiscal year regardless of whether this is the first time attesting or if they have attested in the past.

There are also cost reporting implications as to which cost reporting period will be used to settle any related incentive payments which do not appear to be addressed in the final rule. It is anticipated that CMS will issue clarifying guidance on this issue.

Financial reporting implications

Based on the above changes to the program, many hospitals will be attesting for a 90-day attestation period anytime between October 1, 2014, and December 31, 2015, during January or February 2016. To determine when the meaningful use revenue related to the 90-day attestation period should be recognized, hospitals should continue to consult with the accounting guidance provided within the HFMA Issue Analysis: Medicare Incentive Payments for Meaningful Use of Electronic Health Records. Based on HFMA Issue Analysis: Medicare Incentive Payments for Meaningful Use of Electronic Health Records, most hospitals would have previously elected one of two accounting policies: the grant accounting model or the contingency model.

For those hospitals that had previously elected to apply the grant accounting model, they should recognize the meaningful use revenue when it’s reasonably assured that it will comply with the conditions of the modified Stage 2 and can reasonably estimate the amount it will receive. Since the federal government has little credit risk, it is reasonable to consider a receipt to be assured once compliance with the meaningful use objectives has been achieved. As such, it is expected the meaningful use revenue will be recognized by December 31, 2015, for hospitals attesting to modified stage 2 during the period January 1, 2016, through February 29, 2016.

For example, a September 30 year end hospital attests to a 90-day attestation period that covers July 1, 2015, through September 30, 2015, would need to recognize the ERH revenue as of September 30, 2015, as long as the amount is estimable. If that same September 30 year end hospital attests to a 90-day attestation period that covers October 1, 2015, through December 31, 2015, the hospital would not recognize the EHR revenue until December 31, 2015.

For those hospitals that had previously elected the contingency model, the meaningful use revenue should be recognized entirely in the period in which the last remaining contingency is resolved. As such, it is expected the meaningful use revenue will be recognized after December 31, 2015, after all identified contingencies have been satisfied.

Please contact your Plante Moran engagement team or member of our reimbursement or professional standards team with any questions that you may have on the impact of these final rules.