There were no significant changes from the 2015 forms and related schedules. Therefore, similar to the 2015 forms and related schedules, the majority of the proposed (but not required) questions from the 2015 series remain but again should not be answered for 2016 returns, according to the instructions. We recommend, however, reviewing these questions to ensure information is available to answer these questions as it is anticipated a response will be required for future filings.

The most notable change is an increase in the penalty for failure to file a complete or accurate Form 5500 which has increased to $2,063 per day.

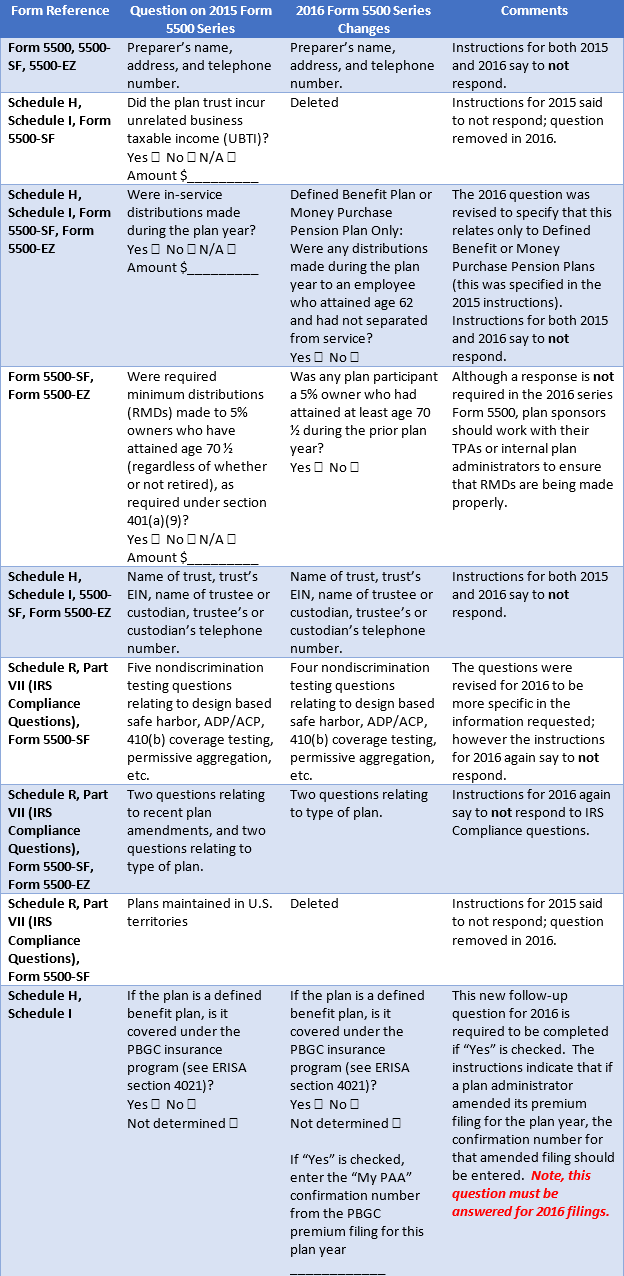

Form 5500/5500-SF and compliance questions

Although the Form 5500 and Form 5500-SF include a section to report “Preparer’s information” at the bottom of the first page, the instructions indicate that this section should not be completed. Compliance questions on Schedule H/I relating to in-service distributions (line 4o), and Trust Information (lines 6a through 6d) should also be skipped. The 2016 series has removed the question relating to Unrelated Business Taxable Income (UBTI), which was not to be answered for 2015.

Schedule H/I has added a question to Line 5c to ask for the “My PAA” confirmation number from the PBGC premium filing for the plan year, if “Yes” has been checked to indicate the plan is covered under the PBGC insurance program. This question is required for the 2016 plan year.

IRS compliance questions located in Part VII (Lines 20a through 22b) of Schedule R, or in Part IX (Lines 15a through 19) on the 5500-SF should not be completed for 2016. These compliance questions are very similar to those that appeared on the Schedule R in 2015, with the exception that the question asking if the plan was maintained in a U.S. territory has been removed.

Schedule SB

The instructions have been revised relating to Line 27 of the Schedule SB, applicable to Cooperative and Small Employer Charity (CSEC) plans. The instructions include additional guidance relating to the application of the Cooperative and Small Employer Charity Pension Flexibility Act, Pub. L. No. 113-97 (CSEC Act).

Administrative penalties

The new maximum penalty that can be assessed by the DOL for failure to file a complete or accurate Form 5500 has been increased to $2,063 per day. Previously, the DOL could assess penalties of up to $1,100 per day.

This penalty is assessed under ERISA section 502(c)(2), as amended by the Federal Civil Penalties Inflation Adjustment Act Improvements Act of 2015 (Inflation Adjustment Act) (Pub. L. No. 114-74; 129 Stat. 599), and the DOL’s implementing regulations (81 Fed. Reg. 43430 (July 1, 2016)). The increased penalty would be applicable for any civil penalties assessed after August 1, 2016, for violations occurring after November 2, 2015 (the date of enactment of the Inflation Adjustment Act). Beginning in 2017, it is anticipated that the DOL will adjust the new ERISA Title 1 penalty amount annually, no later than January 15 of each year, as required by the Inflation Adjustment Act.

Plan Administrators remain eligible for reduced penalties by filing under the Delinquent Filer Voluntary Compliance Program (DFVC), as long as the return is filed prior to the DOL issuance of a Notice of Intent to assess a penalty.

If you have questions about how these changes affect your plan, or if you would like assistance filing a Form 5500, please contact a member of our Employee Benefits Consulting Group.