The U.S. Treasury Department has announced that interest rates tied to several estate-planning techniques will be set at close to their lowest point in 10 years. At the same time, equities and other investment holdings are experiencing a decline from record-high values. This combination of market volatility and low interest rates create an opportunity for high-net-worth individuals. Now is an optimal time to consider strategies to manage the tax impact on your estate and family business transitions.

While the Tax Cuts and Jobs Act of 2017 temporarily increased the amount individuals can distribute free of federal estate taxes at death ($11,580,000 in 2020), the top rate on estates subject to the federal estate tax is still 40%. By taking steps today, you can lock in benefits and plan ahead with more certainty.

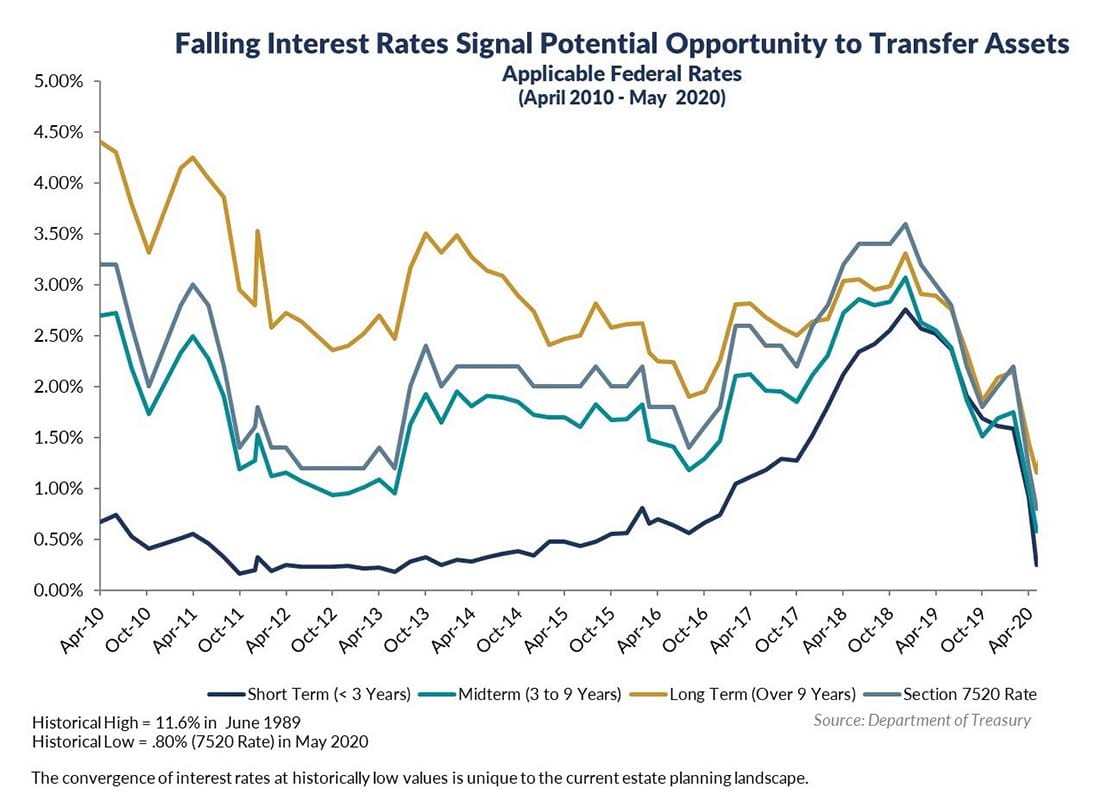

Interest-rate-based wealth transfer strategies range from relatively basic, such as low-interest intrafamily loans, to more complex uses of irrevocable trusts such as grantor-retained annuity trusts (GRATs).

Intrafamily loans

If your estate is large enough to trigger estate taxes when you die, an intrafamily loan to your children or other family members during your lifetime could transfer some of the appreciation in asset value outside of your taxable estate. Until 2026, estates for single individuals will be subject to tax if they exceed $11.58 million. Married couples get a $23.16 million exemption from estate tax under current law. On Jan. 1, 2026, if the law isn’t changed in the interim, the exemption will be reduced to an amount calculated by indexing $5 million, $10 million for married couples, for inflation occurring after 2011.

For instance, if you hold onto $1 million in assets for the next 10 years, the increase in value of those assets will still be in your estate at the end of the term. If you loan that $1 million now to someone who would otherwise inherit it, you would have to charge them 1.15% interest, based on May 2020 rates, for tax purposes. Any amount of return the borrower earns above the interest charged is, in effect, a transfer of the appreciation of the $1 million during your lifetime. At the end of 10 years, your estate would have the $1 million plus the interest earnings, but any additional return above 1.15 percent would now be in the hands of your beneficiary.

The combination of currently low-valued assets and low interest rates makes today an especially valuable time to consider an intra-family loan. As assets are poised to increase in value grow over time, more wealth in excess of the low interest rate can be transferred to the borrower/beneficiary.

Under certain circumstances, existing intrafamily loans can be replaced with new loans using today’s low rates. In these cases, the prior loan balance can be consolidated into a new loan, so little changes for the borrower/beneficiary.

Grantor-retained annuity trusts

GRATs provide a similar opportunity to transfer appreciation of assets to future beneficiaries during the grantor’s lifetime. This type of trust offers a few additional advantages when compared to an intrafamily loan, such as:

- No current income tax effect. The loan option above generates interest income to the lender, whereas the trust plan doesn’t create any additional income to the donor.

- Little to no lifetime gift exemption. Using a portion of a donor’s marketable securities, a GRAT can be used to transfer appreciation of those securities during the term of the trust to beneficiaries. Depending on the securities and the duration of the trust term, which can be as short as two years, a donor can transfer many times the value of the actual lifetime gift.

- No risk to you or the beneficiaries. If the securities decline in value during the term of the trust, you can simply take the property back at the end of the trust’s existence without any adverse consequences to the beneficiary/ies. The only consequence to you as the donor is the cost of creating the GRAT.

To create a GRAT, place assets — usually some type of marketable securities — into a trust for a specific time period. The trust pays a fixed-dollar amount back to you over the course of its existence. In order to reduce the effect of the gift tax at the time the trust is created, plan the payments over the life of the trust to return the amount you invested as well as some appreciation, calculated using a rate set by law (the Section 7520 rate). As long as you have survived the term of the trust, what hasn’t been paid back to you by the end of the trust’s term is distributed to the trust’s beneficiaries. They get the excess shares in the securities at your cost basis.

GRATs provide a helpful way to begin distributing earnings on your investments to your beneficiaries during your lifetime, while keeping the assets themselves at your disposal.

As with intrafamily loans, there may be planning opportunities for existing GRATs. For GRATs that have experienced significant value decline due to market volatility, you may have the option to substitute GRAT assets with cash or other easy-to-value assets. Then, you can redeploy the equities in a new GRAT using the lower interest rate.

In conclusion

The economy is at an important juncture when it comes to asset values and interest rates. When you look back decades, today’s rates are comparatively low — but they won’t stay this low. These strategies become less effective with each new rate hike. There’s no time like the present to evaluate your wealth and family-business transfer plans to see if these interest-based strategies make sense for you.

As always, if you have any questions, feel free to reach out.