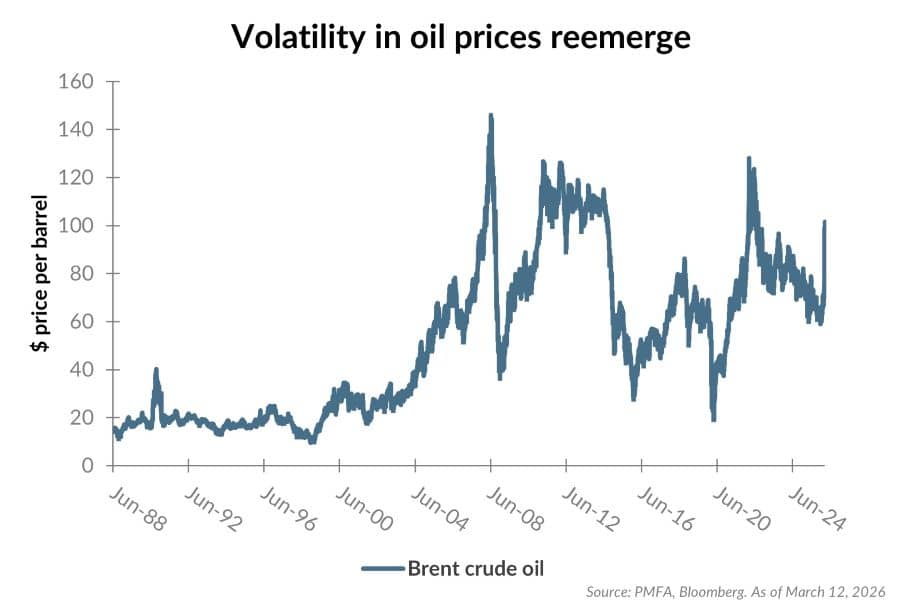

Oil markets are no stranger to volatility, but the past several weeks have underscored how quickly geopolitical risk can translate into price action. Brent crude has repriced dramatically — surging well above $100 per barrel and briefly approaching $119 — only to retrace in response to evolving headlines focused on shipping access, releases from global petroleum reserves, and the expected duration of disruptions. More recently, prices have rebounded again as the conflict widens and efforts to alleviate upward pressure on prices continue to emerge.

At the center of the volatility is the Strait of Hormuz, as we discussed recently, a narrow maritime passage linking the Persian Gulf to global markets. About one-fifth of global oil supply (and a large share of seaborne trade from key gulf producers) typically transits this corridor, which is why even the risk of disruption can move prices quickly. That sensitivity has been on full display, following an effective closure of the strait for most vessels in recent weeks, and conflicting signals on potential military escorts and a general lack of clarity on any reasonable timeline for reopening the passage, in turn driving abrupt repricing for crude oil.

From a macro perspective, the United States is meaningfully better positioned today to absorb an oil shock than has been the case since potentially the early 1950s. Domestic energy production has surged in the past two decades as shale-related production more than doubled from 2008 to 2019, making the United States a net exporter of energy and significantly less dependent on Middle Eastern supply. In fact, only 6% of U.S. crude oil imports come through the Strait of Hormuz. Most of the energy traversing the strait is destined for Asian markets. That said, the oil market is still global, and while Brent Sea Crude prices (from sources in the Middle East) have risen sharply on supply disruption, West Texas Intermediate oil prices have also surged. The result is that U.S. consumers are still feeling the impact at the pump, while higher energy prices also feed into other products and services and deliver a broader economic impact.

In the near term, inflation is where the transmission risk is most acute. The latest CPI report showed headline inflation holding at 2.4% year over year and core CPI at 2.5% year over year, with the energy index up 0.6% month over month (even before the most recent oil surge was fully reflected in the data.) Sharply rising energy costs are one of the most notable catalysts that could cause inflation to rapidly reaccelerate in the near term. It can also lift near-term inflation expectations as households and businesses respond to higher fuel and transportation costs and adjust their spending accordingly. While policymakers have attempted to dampen near-term price pressures, announcing a planned release of 172 million barrels from the Strategic Petroleum Reserve as part of a coordinated global 400-million-barrel International Energy Agency (IEA) release, these efforts are only a short-term stopgap. Ultimately, the duration of the conflict and the resulting shipping disruption will matter more to the longer-term impact on energy prices.

Against this backdrop, the implications for monetary policy warrant close examination. The Fed’s latest projections imply one interest rate cut in 2026, with Chair Powell suggesting that it’s too soon to fully assess the impact of higher oil prices. With a rising energy-driven inflation risk premium, markets will continue to adjust their view on the future rate path — particularly as energy costs begin to seep more clearly into broader inflation measures.

Periods like this reinforce a few timeless investment principles:

- Diversification matters. Concentrated bets, whether on energy, interest rates, or specific sectors or asset classes, can amplify volatility when headlines and sentiment shift quickly. Broad diversification allows a portfolio to remain anchored and resilient over the long run, despite short-term market turbulence.

- Keep a long-term focus. Geopolitical shocks often create sharp short-term volatility, but more durable economic fundamentals tend to matter more over time. When headlines become a dominant driver of the immediate market narrative, it’s important for investors to reset their perspective toward a strategic, longer-term view and maintain a disciplined approach.

- Maintain adequate liquidity. Ensuring near-term cash needs are met can allow portfolios to better navigate periods of heightened volatility.

Past performance does not guarantee future results. All investments include risk and have the potential for loss as well as gain.

Data sources for peer group comparisons, returns, and standard statistical data are provided by the sources referenced and are based on data obtained from recognized statistical services or other sources believed to be reliable. However, some or all of the information has not been verified prior to the analysis, and we do not make any representations as to its accuracy or completeness. Any analysis nonfactual in nature constitutes only current opinions, which are subject to change. Benchmarks or indices are included for information purposes only to reflect the current market environment; no index is a directly tradable investment. There may be instances when consultant opinions regarding any fundamental or quantitative analysis may not agree.

Plante Moran Financial Advisors (PMFA) publishes this update to convey general information about market conditions and not for the purpose of providing investment advice. Investment in any of the companies or sectors mentioned herein may not be appropriate for you. You should consult a representative from PMFA for investment advice regarding your own situation.