The bottom line

- By virtually any measure, consumers aren’t simply disappointed with the economy, they’re depressed. They’re feeling the impact of resurgent inflation pressures, and they’re increasingly pessimistic that conditions will improve soon.

- The impact is increasingly moving beyond the near-term challenges but are becoming more deeply embedded in the collective consumer psyche.

- Long-term inflation expectations continue to rise — a reality that creates additional risk for Fed policymakers seeking to provide reassurance that they have both the tools and resolve to fulfill their price stability mandate.

- As new Fed Chief Kevin Warsh assumes leadership today, reaffirming the Fed’s credibility, recommitting to the Fed’s dual mandate, and guiding policy with a steady hand steered toward the achievement of those goals will be crucial to reestablishing consumer trust that inflation will normalize sooner rather than later.

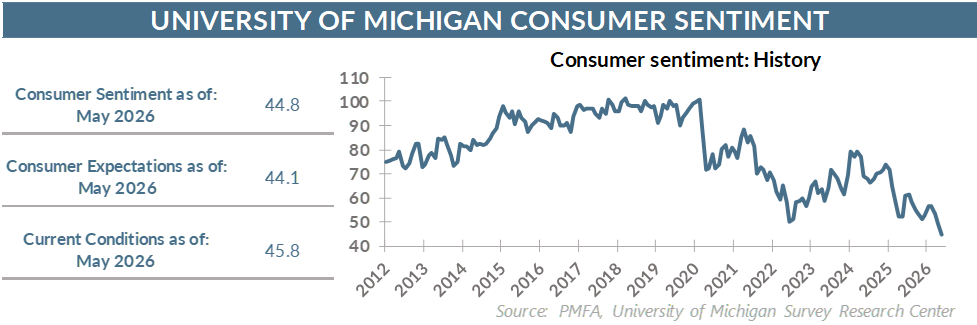

By the numbers

- The University of Michigan’s Consumer Sentiment Index fell more than expected to 44.8 in May, plumbing depths for the index seldom seen in its history.

- The Index of Current Economic Conditions dropped sharply from April’s 52.5 reading to just 45.8 in May. The accompanying index focused on expectations also dipped from 48.1 last month to 44.1.

- This May results continued the downward trajectory from the December 2024 peak of 74.0, highlighting a sustained erosion in consumer confidence that’s now persisted for more than a year and continues to push measures of the collective consumer mood to historic lows.

Broad thoughts

- The consumer mood was already tenuous before the sharp escalation in the conflict with Iran, but its impact both psychologically and economically have taken a toll. The recent decline in sentiment can be tied directly to the disruption in the flow of oil through the Strait of Hormuz and resulting spikes in gasoline and other energy costs.

- Inflation has been a challenge in recent years, but few goods or services are subject to the daily scrutiny or attention as the price of gasoline. Consumers feel it every time they stop to fill their tanks, but they watch the price fluctuate daily as they travel. It’s hard to miss, and it carries more psychological weight than price increases for many other products.

- That’s particularly true for lower- and middle-income households where the cost of essentials like gasoline represents a larger portion of their spending budget.

- It’s that reality that’s coloring the mood for investors, weighing heavily despite constructive labor market conditions and an economy that has held up surprisingly well in growth territory despite the challenge posed by inflation to household spending.

- Also notable is the meaningful increase in long-term inflation expectations, which reached 3.9% — well above its range in recent years despite inflation then reaching its highest level in decades.

- The fact that consumers are increasingly surrendering to the belief that price volatility isn’t a short-term issue and that a higher inflation regime may be at the doorstep shouldn’t be overlooked.

- Negativity concerning the long-term inflation outlook could signal a loss of faith that the Fed has the tools or ability to rein in inflation toward its stated 2% target. That creates a credibility gap that incoming Fed Chair Warsh will need to address as he charts the direction for the central bank under his leadership.

- A much more pessimistic inflation outlook may also have a more meaningful impact on the balance between consumer spending and perceived need to save for the future.

- The near-term impact on household discretionary spending will be worth watching closely. Trading down to stretch household budgets might help to bridge the gap for some consumers, while others will undoubtedly have to further curtail discretionary spending as the cost of necessities continue to rise.

Past performance does not guarantee future results. All investments include risk and have the potential for loss as well as gain.

Data sources for peer group comparisons, returns, and standard statistical data are provided by the sources referenced and are based on data obtained from recognized statistical services or other sources believed to be reliable. However, some or all of the information has not been verified prior to the analysis, and we do not make any representations as to its accuracy or completeness. Any analysis nonfactual in nature constitutes only current opinions, which are subject to change. Benchmarks or indices are included for information purposes only to reflect the current market environment; no index is a directly tradable investment. There may be instances when consultant opinions regarding any fundamental or quantitative analysis may not agree.

Plante Moran Financial Advisors (PMFA) publishes this update to convey general information about market conditions and not for the purpose of providing investment advice. Investment in any of the companies or sectors mentioned herein may not be appropriate for you. You should consult a representative from PMFA for investment advice regarding your own situation.