The bottom line: Little impact from surprisingly positive report

- The March employment report doesn’t really change the broader narrative that’s prevailed in recent months. Growth has slowed, labor conditions have cooled, and inflation is poised to move in the wrong direction, raising the stakes for the Fed.

- One month of better-than-expected hiring won’t change that narrative, doesn’t address the primary risk to the economy, and won’t assuage investor concerns.

- If there’s a silver lining, it’s that employers that still appear relatively stoic in the face of uncertainty. Layoffs remain quite low, keeping the labor market in a delicate balance.

By the numbers: March hiring pace was strong, but rosier than the reality

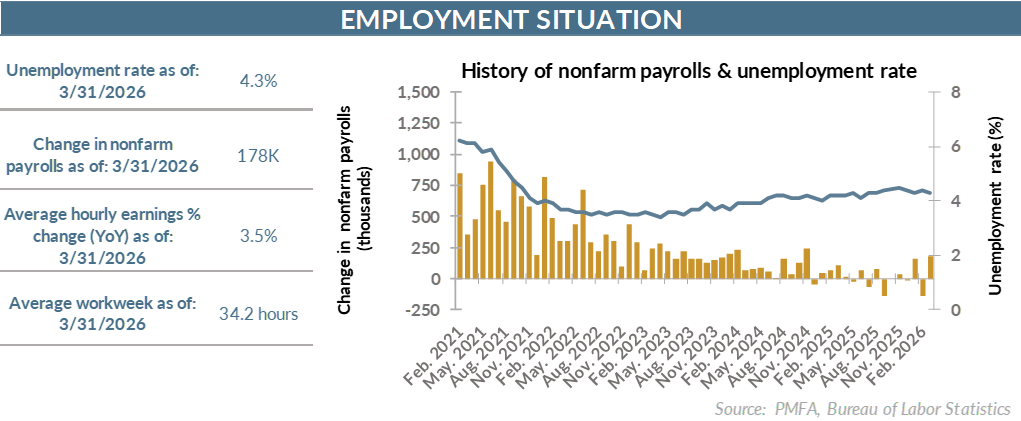

- Unemployment eased modestly to 4.3% from 4.4% in March, with the improvement largely driven by a continued decline in labor force participation. The number of employed individuals moderately declined, according to the household survey upon which the unemployment rate is calculated.

- The employer survey provided a much stronger picture of the hiring backdrop last month. Nonfarm payrolls rose by a better-than-expected 178,000 — the strongest single-month result since December 2024. Revisions to the prior two months shaved 7,000 jobs from previously reported estimates.

- The magnitude of the monthly gain, while surprisingly positive, likely overstates the actual strength of the underlying hiring trend. More than half of the gain came from the healthcare sector, which benefited from the return of previously striking workers.

- The three-month average suggests some firming in underlying hiring conditions, although near-term hiring could be dampened as the impact of the war in the Middle East continues to weigh on sentiment.

- Also notable — and critical to the easing in the jobless rate — is a continued erosion in labor force participation, which slipped to 61.9% in March. Workers have been dropping out of the labor force since last fall, with that slippage slicing 0.6% from participation since November. The impact of that trend shouldn’t be overlooked. Had participation simply held steady since November, the unemployment rate would have topped 5% in the past few months.

Market impact: Good news, but investors are focused elsewhere

- Against a different backdrop, the market impact of the positive headline numbers in the March jobs report might be more notable. Against the current one, the report is much more likely to be quickly lost in the flow of news and buried under more pressing investor concerns.

- With global energy prices surging and the geopolitical landscape still tenuous, a solid jobs report won’t address investors’ predominant concerns or embolden risk-taking.

- Earnings season is now rapidly approaching; expectations for softer growth and higher inflation are already factored in. Even so, investors remain focused on the Middle East conflict. Hopes for a quicker resolution persist, but optimism has dimmed as conditions in the region remain highly unstable and the risk of further escalation in the coming weeks appears to be rising.

- The result is that the positive jobs report may provide a brief respite, but with the recognition that the near-term hiring outlook could be dimmed by consumers curbing spending in the near term.

- All things considered, a very restrained reaction by investors of “that’s nice, but…” isn’t surprising.

Federal Reserve: Growing inflation risk complicates Fed rate calculus

- The March jobs report changes little if anything for the Fed. The softening in the labor economy over the last year was the Fed’s primary rationale for trimming policy rates last fall, but with inflation pressures building and the risk that inflation expectations move higher should higher oil prices be sustained, Fed policymakers can’t afford to ride to the rescue should growth and hiring falter.

- Policymakers appear to be willing to look through a temporary surge in energy prices, instead focusing on the flow-through effect into core inflation. The impact there should be muted compared to spiking gas prices, but still sufficiently meaningful to raise the stakes for policymakers.

- Much will hinge on the evolution of the conflict itself, the stickiness of crude oil prices at current levels, and the risk that prices could rise further if the disruption in the flow of product becomes protracted. An extended surge in energy prices will change the outlook for growth, inhibiting consumption and raising input costs for many industries to varying degrees.

- A one-two punch of higher, stickier inflation, coupled with slower growth and weaker hiring, will increasingly pinch the Fed as whiffs of stagflation strengthen.

- Massive structural changes in the U.S. economy in recent decades significantly mitigates the risk of a 1970s-style stagflation. Even so, the Fed could easily be looking at a convergence of conditions that will challenge their ability to execute monetary policy within the context of their price stability/full employment dual mandate. That alone will require the Fed to be patient and constrain the ability of policymakers to deliver a rate cut in the near term.

Past performance does not guarantee future results. All investments include risk and have the potential for loss as well as gain.

Data sources for peer group comparisons, returns, and standard statistical data are provided by the sources referenced and are based on data obtained from recognized statistical services or other sources believed to be reliable. However, some or all of the information has not been verified prior to the analysis, and we do not make any representations as to its accuracy or completeness. Any analysis nonfactual in nature constitutes only current opinions, which are subject to change. Benchmarks or indices are included for information purposes only to reflect the current market environment; no index is a directly tradable investment. There may be instances when consultant opinions regarding any fundamental or quantitative analysis may not agree.

Plante Moran Financial Advisors (PMFA) publishes this update to convey general information about market conditions and not for the purpose of providing investment advice. Investment in any of the companies or sectors mentioned herein may not be appropriate for you. You should consult a representative from PMFA for investment advice regarding your own situation.