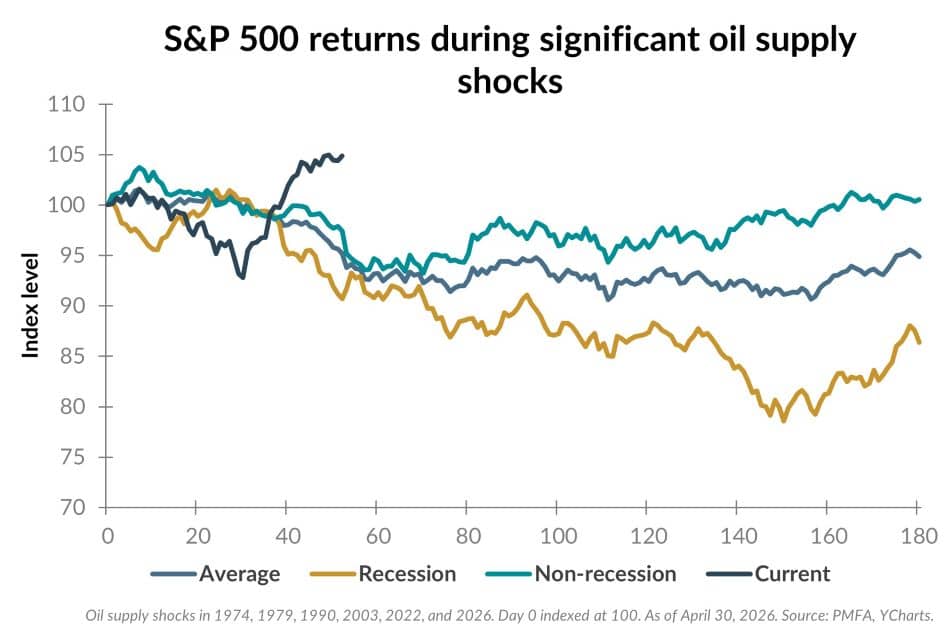

Global stock markets have shown notable resilience amid the Middle East tensions, defying historical precedent in recent weeks as equity markets have reached new highs. While stocks often absorb geopolitical shocks, periods marked by major oil supply disruptions such as the 1970s oil embargoes or the 1990 Gulf War have tended to produce weaker outcomes.

To provide context, we illustrate market performance during prior oil supply shocks, distinguishing between recessionary and non-recessionary outcomes — a key driver of equity outcomes. Although momentum toward a potential resolution appears to be building, a prolonged disruption into the summer could introduce additional downside pressure. Though notably, even these historical periods were followed by recovery rather than lasting structural damage.

Of course, the economy has evolved over time, and today’s environment differs meaningfully from past oil crises. As we highlighted last month, the U.S. economy is far less energy-dependent than in prior decades, muting the impact of higher oil prices on domestic growth. Moreover, equities continue to be supported from solid fundamentals and upward revisions to earnings expectations for 2026, as we discuss in our accompanying piece.

The key takeaway is one of perspective and discipline. While geopolitical risks can drive short-term volatility, the market’s resilience reinforces the importance of staying diversified and focused on long-term, strategic objectives as a foundation for one’s investment plan.

Past performance does not guarantee future results. All investments include risk and have the potential for loss as well as gain.

Data sources for peer group comparisons, returns, and standard statistical data are provided by the sources referenced and are based on data obtained from recognized statistical services or other sources believed to be reliable. However, some or all of the information has not been verified prior to the analysis, and we do not make any representations as to its accuracy or completeness. Any analysis nonfactual in nature constitutes only current opinions, which are subject to change. Benchmarks or indices are included for information purposes only to reflect the current market environment; no index is a directly tradable investment. There may be instances when consultant opinions regarding any fundamental or quantitative analysis may not agree.

Plante Moran Financial Advisors (PMFA) publishes this update to convey general information about market conditions and not for the purpose of providing investment advice. Investment in any of the companies or sectors mentioned herein may not be appropriate for you. You should consult a representative from PMFA for investment advice regarding your own situation.

© 2025 YCharts, Inc. All rights reserved, The information contained herein: (1) is proprietary to YCharts, Inc. and/or its content providers; (2) may not be copied, reproduced, retransmitted, or distributed; and (3) is provided “AS IS” with all faults and is not warranted to be accurate, complete, or timely. YCHARTS, INC. AND ITS CONTENT PROVIDERS EXPRESSLY DISCLAIM, TO THE FULLEST EXTENT PERMITTED BY APPLICABLE LAW, ANY WARRANTY OF ANY KIND, WHETHER EXPRESS OR IMPLIED, INCLUDING WARRANTIES OF MERCHANTABILITY, FITNESS FOR A PARTICULAR PURPOSE, ACCURACY OF INFORMATIONAL CONTENT, OR ANY IMPLIED WARRANTIES ARISING OUT OF COURSE OF DEALING OR COURSE OF PERFORMANCE. Neither YCharts, Inc. nor its content providers are responsible for any damages or losses arising from any use of this information. Past performance is no guarantee of future results.