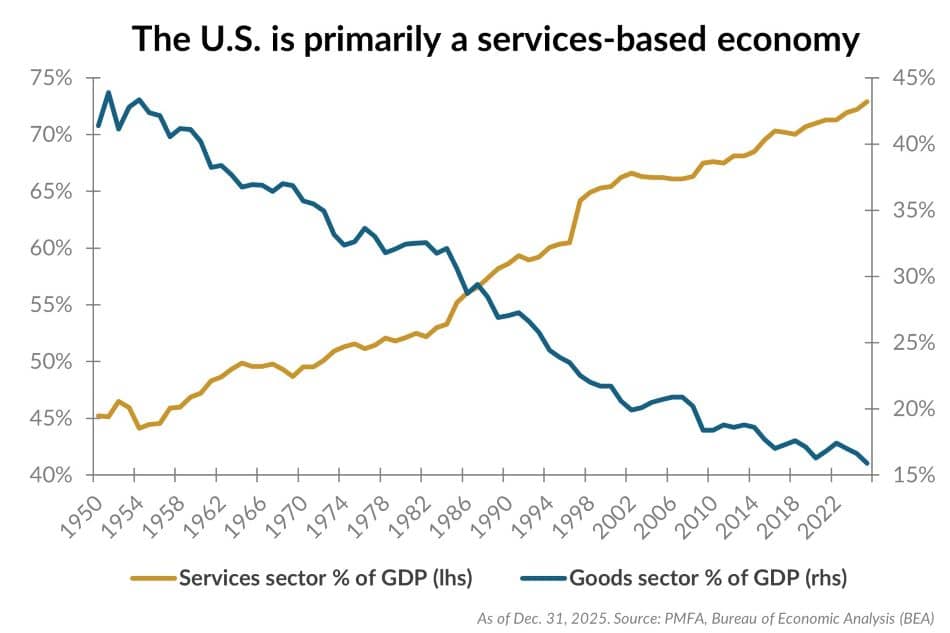

While manufacturing once sat at the core of the economy, growth today is overwhelmingly driven by services. Services‑producing industries now account for 70–80% of U.S. GDP on a value‑added basis, reflecting the growing importance of sectors such as healthcare, professional services, finance, and technology.

A services-oriented economy is more asset-light and less energy-intensive than one dominated by manufacturing. As efficiency has improved and services have grown as a share of output, the energy required to produce a dollar of output has fallen sharply, leaving the economy far less sensitive to energy price shocks than in the 1970s and 1980s. At the same time, advances in fracking have reshaped the U.S. energy landscape, positioning the country as the world’s largest crude oil producer and a net oil exporter. As a result, higher energy prices can stimulate domestic energy production, helping to offset the impact elsewhere in the economy.

This context matters amid oil price volatility stemming from conflict in the Middle East, particularly concerns over disruptions in the Strait of Hormuz, which is a critical choke point for global supply but not for U.S.-specific energy flows. While higher global energy costs still flow through to the U.S. economy, via transportation, utilities, and consumer prices, the overall macroeconomic impact is more muted than in the past. Consistent with this, corporate earnings expectations outside the energy sector have remained firm since the onset of the Iran conflict, suggesting that higher oil prices haven’t yet meaningfully disrupted the broader profit outlook. The resilience of non-energy earnings expectations reinforces the view that today’s U.S. economy is better insulated from energy-driven shocks.

The bottom line is that global shocks and distributional effects still matter, but lower energy intensity and a diversified services base have made U.S. economic growth less tightly linked to traditional energy and manufacturing cycles. That said, ongoing geopolitical risks could still introduce market volatility and lead to tighter financial conditions — particularly the longer tensions persist. For investors, this underscores the importance of balancing awareness of near-term risks with a longer term perspective. Maintaining diversification, aligning portfolios with long term objectives, and avoiding reactive decisions remain critical.

Past performance does not guarantee future results. All investments include risk and have the potential for loss as well as gain.

Data sources for peer group comparisons, returns, and standard statistical data are provided by the sources referenced and are based on data obtained from recognized statistical services or other sources believed to be reliable. However, some or all of the information has not been verified prior to the analysis, and we do not make any representations as to its accuracy or completeness. Any analysis nonfactual in nature constitutes only current opinions, which are subject to change. Benchmarks or indices are included for information purposes only to reflect the current market environment; no index is a directly tradable investment. There may be instances when consultant opinions regarding any fundamental or quantitative analysis may not agree.

Plante Moran Financial Advisors (PMFA) publishes this update to convey general information about market conditions and not for the purpose of providing investment advice. Investment in any of the companies or sectors mentioned herein may not be appropriate for you. You should consult a representative from PMFA for investment advice regarding your own situation.