Editor’s note: Please see our 2026 meals and entertainment article for the most recent information.

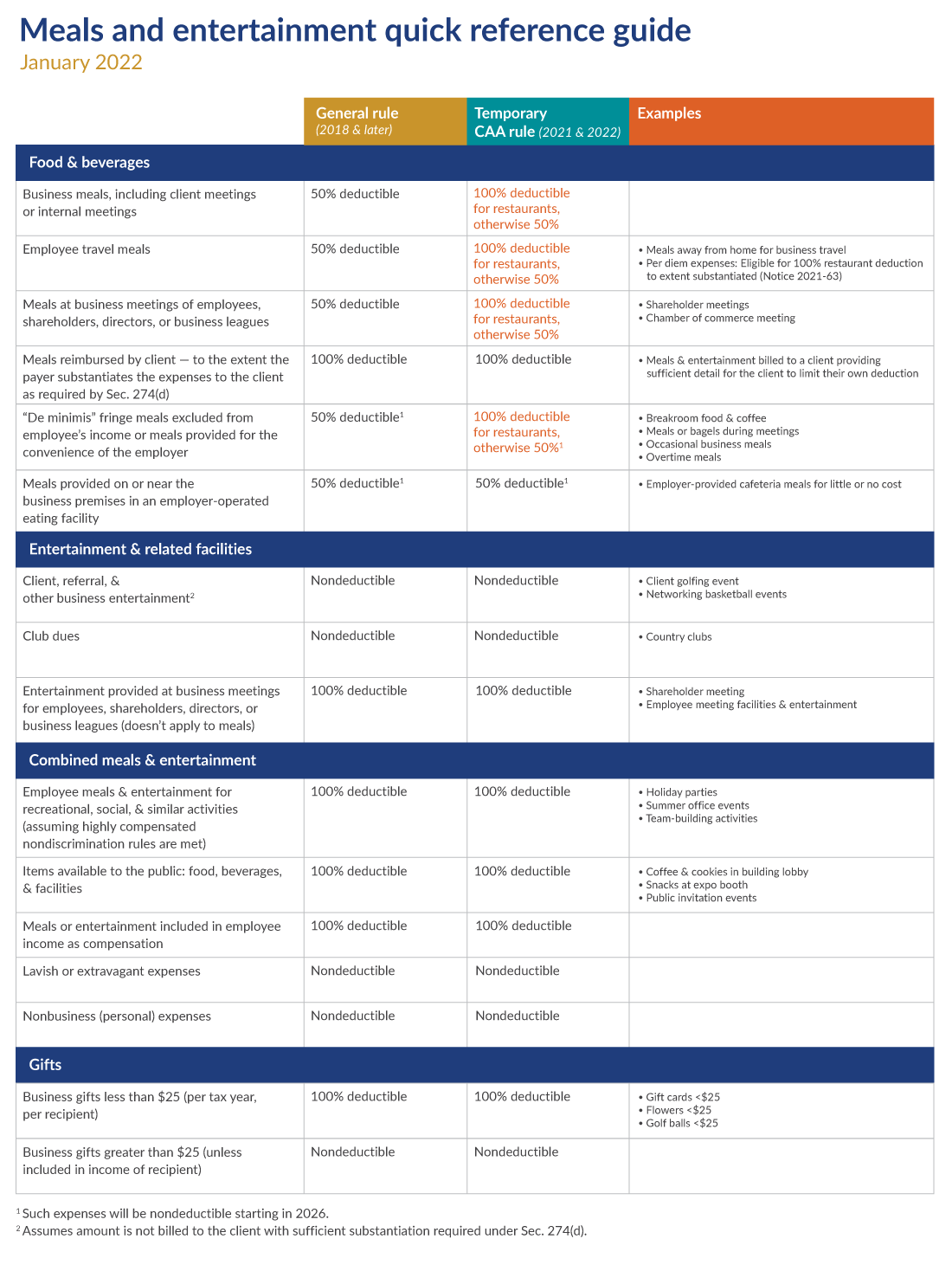

Over the past several years, there have been numerous changes to the deductibility of meals and entertainment expenses. As part of the 2018 tax reform created by the Tax Cuts and Jobs Act (TCJA), Congress made several significant changes to the deductions for meals, entertainment, and employee fringe benefits, including making business entertainment expenses entirely nondeductible and reducing the deduction for most meals to 50%. Since the enactment of the TCJA, important changes have been made to increase tax deductions for some meals expenses from 50 to 100%. Below, we summarize the changes since the enactment of the TCJA and what they mean for taxpayers’ businesses.

What has changed with meals and entertainment deductions?

Following the enactment of the TCJA, which largely disallowed entertainment deductions and reduced most meal expense deductions to 50%, administrative and regulatory guidance has clarified how taxpayers should apply these changes. The Consolidated Appropriations Act, 2021 (the CAA) enacted additional temporary changes to the rules for deducting meals provided by a restaurant.

Modifications to restaurant meals deductions

In an effort to help the restaurant industry during the economic fallout of the COVID-19 pandemic, additional changes to meals and entertainment deductions were enacted through the CAA. For costs paid or incurred during the 2021 and 2022 calendar years, businesses may claim a deduction for 100% of the cost of meals provided by a restaurant. The temporarily enhanced deduction doesn’t apply to entertainment, which remains a disallowed deduction.

IRS guidance on restaurant meals deductions

Following the enactment of the CAA, the IRS released Notice 2021-25 and Notice 2021-63 to provide taxpayers with additional guidance on applying the temporary 100% meals deduction. Meal expenses that don’t qualify for the 100% deduction still qualify for a 50% deduction as was previously allowed.

For purposes of the temporary 100% meals deduction, the meal must be provided by a restaurant. Notice 2021-25 provides that a “restaurant” includes “a business that prepares and sells food or beverages to retail customers for immediate consumption, regardless of whether the food or beverages are consumed on the business’s premises.” Businesses that primarily sell prepackaged foods not for immediate consumption — including a grocery store, liquor store, convenience store, drug store, specialty food store, newsstand, or a vending machine or kiosk — are not considered restaurants. Expenses related to eating facilities located on the business premises of the employer or employer-operated eating facilities are not permitted the enhanced 100% deduction, even if the facility is operated by a third party under contract with the employer. However, meals bought from outside restaurants and brought on premises for employee meetings, for example, would often qualify for full tax deductibility.

Most recently, the IRS issued Notice 2021-63, which addressed questions regarding the application of the temporary 100% deduction to per diem expenses. The Notice provides that taxpayers may treat the meal portion of a per diem rate or allowance as 100% deductible if the taxpayer meets the requirements to substantiate the expense, and the expense otherwise qualifies for the temporary 100% meals deduction.

Final regulations on TCJA changes

In October 2020, final regulations were released to guide taxpayers in applying the TCJA meals and entertainment deduction rules. The regulations clarify that meals expenses are not classified as disallowed entertainment expense deductions unless such expenses are incurred as part of an entertainment activity. However, meals expenses incurred as part of an entertainment activity may still be classified as a 50% deductible meals expense if they’re purchased separately from the entertainment or if the cost of the food or beverage is separately stated on the invoice. The regulations provide that the 50% meals deduction is allowed for all food and beverage expenses and reiterates the statutory requirements that the meal must not be lavish or extravagant, and the taxpayer or the taxpayer’s employee must be present when the meal is provided. Incidental costs associated with the meal, such as delivery fees, taxes, and tip, are also allowable expenses.

How we can help with meals and entertainment deductions

These recent changes to meals deduction expenses can benefit businesses and their employees. Most restaurant meals expenses are only 100% deductible from Jan. 1, 2021 through Dec. 31, 2022, so it’s important to take advantage of these changes while the 100% deduction is available. Our team of experts will work with taxpayers to maximize the benefits these changes can provide to taxpayers’ businesses.