Provisions enacted as part of the One, Big, Beautiful Bill Act (OBBBA) in 2025 seem targeted at alleviating concerns about downward attribution of ownership interests in non-U.S. entities that arose as a result of the Tax Cuts and Jobs Act of 2017 (TCJA). TCJA changes to Internal Revenue Code (IRC) Section 958 appeared to go farther than Congress intended toward removing safeguards against downward attribution of ownership interests in non-U.S. entities. Those changes remain in effect for tax years that begin on or before Dec. 31, 2025, so they apply to returns of calendar-year taxpayers that are being prepared in the spring of 2026. Affected taxpayers working on those returns should continue to apply the TCJA rules and consult with their tax advisors to learn how the OBBBA changes will affect their filing obligations going forward.

Downward attribution before and after TCJA

Prior to the TCJA, IRC Section 958 included subsection (b)(4), which stated that the downward attribution rules elsewhere in the IRC didn’t apply to treat a U.S. person as owning the stock owned by a non-U.S. person.

The TCJA eliminated that subsection for the last taxable year of foreign corporations beginning before Jan. 1, 2018, and each subsequent year going forward (until the OBBBA restored a revised version of 958(b)(4) protections for tax years beginning after Dec. 31, 2025). The result: Ownership by a “U.S. person” (i.e., any U.S. entity, such as a U.S. citizen or resident, a domestic corporation, a domestic partnership, etc.) of a 10% interest in a foreign parent corporation that has at least one U.S. subsidiary could trigger attribution rules between the foreign parent, the U.S. subsidiary, and any other worldwide subsidiaries. The TCJA elimination of IRC 958 subsection (b)(4) resulted in the treatment of these subsidiaries as controlled foreign corporations (CFCs) for U.S. reporting purposes. In effect, the attribution rules didn’t change so much as a piece of the law that exempted many multinational business structures from them was eliminated. At that point, even though nothing had effectively changed in the ownership structures of the businesses in question, multinational corporations with subsidiaries in different countries were subject to a new reporting requirement in the United States that few were prepared for.

The potential challenges that arose out of this downward attribution had to be understood and addressed. Existing businesses that may have failed to properly document these relationships after the law changed faced a variety of penalties. Investors looking to purchase interests in global conglomerates needed to realize that such an acquisition could trigger complicated reporting requirements and U.S. tax issues under the post-TCJA downward attribution regime. These challenges remain relevant for tax year 2025, and affected multinational businesses with U.S. tax filing obligations need to stay wary of the impact that downward attribution can have on their returns. The efforts that have been made in the OBBBA to limit the scope of the downward attribution rules will take effect for tax years beginning after Dec. 31, 2025, and those will be described a little bit later in this article.

What happened when the CFC attribution rules went into effect?

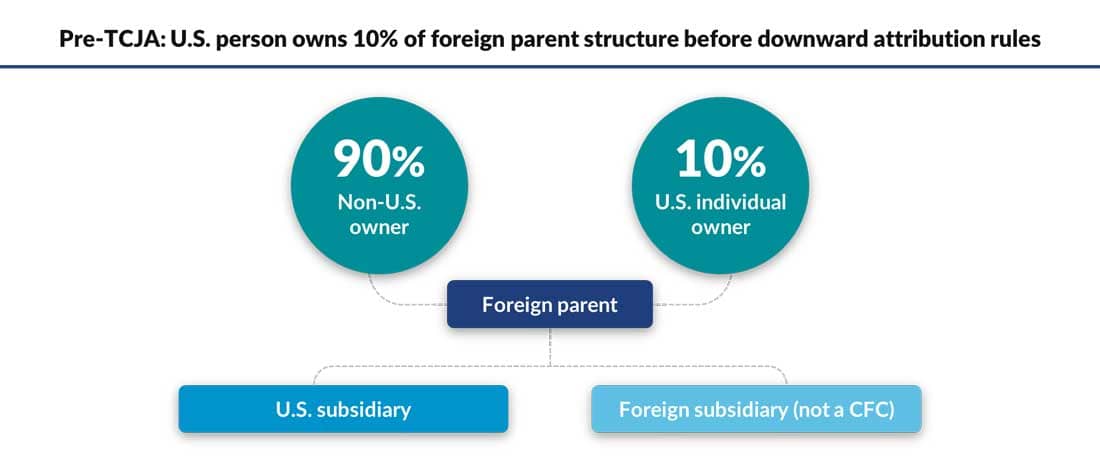

Perhaps the quickest way to illustrate the before and after is a side-by-side look at a simplified business structure. Consider a foreign parent company — 10% of that foreign parent is owned by a U.S. person. The foreign parent wholly owns one U.S. subsidiary and one non-U.S. subsidiary.

The rules in effect prior to the TCJA changes to IRC 958 protected the U.S. participants in this structure from downward attribution, i.e., the U.S. subsidiary wasn’t deemed to own assets owned by its foreign parent. Now, let’s look at the impact of the Section 958(b)(4) repeal and the resulting relationships between the entities.

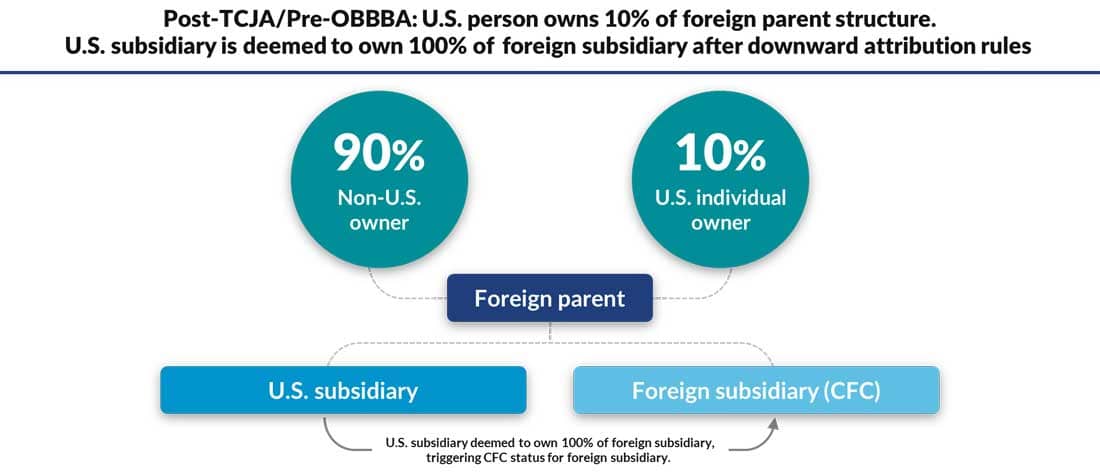

Because of the TCJA’s elimination of rules that protected U.S. persons from attribution of stock owned by non-U.S. persons, the downward attribution rules now apply to both the 10% U.S. investors in the foreign parent and the U.S. subsidiary of the foreign parent in tax years up to and including 2025. (Technically speaking, the repeal of IRC Section 958(b)(4) actually triggered downward attribution issues for all U.S. owners of the foreign parent, but the IRS provided relief in Rev. Proc. 2019-40 that limited downward attribution reporting when the foreign parent doesn’t have a 10% U.S. owner.)

The attribution rules basically tell the certain taxpayers that they’ll be substituted into the position of the foreign parent, and any interest that the foreign parent holds will be attributed to them as well. In this limited example, that makes the U.S. subsidiary of the foreign parent 100% the owner of the foreign subsidiary. This results in the foreign subsidiary being classified as a CFC, which triggers specific reporting and income inclusion requirements related to CFC stock ownership.

What happens when these entities are deemed to hold CFC stock?

In this simplified example, the change in the downward attribution rules imposed a new filing requirement on the 10% U.S. investor above the foreign parent and on the U.S. subsidiary. Because both entities were deemed to hold an interest in a CFC once the law changed and ownership was attributed to them, they needed to file IRS Form 5471, “Information Return of U.S. Persons with Respect to Certain Foreign Corporations.” That filing requirement continues for tax year 2025.

The rules impose a $10,000 fine for each U.S. person’s failure to file Form 5471 for each annual accounting period. For this very limited example, that’s $20,000 per year since 2018. Now consider multinational entities with 10% U.S. investors and dozens, if not hundreds, of foreign subsidiaries around the world. Even without any additional tax obligation, the penalties for failing to file could quickly run into the millions, especially if the taxpayer needs to consider multiple years going back to 2018 and continuing forward into 2025.

On top of the additional filing requirements (and penalties for missed filings), U.S. investors holding a 10% stake in the foreign parent could incur additional U.S. tax liabilities if they are subject to anti-deferral rules in the U.S. law under net CFC tested income (NCTI) provisions, formerly known as GILTI and subpart F.

The first step toward identifying a downward attribution issue on affected returns between 2018 and 2025

Several common components of a multinational corporate structure indicate the likelihood of a downward attribution scenario under the TCJA rules. Downward attribution will likely be triggered when:

- A foreign parent company owns a U.S. subsidiary.

- That same foreign parent company has subsidiaries that it operates in other countries.

- The foreign parent company has multiple investors that are U.S. tax residents, which could include private equity funds, individuals, and other businesses.

To identify and correct problems in this area, multinational businesses with significant ownership based in the U.S. should consider these steps:

- Review the global structure of the foreign parent and its subsidiaries to identify how much of the business is owned by U.S.-based investors and determine the impact of downward attribution.

- Understand the full legal ownership of the entire structure, especially the foreign parent (knowledge of the tax residency of upper tier investors is critical).

- If downward attribution rules do apply, determine the scope of reporting and U.S. tax impact to U.S. investors.

- Certain planning strategies may be available to mitigate and/or eliminate the negative impact of downward attribution.

Because these structures existed prior to the TCJA modification without any significant reporting or tax consequences, word had been slow to travel among affected groups about this important change.

OBBBA changes: IRC Section 958(b)(4) returns and IRC Section 951B provides targeted anti-abuse rules

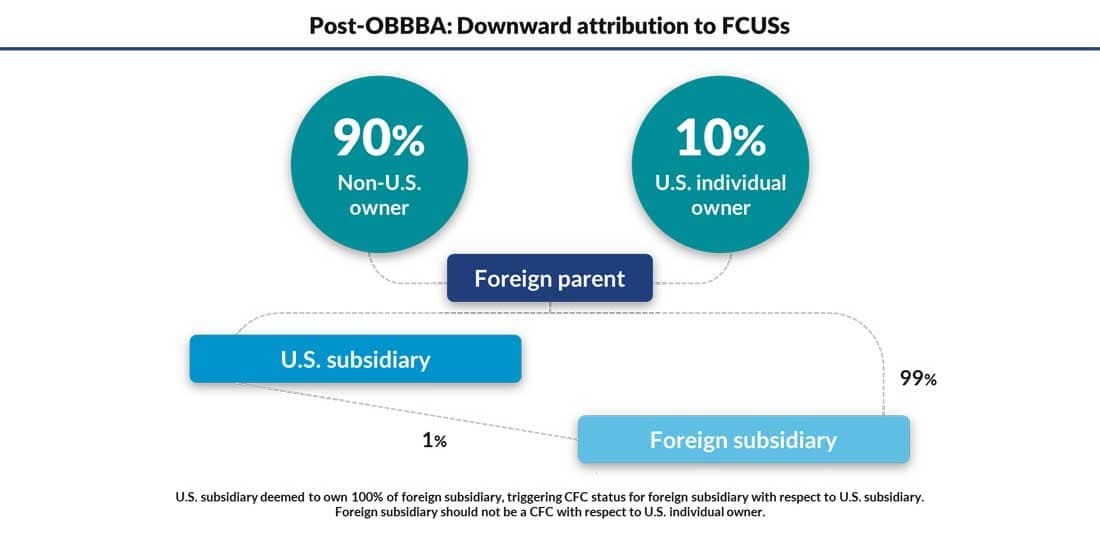

For tax years beginning after Dec. 31, 2025, the OBBBA reinstates the broader protections against downward attribution in IRC Section 958(b)(4) while instituting provisions more closely targeted to limit offshoring of income otherwise taxable in the United States. Rather than the 10% thresholds that were removed when TCJA eliminated Section 958(b)(4), the OBBBA revisions identify “foreign controlled U.S. shareholders” (FCUSs) (those who own more than 50% of a foreign corporation) and applies downward attribution to “foreign controlled foreign corporations” (FCFCs) (those that are owned more than 50% by FCUSs).

In the diagram above illustrating pre-OBBBA rules (included again for ease of reference), the OBBBA changes would end the classification of a foreign subsidiary as a CFC with respect to the U.S. 10% owner due to downward attribution. The U.S. subsidiary of the foreign parent may still have Form 5471 reporting considerations because the law deems that it has 100% constructive ownership of the foreign subsidiary since both are controlled by the foreign parent. It appears that the OBBBA changes would end potential GILTI (now NCTI)/Subpart F income tax obligations for both the U.S. individual and the U.S. subsidiary.

While additional guidance from Treasury and the IRS may be needed to clarify this concern, it’s expected that the U.S. subsidiary would have a tax obligation under the NCTI/Subpart F rules if it owned even a small percentage of the foreign subsidiary directly. For instance, in the diagram below, foreign parent owns 99% of the foreign subsidiary and U.S. subsidiary owns 1%. Under the OBBBA laws, U.S. subsidiary is now an FCUS and foreign subsidiary is an FCFC. Any direct ownership of foreign subsidiary by U.S. subsidiary could trigger the obligation because even a small percentage of direct ownership would be combined with the 100% constructive ownership.

TCJA rules apply until tax years starting after Dec. 31, 2025

Affected businesses should be aware that the broader attribution rules still apply for tax years that began in 2025. Failures to properly report attributions based on the 10% threshold will still be subject to penalties for each missed Form 5471.

Affected taxpayers filing their last returns based on the TCJA attribution rules should take the opportunity to consult with their tax advisors to understand how the new attribution rules will affect their returns for the tax years that begin in 2026 and beyond.