Hedge funds can play a role within an investor’s alternative’s allocation, namely through the addition of uncorrelated strategies that provide diversification benefits from both a risk and return standpoint. Moreover, hedge funds can utilize a broader range of investment techniques than most traditional strategies, including short selling securities, investing in nontraditional assets such as derivatives and private investments, employing leverage, or capitalizing on investments that simply can’t be owned in a liquid vehicle. These techniques may allow hedge funds to generate unique return streams with reduced sensitivity or correlation to public markets.

Hedge funds can serve as an attractive complement to an existing portfolio of stocks and bonds. As illustrated in the chart below, over the trailing 25-year period ended Dec. 31, 2023, the HFRI Fund Weighted Index, which represents hedge funds broadly, has avoided the extreme declines seen in public equities. At the same time, hedge funds have outperformed high-quality core fixed income, with a more attractive Sharpe ratio, or return per unit of risk. As such, due to the unique diversification benefits, an allocation to a diversified portfolio of hedge funds can often enhance potential returns while reducing overall portfolio volatility. The benchmark of hedge fund returns can be quite deceiving as there are thousands of hedge fund strategies with an exceptionally wide range of return/risk characteristics reflective of the breadth of strategy types. Manager performance dispersion is among the highest compared to other investment categories; therefore, getting access to the top hedge fund managers is critical. We’ll explore this topic further below

Hedge funds in various interest rate environments

The decade that followed the global financial crisis of 2008 was characterized by ultra-low policy rates and subdued market volatility. The accommodative monetary policy of the last 15 years was certainly an anomaly in the long history of financial markets. Only the period between the Great Depression and World War II had interest rates as low for an extended period before the introduction of the first hedge fund in 1949. The macro landscape drastically shifted in March 2022, as persistently rising inflation prompted the Federal Reserve to begin a rapid succession of interest rate hikes. Over the course of 18 months, the Federal Reserve raised short-term interest from 0% to over 5%, the most aggressive Fed tightening cycle in decades. A higher neutral interest rate is prompting investors to revisit asset allocation decisions as forward-looking risk and return expectations have shifted across asset classes.

Components of hedge fund cash yields:

From a structural perspective, hedge funds stand to benefit from the higher-rate environment, particularly those strategies that utilize derivatives and use short selling. Many hedge funds utilize leverage as part of their strategy to enhance potential returns. This is typically done using derivatives, which often carry low-margin requirements (a portion of notional value in cash or equity required as collateral to borrow from the broker). As a result, hedge fund strategies can often have high cash balances, which they invest in short-term cash instruments, including money market funds and treasuries. At current interest rates, these strategies are now earning over 5% on their cash, compared to near zero since 2008. However, the cost of leverage, has also risen and will offset some of the cash yield benefits for strategies that use it.

Many hedge funds also seek to profit or hedge their portfolios by “short” selling securities (or indexes) that they expect to decline in value. This technique may also be used in an attempt to reduce the risk of an existing portfolio of equities. Strategies that use short selling include equity long/short, merger arbitrage, relative value, and market neutral, among others. To establish a short position, the hedge fund manager will provide cash collateral to a lender for borrowing the security. The hedge fund is entitled to receive the interest that accrues on cash held as collateral over the period, less any dividends received on the security. This return earned on the collateral is known as the short rebate, and it can meaningfully contribute to a hedge fund’s return over time. For example, if a hedge fund has 60% gross short exposure, approximately 60% of their portfolio should be held in cash and earning the risk-free rate (currently approximately 5%). That’s before any potential gain resulting from the decline in the value of the shorted stocks and net of interest paid on the borrowed securities.

Credit strategies can also expect to have better prospective returns since the strategies tend to be long and (to varying degrees) own performing levered loans and high yields bonds, both of which are income-producing investments. Outside of the yield pickup, higher interest rate environments may also provide greater availability of stressed and distressed opportunities, a large component of the “event-driven” category.

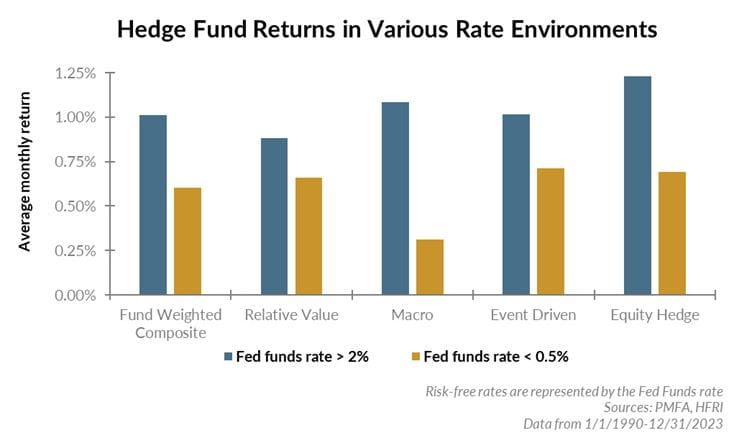

The benefits of higher yields can be illustrated through performance: the average return of hedge fund managers during periods of higher risk-free rates (defined as risk-free rates >2%) has been greater on average than periods of low risk-free rates (defined as risk-free rates <.5%). While the relative performance differential has varied, this has been true across hedge fund strategy types.

Performance dispersion among hedge fund managers:

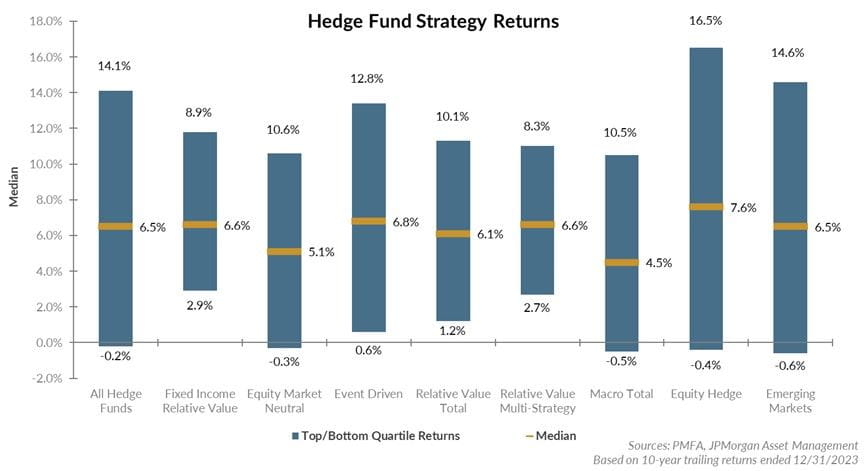

Higher-interest rate regimes are often associated with greater dispersion of asset returns; as such, manager selection remains critically important. The performance of hedge fund indices, such as the HFRI index series, can appear lackluster but reflects aggregated returns from hundreds of different strategies and managers. Individual hedge fund manager performance will vary significantly within each category. The chart below illustrates manager dispersion for the trailing 10-year period ended Dec. 31, 2023, across the broad hedge fund universe as well as across several hedge fund categories. The return variability between top- and bottom-performing managers can be attributed to differences in a manager’s skills, resources, strategy opportunity set, leverage, net exposure, and asset allocation to generate returns. Depending on the space, top quartile funds have typically produced competitive returns that have topped core bonds and closely matched or outperformed equities, generally with less volatility. While investing in hedge funds broadly can provide portfolio benefits, investors who can access top performing funds have a greater opportunity to improve portfolio performance, reduce portfolio risk, or both.

Of course, interest rates are variable, and the current rate environment will change over time. While higher rates may provide a boost to hedge fund performance, a compelling investment case for hedge funds still exists if interest rates fall. Lower rates present their own unique set of tailwinds to hedge funds, including a lower cost of borrowing, making it more attractive for hedge funds to employ leverage. Additionally, lower rate environments are generally associated with rising asset values and increased deal activity. For investors that can access hedge funds, the uncorrelated nature of these strategies relative to traditional public market strategies makes them an attractive asset class to include within a long-term investment portfolio.

Bottom line

While hedge funds may introduce additional complexity and unique risks relative to traditional investments, historically they have served as an attractive diversifier within an investment portfolio. Given their structure and composition, the higher-rate environment of today should provide one valuable tailwind to hedge fund performance. Hedge fund strategies can vary significantly by risk and return profiles, so understanding what to expect from a given manager is essential.

Past performance does not guarantee future results. All investments include risk and have the potential for loss as well as gain.

Data sources for peer group comparisons, returns, and standard statistical data are provided by the sources referenced and are based on data obtained from recognized statistical services or other sources believed to be reliable. However, some or all of the information has not been verified prior to the analysis, and we do not make any representations as to its accuracy or completeness. Any analysis nonfactual in nature constitutes only current opinions, which are subject to change. Benchmarks or indices are included for information purposes only to reflect the current market environment; no index is a directly tradable investment. There may be instances when consultant opinions regarding any fundamental or quantitative analysis may not agree.

Plante Moran Financial Advisors (PMFA) publishes this update to convey general information about market conditions and not for the purpose of providing investment advice. Investment in any of the companies or sectors mentioned herein may not be appropriate for you. You should consult a representative from PMFA for investment advice regarding your own situation.

When considering alternative investments, such as hedge funds, you should consider various risks including the fact that some hedge funds use leverage and other speculative investment practices that may increase the risk of investment loss, may execute a substantial portion of the trades executed for the fund on a foreign exchange, may have performance that is volatile, can be illiquid, are not required to provide periodic pricing or valuation information to investors, may involve complex tax structures and delays in distributing important tax information, are not subject to the same regulatory requirements as mutual funds, often charge high fees, and in many cases the underlying investments are not transparent and are known only to the investment manager. There may be restrictions on redeeming interests in the fund. Investors in hedge funds may experience performance different than that shown. Performance may be higher or lower due to a number of variables, which may include differences in incentive fees, management fees, and certain restrictions unique to the investor. Alternative investments may not be suitable for all investors. Read all offering materials before investing.

.jpg?la=en&h=307&mw=480&w=480&hash=6A627DBF766882E4EE1BC9926E34CB08)