As you prepare for recognition of opportunity zone (OZ) deferred capital gains effective Dec. 31, 2026, it’s essential to understand a little-known regulatory provision that could preclude investors in qualified opportunity funds (QOFs) whose investment has declined in value from reducing the amount of deferred gain required to be recognized. This provision applies to investors in QOFs structured as partnerships and S corporations who have received distributions or cumulative loss allocations and an allocation of liabilities on their Schedule K-1.

The Internal Revenue Code (IRC) requires investors in QOFs to reduce the amount of deferred gain recognized on Dec. 31, 2026, to the extent that the fair market value (FMV) of their QOF investment is lower than their original deferred gain. The FMV of a QOF investment can decline for numerous reasons, most obviously because the value of the underlying business has declined. However, several valuation discounts can also contribute to such a decline, specifically three discount types: lack of marketability (DLOM), lack of control (DLOC), and risk associated with real estate under construction.

Deferred gain recognition calculation regulatory guidance

The Treasury Department is responsible for issuing guidance to taxpayers to assist them in applying the tax law as enacted by Congress in the Internal Revenue Code. Such guidance often takes the form of regulations that interpret the IRC. In December 2019, the Treasury Department issued final regulations related to OZs. Included in such guidance was Treasury Regulation Section 1.1400Z2(b)-1(e)(4), which provides a “special amount includible rule” that investors in QOF partnerships and S corporations are required to use to calculate the deferred capital gain recognized on Dec. 31, 2026. Such regulation reduces and potentially eliminates the benefit of a low valuation to the extent that a partner or S corporation shareholder has received debt financed distributions or loss allocations.

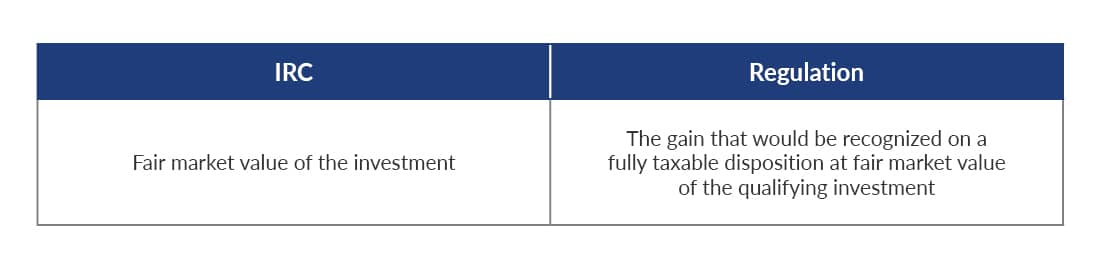

IRC vs. Treasury regulation deferred gain recognition calculation

The regulatory calculation is similar to the formula in the IRC in that both require the QOF investor to recognize the lesser of their deferred capital gain or an amount that’s tied to the FMV of their investment on Dec. 31, 2026. However, there are slight nuances between the statutory and regulatory language, which significantly impact the result depending on the facts and circumstances. Below is a comparison of the component of the calculation that references FMV.

The IRC focuses on the FMV of the investment in the QOF, whereas the regulation requires the investor to instead calculate the gain that would be recognized on a fully taxable disposition at FMV of the qualifying investment. In some cases, these calculations will produce the same result, but that’s not always the case. Per the preamble to the final OZ regulations, the intent of the special amount includible rule is to prevent QOF investors from receiving an unintended tax benefit to the extent that the investor previously received a distribution or loss allocation which was directly or indirectly financed with debt.

Examples of IRC vs. regulatory deferred gain recognition calculation

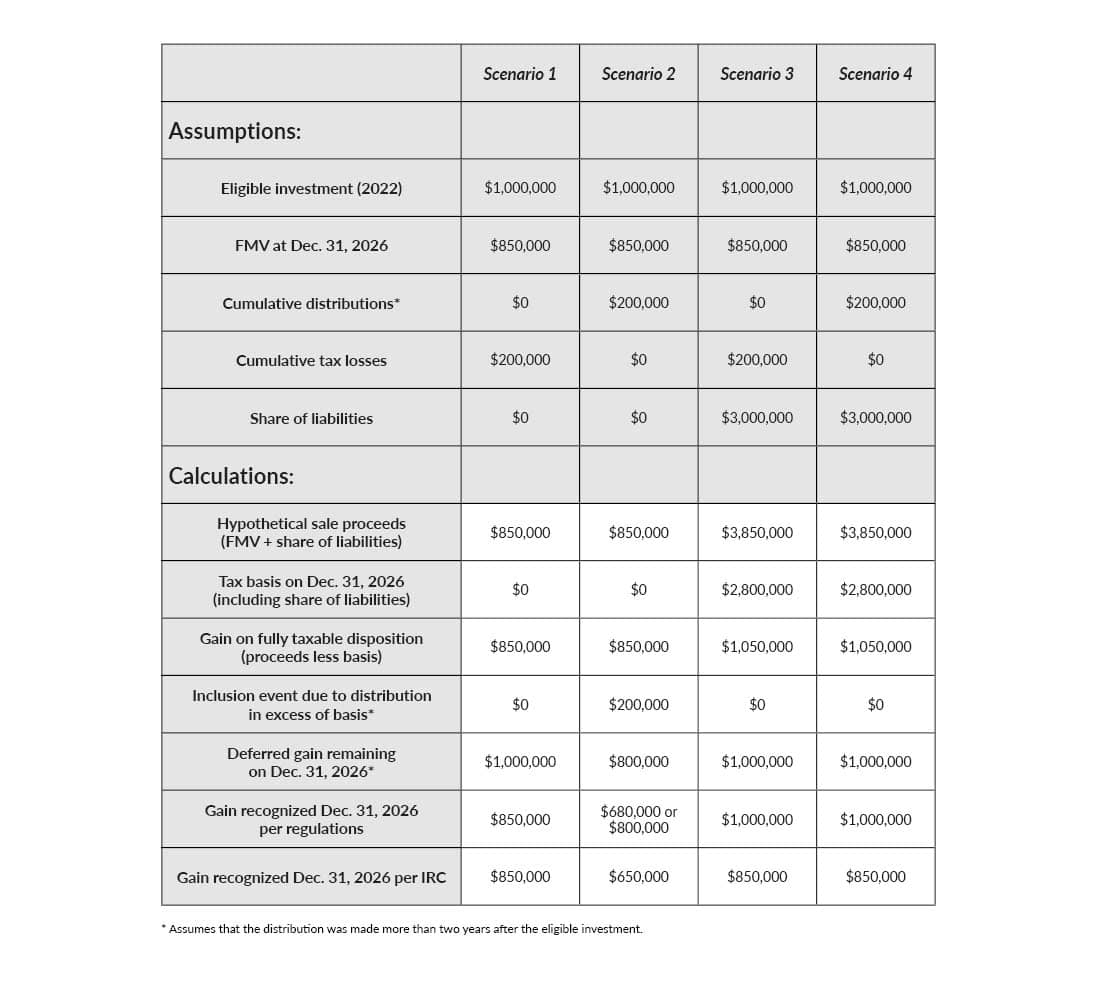

The easiest way to understand the nuances of these calculations is to walk through an example. The table below illustrates these calculations in four different situations assuming the QOF is taxed as a partnership, as follows:

- In all four situations, an eligible investment of $1,000,000 was made in 2022 and the FMV of the investment on Dec. 31, 2026 is $850,000.

- In two situations (Scenario 2 and Scenario 4), the QOF investor received cumulative distributions of $200,000 and no cumulative income/loss allocations.

- In the other two situations (Scenario 1 and Scenario 3), the QOF investor received cumulative loss allocations of $200,000 and no distributions.

- Finally, in two situations (Scenario 3 and Scenario 4), the QOF investor had an allocation of $3 million of liabilities, whereas in the other two situations (Scenario 1 and Scenario 2), the QOF investor had no allocation of liabilities.

Impact of liability allocations on regulatory deferred gain recognition calculation

These examples illustrate the impact of liabilities upon the amount of deferred gain required to be recognized on Dec. 31, 2026. In particular:

- In the scenarios where the QOF investor had an allocation of liabilities (i.e., Scenario 3 and Scenario 4), the investor is required to recognize the entire $1 million deferred gain on Dec. 31, 2026, despite the fact that the value of the investment on Dec. 31, 2026, had declined to $850,000 because the investor previously received the benefit of a distribution or tax loss allocation which exceeded the reduction in fair market value.

- In Scenario 1, where the QOF investor didn’t have a share of liabilities to provide basis to deduct the losses, the investor is able to reduce the amount of deferred gain required to be recognized on Dec. 31, 2026, to the FMV of the QOF investment equalling $850,000.

- It’s interesting to note that in Scenario 1, the QOF investor will receive tax basis on Dec. 31, 2026, upon recognition of the deferred gain that will enable the investor to deduct the cumulative $200,000 of tax losses that were previously suspended due to lack of tax basis (subject to the passive activity and excess business loss limitations).

- In Scenario 2, where the QOF investor also didn’t have a share of liabilities due to ambiguities in the regulations, it’s not clear how much gain the investor is required to recognize on Dec. 31, 2026.

- The only thing certain is that the investor won’t be required to recognize more than the $800,000 remaining deferred gain on Dec. 31, 2026, (i.e., $1,000,000 original deferred gain less $200,000 inclusion event gain recognized on the distribution in excess of basis). The formula in the IRC requires the investor to recognize $650,000 of deferred gain on Dec. 31, 2026, ($850,000 FMV less $200,000 tax basis from inclusion event gain recognized). Depending on how the regulations are interpreted, the amount of deferred gain recognized on Dec. 31, 2026, could be either $800,000 or $680,000 ($850,000 FMV x 80% which represents the percentage of the original deferred gain that was deferred until Dec. 31, 2026). It’s beyond the scope of this article to explain such possible interpretations of the regulations in this scenario.

Regulatory deferred gain recognition formula

Below is the regulatory formula that QOF partners and S corporation shareholders are required to use to calculate the amount of deferred gain to recognize on Dec. 31, 2026:

- The lesser of:

- (i) The product of:

- (A) The percentage of the qualifying investment that gave rise to the inclusion event.

- (B) The remaining deferred gain, less any basis adjustments pursuant to Section 1400Z-2(b)(2)(B)(iii) and (iv).

- (ii) The gain that would be recognized on a fully taxable disposition at fair market value of the qualifying investment that gave rise to the inclusion event.

- (i) The product of:

The regulation citations in part (i)(B) of the calculation refer to the 10% and 15% basis increase earned by a QOF investor for holding their QOF investment for at least five or seven years, respectively. The above examples don’t include a 10% or 15% basis adjustment since the eligible investment was assumed to be made in 2022. To the extent that a QOF investor qualifies for such a basis adjustment, the amount of gain required to be recognized on Dec. 31, 2026, would be reduced accordingly, since such basis adjustment is included in both parts of the calculation in the regulations (i.e., in (i)(B) by specific reference and in (ii) since it is included in the tax basis used to calculate the gain upon hypothetical sale).

Planning for the impact of the regulatory deferred gain calculation

As the examples above illustrate, the regulatory calculation could reduce and potentially eliminate the benefit of a low valuation in calculating deferred gain required to be recognized on Dec. 31, 2026, for investors in pass-through QOFs to the extent they have received distributions or loss allocations and a share of the QOF’s liabilities.

To identify situations where the “special amount includible rule” in the regulations is expected to negatively impact a QOF investor’s ability to reduce deferred gain required to be recognized on Dec. 31, 2026, investors should look for the following fact pattern:

- FMV of QOF interest on Dec. 31, 2026, is expected to be lower than the original deferred gain.

- QOF is a partnership or S corporation.

- QOF investor has or is expected to receive distributions or cumulative tax loss allocations through Dec. 31, 2026.

- QOF investor has or is expected to receive an allocation of the partnership or S corporation’s liabilities on its Schedule K-1.

It’s important for QOF investors to identify such fact pattern well in advance of Dec. 31, 2026, to give them time to consult with their tax advisor to determine the impact of the “special amount includible rule.” At a minimum, identifying such fact pattern timely could potentially help QOF investors avoid paying for an appraisal that’s not beneficial. Depending on the facts and circumstances, there may also be opportunities to implement planning strategies prior to Dec. 31, 2026, to mitigate the impact of the “special amount includible rule.” If a taxpayer identifies such fact pattern after Dec. 31, 2026, then they will have no flexibility to change the facts to help produce a more favorable result.

One possible opportunity to plan to mitigate the impact of the “special amount includible rule” involves the timing of a cost segregation study. It’s generally advantageous for QOF investors to maximizes depreciation deductions because they can create a permanent tax benefit. However, for real estate projects that have declined in value as of Dec. 31, 2026, performing a cost segregation study before 2027 could cause QOF investors to recognize more gain on Dec. 31, 2026 due, to the “special amount includible rule.” In such situations, QOF managers should consider deferring the cost segregation study until 2027.

If a QOF investor is tempted to ignore the calculation in the regulation and follow the calculation in the IRC, they should be aware that the Internal Revenue Service can assess substantial penalties in such situations. In addition, if a taxpayer takes a position contrary to a regulation, they’re required to disclose such position by attaching Form 8275-R to their tax return. With that being said, recent legal developments have impacted the authoritative value of government regulations. Taxpayers should consult their tax advisor to discuss how such developments may apply to their situation.

Key takeaways

- Investors in pass-through QOFs whose investment has declined in value should consult their tax advisor regarding the fine print in the Treasury regulations as soon as possible while they still have time before Dec. 31, 2026, to plan for the potential impact of such fine print.

- Such regulations may reduce or eliminate the investor’s ability to benefit from a low valuation to decrease the amount of deferred gain required to be recognized on Dec. 31, 2026.

- This issue applies to QOF investors who have or expect to receive distributions and/or cumulative tax loss allocations through Dec. 31, 2026, and an allocation of the partnership or S corporation’s liabilities on their Schedule K-1.