Individuals are often surprised to learn that accounting options are available for Paycheck Protection Program loans (PPP loans) made available under the Coronavirus Aid, Relief, and Economic Security (CARES) Act. These loans are perhaps the most well-known and talked-about element of the $2.2 trillion economic stimulus package authorized by Congress in March 2020 in response to the economic crisis resulting from the COVID-19 pandemic.

The Paycheck Protection Program was designed to provide loans as a direct incentive for small businesses to keep their workers on the payroll. PPP loans are generally intended for employers with fewer than 500 employees on their payroll. However, there were exceptions for entities such as franchises in the accommodation and food industries. Under the program, loans are administered by the Small Business Administration (SBA) and offered through participating lenders. If the funds are spent on qualifying expenditures and other criteria related to staffing, salary, and wage levels, some or all of each loan is eligible for forgiveness.

It’s the forgiveness aspect of PPP loans that provides the opportunity for accounting options. Loans are typically accounted for as debt, but in some situations, they can be treated as an in-substance government grant. Entities should take care in selecting an accounting policy, since the circumstances under which a Government Grant Approach can be used are limited. The accounting for a PPP loan will depend most significantly on the possibility of loan forgiveness, but will be influenced also by other important factors such as whether the entity receiving the loan is for-profit or not-for-profit and if financial statements are filed with the Securities and Exchange Commission (SEC).

Accounting approaches

Debt Approach

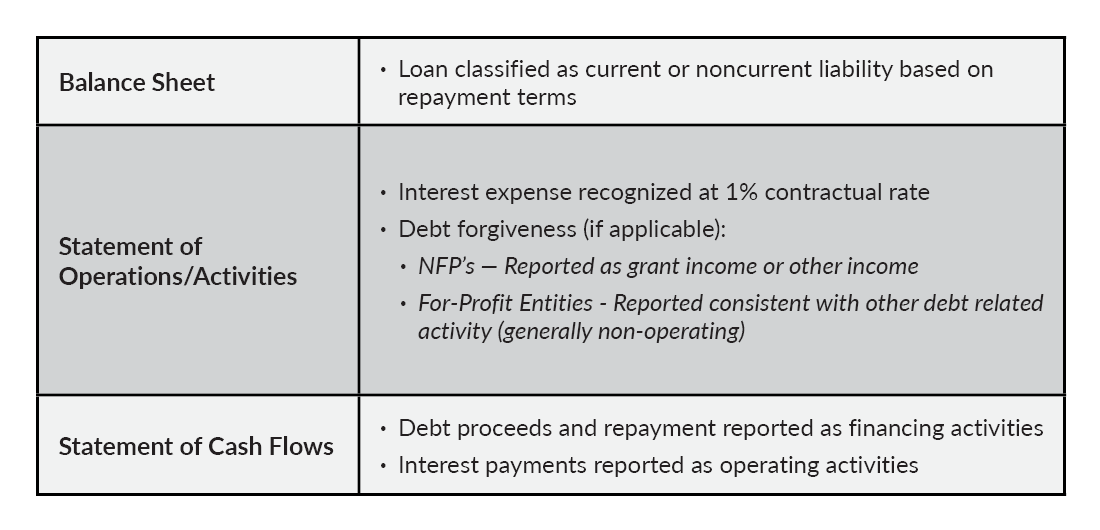

PPP loans, exactly as the name describes, are borrowings that bear interest and have specified repayment dates. Given the legal and contractual status of the loan as a debt obligation, it’s acceptable for all entities in all circumstances to account for it as debt. Under this option, called the Debt Approach, interest is accrued at the contractual rate of 1%, and the liability is classified in the balance sheet based on the required repayment dates. If the loan is forgiven in the future, the loan and related accrued interest will be removed from the balance sheet when notice of loan forgiveness has been received from the SBA.

Following is a summary of how a PPP loan is reflected in the financial statements under the Debt Approach:

The Debt Approach is acceptable in all circumstances and is required when the loan recipient doesn’t intend to seek or expect to qualify for loan forgiveness. It’s also recommended if the recipient intends to seek loan forgiveness but there is uncertainty as to whether it will be granted, either based on questions about the entity’s initial eligibility for a loan or meeting the loan forgiveness criteria.

Government Grant Approach

When the loan recipient reasonably expects to have some or all of the loan forgiven, it may be appropriate in some cases to account for the PPP loan and subsequent forgiveness as an in-substance government grant. This Government Grant Approach requires the borrower to conclude at all times, from initial receipt of the funds until final notification of SBA forgiveness, that loan forgiveness is probable. The expectation that PPP loan proceeds will never require repayment permits an accounting approach that ignores the legal and contractual status of the loan as a debt obligation.

Concluding that loan forgiveness is probable at all times should not be viewed as a simple undertaking. In an accounting context, probable events are those considered “likely to occur.” The threshold for concluding that an event is probable is significantly higher than that for “possible” or “more likely than not.

When evaluating the potential for loan forgiveness, borrowers must consider, not only the forgiveness criteria, but also their initial eligibility for the loan. The CARES Act allowed for fast dissemination of loans in the interest of combating the economic effects of the COVID-19 pandemic, but for many recipients, the forgiveness process will include an evaluation by SBA of the initial eligibility criteria. If the SBA concludes that the initial eligibility criteria weren’t met, it’s likely that repayment of the loan will be required.

As can be imagined, the quick rollout of PPP loans and the limited guidance on eligibility have created uncertainty for many recipients regarding whether they were initially qualified under the program. To help administer the loan program, the SBA has issued several Interim Final Rules, along with a significant number of Frequently Asked Questions (FAQs) to address common issues that have arisen.

Despite the guidance issued by the SBA, uncertainty still surrounds both the interpretation of certain aspects of the initial eligibility for PPP loans and the criteria for forgiveness. While the SBA indicated in one of its FAQs that entities with loans less than $2 million will be deemed to have made the initial loan certification requests in good faith, in one of the Interim Final Rules, they also reserved the right to review any loan in any amount at any time to determine whether the initial eligibility criteria have been met. As a result, the possibility of an SBA review should be considered when the borrower expects loan forgiveness. It’s this uncertainty as to how the SBA will interpret and enforce the program’s rules that can make it difficult to conclude that loan forgiveness is probable. For this reason, except in situations where it is evidently clear that forgiveness of a PPP Loan is not in question, we recommend the Debt Approach be used.

The Government Grant Approach itself allows for multiple options, but the use of one or more of these methods may be restricted by the nature of the entity and whether financial statements are filed with the SEC. Acceptable approaches include:

- Not-for-Profit Approach

- International (IAS 20) Approach

- Gain Contingency Approach

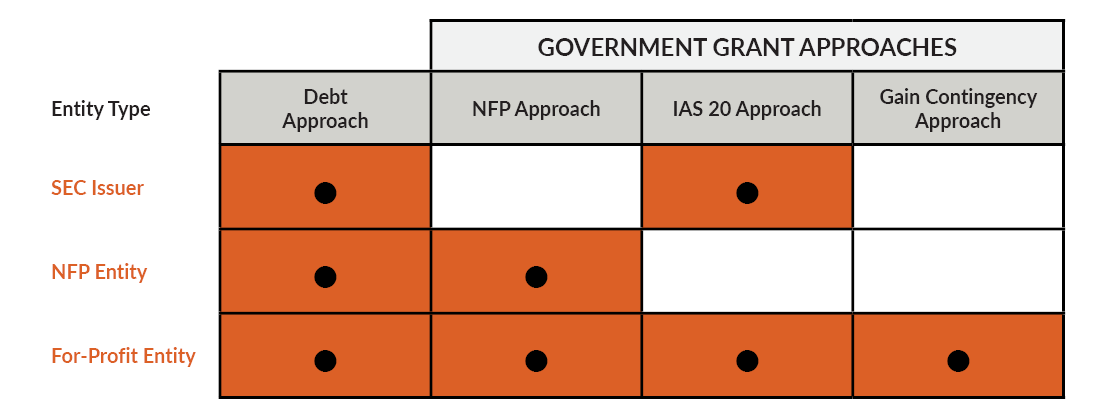

Not-for-profit entities that elect to use a Government Grant Approach to account for a PPP loan are required to use the Not-for-Profit Approach. Entities that file their financial statements with the SEC and elect to use a Government Grant Approach are required to follow the International (IAS 20) Approach, based on guidance from SEC staff. All other for-profit entities may elect to apply any one of the three options if they use a Government Grant Approach.

Each of three Government Grant Approaches is discussed in more detail below. As a reminder, the likelihood of forgiveness must be considered probable at all times from receipt of the initial proceeds until the final notification of forgiveness.

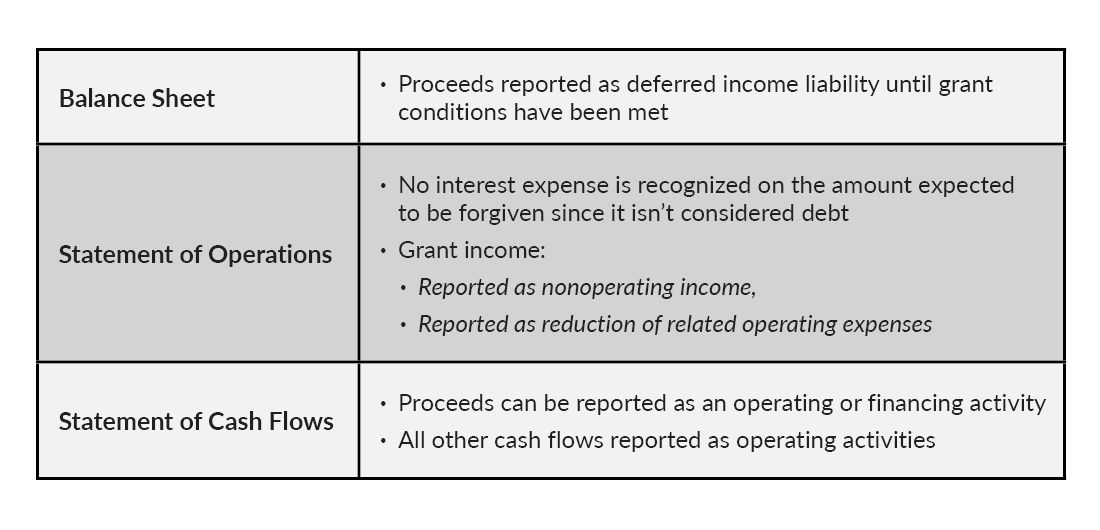

Not-for-Profit Approach – Generally accepted accounting principles for NFP entities include specific guidance to account for government grants. While for-profit entities are not included in the scope of the NFP guidance, it’s appropriate for them to apply this guidance by analogy. Recipients of PPP loans that are accounted for as in-substance government grants under the NFP Approach should follow the guidance for conditional government grants, which should be recognized in income when all conditions (often referred to as measurable barriers) have been substantially met. Prior to that time, funds received should be reported as a deferred income liability on the balance sheet.

Initial eligibility and forgiveness criteria, which include incurring eligible costs and maintaining certain employment and salary thresholds, should be evaluated for substantial compliance. It’s also important for entities to consider to whether the SBA’s review and approval of the forgiveness application constitutes a measurable barrier. If their approval is merely administrative, it’s not a barrier but a substantive process. No amount should be recognized in income until the period in which measurable barriers have been substantially met. That is, the recipient is prohibited from applying a probability assessment to the likelihood of meeting any of the measurable barriers.

If SBA approval is considered a measurable barrier, upon receipt of their SBA forgiveness notification, grant income will be recognized in the operating statement. On the other hand, if SBA approval isn’t deemed to be a measurable barrier, grant income can be recognized in the operating statement either at a single point (the end of the period when all eligible costs have been incurred), or ratably over the covered period based on the estimated level of loan forgiveness achieved to date. The way in which measurable barriers have been identified and interpreted will determine which recognition method should be used.

Following is a summary of how a PPP loan is reflected in the financial statements under the Not-for-Profit Government Grant Approach:

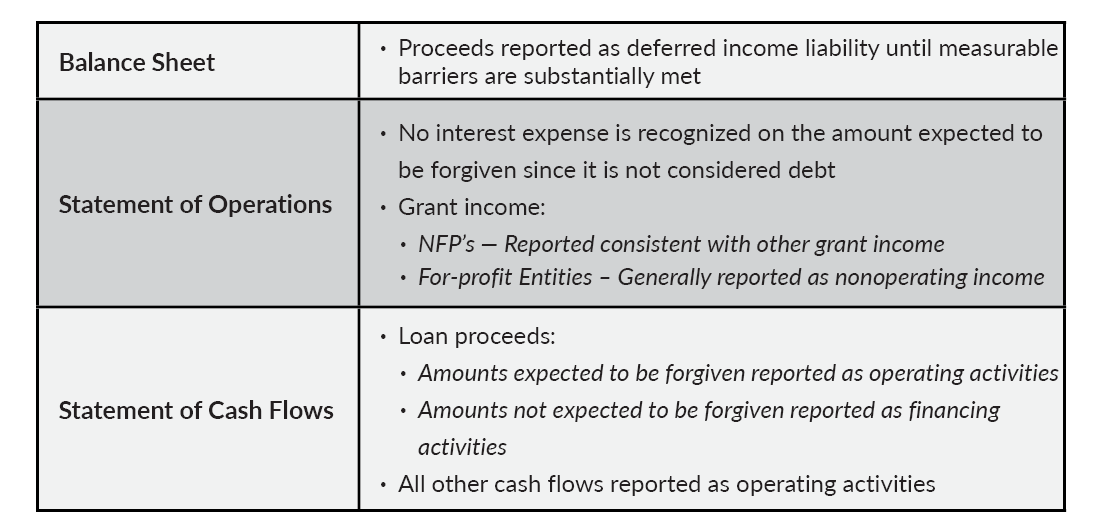

International (IAS 20) Approach – There is no authoritative guidance in accounting principles generally accepted in the United States (U.S. GAAP) addressing the accounting for government grants by for-profit entities. However, the International Financial Reporting Standards (IFRS), which are applied in many countries outside of the United States, provide guidance specifying how to account for government grants by for-profit entities, commonly referred to as IAS 20 based on the number assigned to the relevant standard. While entities applying U.S. GAAP are generally not permitted to use standards from other reporting frameworks, they may apply guidance by analogy when U.S. GAAP doesn’t provide any relevant direction. The application of IAS 20 by analogy by entities applying U.S. GAAP is well established in practice.

Under the International (IAS 20) Approach, government grants should be recognized in income when there is reasonable assurance that the terms of the grant will be met. “Reasonable assurance” is similar to “probable.” Funds received before an entity meets the terms of the grant are reported as a deferred income liability on the balance sheet.

While grant income should not be recognized until the terms have been met, the International (IAS 20) Approach permits income to be recognized using a systematic basis over the period that related expenditures are incurred. This generally results in the recognition of grant income over the period the covered expenditures are made, either eight or 24 weeks, depending on the terms of the PPP loan. The ability to recognize grant income proportionately is dependent on the continued ability to assert that if loan forgiveness is reasonably assured (probable) at all times, then grant income can be recognized proportionately. As always, forgiveness criteria and initial eligibility determines the likelihood of forgiveness.

The International (IAS 20) Approach also offers more flexibility for presentation of amounts in the statement of operations. Grant income can be reported as nonoperating income, or can be offset against the related operating expenses. Should the latter approach be used, the effect these offset amounts will have on operating margins and trends over multiple periods in specific line items in the operating statement should be considered.

Following is a summary of how a PPP loan is reflected in the financial statements under the International (IAS 20) Approach:

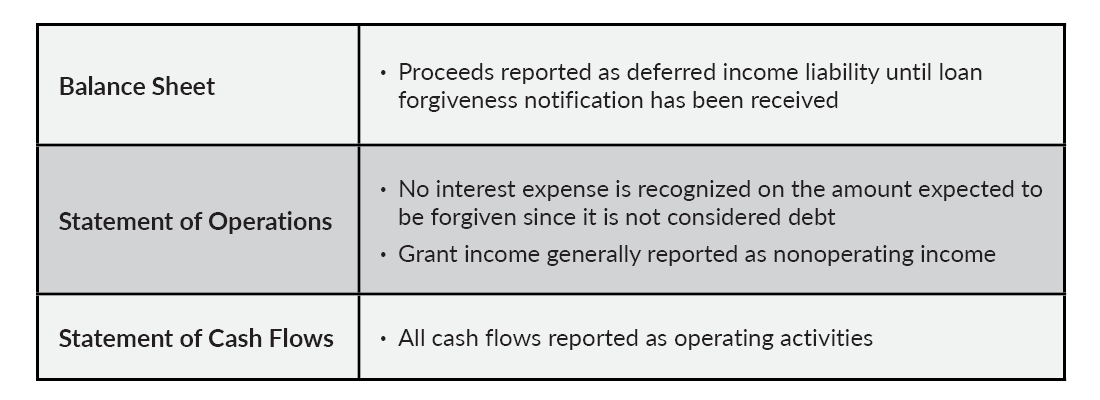

Gain Contingency Approach – A third approach is to view the potential forgiveness of a PPP loan as a gain contingency, which in U.S. GAAP, isn’t recognized in the operating statement until realized. Loan forgiveness would not occur until forgiveness notification from the SBA has been received. While the Gain Contingency Approach is similar to the Debt Approach in that no amounts are recognized in the financial statements without loan forgiveness, this option should only be used if it’s probable the PPP loan will be forgiven. This conclusion is necessary to avoid reporting the PPP loan as debt in the financial statements.

Once the SBA has forgiven the loan, grant income would be reported in the operating statement.

Following is a summary of how a PPP loan is reflected in the financial statements under the Gain Contingency Approach:

Following is a summary of the approaches to accounting for PPP loans by entity type:

Conclusion

Paycheck Protection Program loans have played a critical role in helping businesses and not-for-profits respond to the economic crisis resulting from COVID-19. Both their popularity and the unique provisions of the program in the CARES Act have made these loans a frequent topic of discussion. Accounting options are not often available for instruments that are legally and contractually debt. Under certain circumstances, U.S. GAAP will permit a PPP loan to be viewed as an in-substance government grant. An expectation of forgiveness must be probable at all times from initial receipt through notice of final forgiveness, which includes an assessment of initial eligibility for the loan. To support this conclusion, persuasive evidence must be presented, which may be difficult in some situations given the uncertainty as to how the SBA will enforce the provisions of the PPP loans. When in doubt, the Debt Approach is recommended in all circumstances.