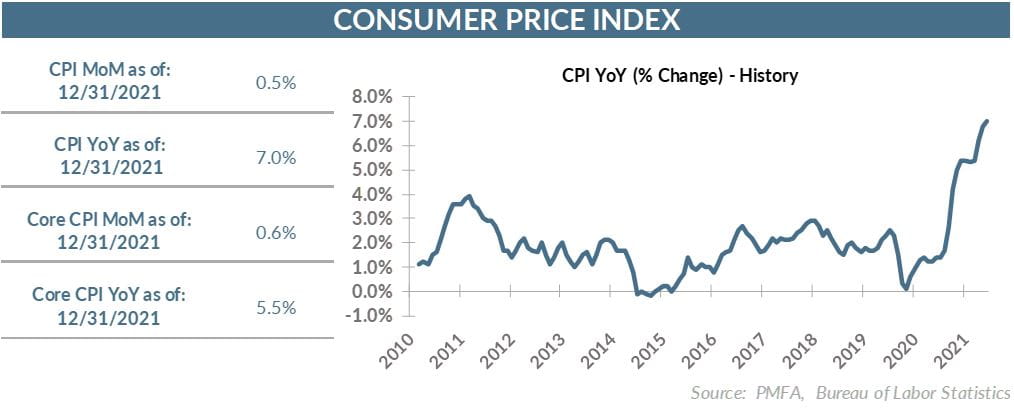

The consumer price index (CPI) increased by 0.5% in December from the month prior, modestly above expectations of a 0.4% increase, lifting the 12-month increase to 7.0%.

The 7.0% increase in the CPI was the highest since 1982 — a striking development after a decade that had economists and policymakers focused not on inflation but the more clear and present danger of deflation.

It was the risk of deflation in the aftermath of the global financial crisis that helped to define global monetary policy for the better part of a decade. It’s clear that the war on deflation is over, and the Fed is rapidly repositioning to take on inflation in a manner that hasn’t been needed in several decades.

A surge in energy costs has been among the primary contributors to higher inflation over the past year, but the causes run much deeper. Rising prices are still readily apparent in industries exposed to supply chain disruptions and labor shortages, including vehicles, lodging, public transportation, and dining out, as businesses pushed along those higher costs to customers.

The tightness of the jobs market has lifted wages for workers, a development that could also have a lasting effect on the prices of many consumer goods. Average hourly earnings rose sharply last year, up 4.7%. On the surface, that might seem like good news for workers, but with inflation running at 7.0% over that same period, real wages declined by 2.4%.

The average worker may like the gain in their paycheck, but those dollars are going out at an even faster pace, reflecting surging prices and the need for households to tap into savings or credit to bridge the gap.

In recent weeks, the Federal Reserve has adopted a much more hawkish outlook amid growing concern over the persistence of tight labor markets and rising inflation. As the labor market moves ever closer to the hypothetical level of “full employment,” there’s even less reason for the Fed to hold off on raising its short-term policy rate. It’s clear that policymakers agree.

The central bank’s December projections reflected a markedly more aggressive policy stance for 2021, baking in three likely rate hikes by the end of the year. The strength of labor and inflation data since then should increase the conviction of policymakers to act. There’s a growing sense that even three rate hikes before 2023 might not be enough.

The question that’s increasingly being raised is whether the Fed waited too long to wean the economy off of their monetary support and has now fallen behind the curve. Their recent shift in tone suggests that risks have risen. With measures of intermediate- to long-term inflation expectations remaining in a reasonable range, it appears that investors still believe that a combination of market forces and policy tightening can bring inflation pressures back under control in a reasonable time frame. Whether those expectations hold true will be an important consideration in the coming months.

The bottom line? While many inflationary pressures are likely to ease in the coming year, other forces like higher wages and home prices are likely to keep inflation above normal levels for some time. Higher interest rates are now in sight and are likely to be a reality sooner than most would have expected until very recently.

Past performance does not guarantee future results. All investments include risk and have the potential for loss as well as gain.

Data sources for peer group comparisons, returns, and standard statistical data are provided by the sources referenced and are based on data obtained from recognized statistical services or other sources believed to be reliable. However, some or all information has not been verified prior to the analysis, and we do not make any representations as to its accuracy or completeness. Any analysis non-factual in nature constitutes only current opinions, which are subject to change. Benchmarks or indices are included for information purposes only to reflect the current market environment; no index is a directly tradable investment. There may be instances when consultant opinions regarding any fundamental or quantitative analysis may not agree.

Plante Moran Financial Advisors (PMFA) publishes this update to convey general information about market conditions and not for the purpose of providing investment advice. Investment in any of the companies or sectors mentioned herein may not be appropriate for you. You should consult a representative from PMFA for investment advice regarding your own situation.