In 2020, interest rates reached their lowest point in 10 years, creating opportunities for wealth transfer strategies that do well in low interest rate environments. Today — with interest rates on the rise —lower-rate strategies may become less viable while new opportunities take their place.

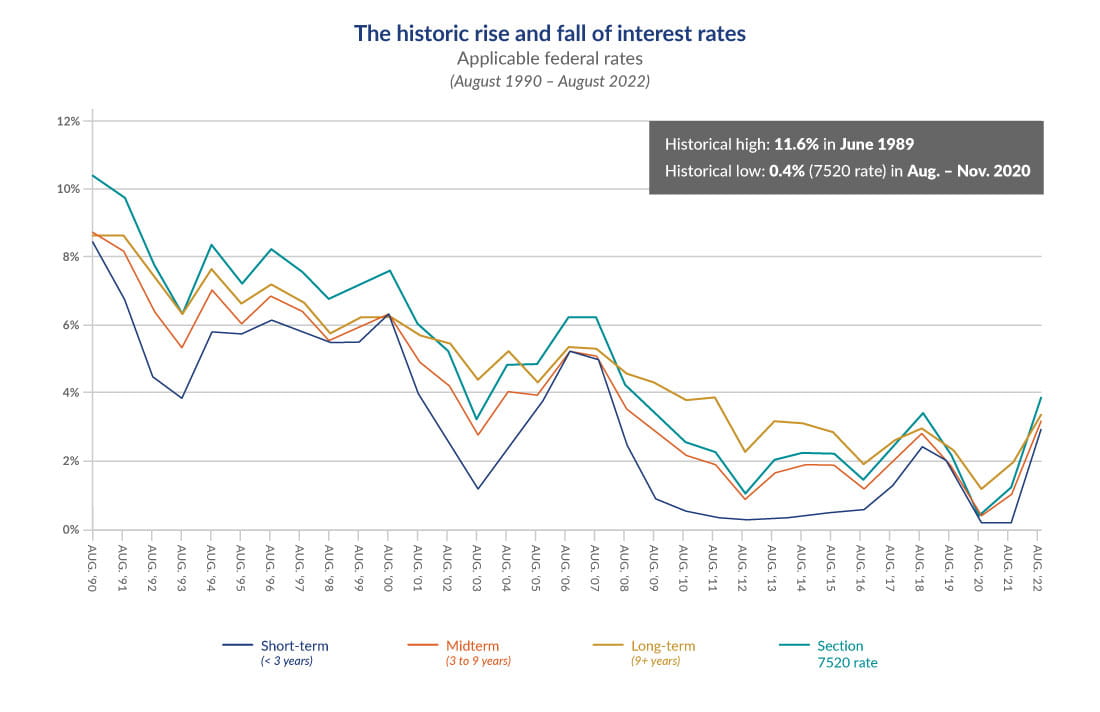

As seen in the chart above, interest rates are rising, but they’re still historically low.

With rates at these levels, now’s a good time to review your estate plan and consider locking in wealth transfer strategies that take advantage of lower interest rates while you can. It’s also a good time to start thinking about alternative strategies that become more effective when interest rates are higher.

Strategies for a low interest rate environment

While interest rates hover around historically low levels, it may still be possible to implement two popular low-rate strategies: the grantor retained annuity trust (GRAT) and the intrafamily loan.

GRATs

The GRAT can be an effective wealth transfer tool if you want to maintain assets — typically marketable securities — while transferring appreciation from the assets to noncharitable beneficiaries while using little to no gift tax exemption.

How does it work? A GRAT is an irrevocable trust in which you transfer assets for a set number of years and receive annuity payments based on IRS-published monthly interest rates (specifically the Section 7520 rate) at funding. If you survive the term of the GRAT, then once the final annuity payment is paid to you, the remaining assets (which represents the appreciation that exceeded the applicable IRS interest rate) will be distributed to the beneficiaries named in the trust. If the appreciation didn’t exceed the interest rate, the assets held in the trust will be distributed back to you. Thus, the only negative aspect to you for a “failed” GRAT is the cost of the legal fees paid to create it.

The reason GRATs are more effective during low interest rate time periods is because if the applicable IRS interest rate is lower, it reduces the rate of return required in order to pass assets to beneficiaries.

Even though interest rates are currently rising, it’s important to remember that interest rates are still historically low. So, for example, a GRAT funded in September 2022 would only need to outperform a 3.6% interest rate to then distribute a tax-free gift to the remainder beneficiaries. If the applicable IRS interest rate were to rise to 10.4% — as it was in August 1990 — it would be much harder for a GRAT to outperform that rate.

One final item of note for these trusts. While simple in concept, they do require knowledgeable administration. Beyond engaging solid legal advice to create them, having an experienced financial professional in the mix is important. They should help ensure proper assets are used to fund, monitor for any changes required while the trusts are in place, and ensure proper handling of annuity payments and final distributions.

Intrafamily loans

Intrafamily loans are a strategy that can help shift asset appreciation outside of your taxable estate. This could be a great strategy if you have a taxable estate and want to provide financial resources to children or other family members while minimizing the use of your gift tax exemption.

During a period of low interest rates, intrafamily loans can allow for a more attractive rate than what would be offered commercially. And with the current market volatility, it’s possible that some assets could be valued lower today than what they’re worth — potentially increasing the value transferred to the borrower/beneficiary.

For example, if you were to loan your child $1 million today, for tax purposes, you would have to charge them 2.93% interest based on the IRS-published minimum interest rates (known as the applicable federal rate [AFR] for September 2022). Any appreciation of assets above 2.93% could be retained by the borrower/beneficiary. At the end of the loan period, the amount included in your estate would be the $1 million loaned plus the interest earnings, but any excess appreciation would be removed from your taxable estate. Although the 2.93% interest rate is not as low as the .41% midterm AFR interest rate in August 2020, it’s still significantly lower than the 8.66% midterm AFR interest rates in August 1990. Further, if interest rates decrease at any point, the note could be refinanced to a lower rate.

As with GRATs, the ongoing administration of such loans are critically important to avoid issues with the IRS down the road. The lender and borrower must follow through on the terms of the note, including timely interest payments and other obligations. And records must support a history of terms being upheld. Once again, an experienced financial professional can support proper ongoing administration in coordination with your attorney and tax professional.

Since rates are still historically low, it may be possible to implement a GRAT or intrafamily loan now and lock in rates before they become too high. If you’re considering these strategies, implement them as soon as possible because rising rates typically reduce their effectiveness.

Strategies for a high interest rate environment

Given the current trajectory of interest rates, now may also be a good time to start considering longer-term strategies that work well in a high interest rate environment. Two options to consider are the charitable remainder trust (CRT) and the qualified personal residence trust (QPRT).

CRTs

A CRT is a trust where you fund a trust and then begin to receive an annual payment for a term of years. Upon the termination of the trust, the remaining assets are distributed to a designated charity. There are two types of CRTs to consider: the charitable remainder annuity trust (CRAT) and the charitable remainder unitrust (CRUT).

The CRAT pays a fixed income stream to you that’s based on a chosen percentage of the initial fair market value of the assets gifted to the CRAT. The annual payment doesn’t change during the term of the CRAT.

The CRUT pays an income stream to you that’s a fixed percentage based on the balance of the trust assets, which are revalued annually. So, the annual payment will change each year throughout the term of the trust.

Upon creation of the CRT, you claim an income tax deduction for the charitable portion of the transfer. The charity must receive at least 10% of the initial contribution upon the expiration of the trust. It’s worth noting that CRTs created for younger beneficiaries didn’t pass the 10% test until recently because interest rates were so low. However, when interest rates are higher, there’s a higher charitable deduction upon creation of the CRT. In this case, it’s assumed the assets in the CRT will grow quickly, meaning there will be a larger amount left for the charity when the annuity payment ends.

QPRTs

A QPRT is an irrevocable trust that reduces your taxable estate by transferring a residence into a trust for a period of time (term interest). Upon expiration of the term interest, the residence is transferred to remainder beneficiaries — oftentimes children or trusts for the benefit of children.

A QPRT can be an effective estate tax minimization tool because it allows you to continue enjoying the benefit of using your home while removing it from your estate. It’s important to note that a limit of two residences may be transferred to a QPRT (a primary residence and a secondary residence).

Upon the expiration of the term interest, you can continue to live in the residence by paying rent at fair market value to the remainder beneficiaries. This provides an additional way to transfer wealth since it’s not considered a gift. Additionally, the QPRT is generally structured, so the tax liabilities flow back to you as the grantor. So, in the IRS’ eyes, you’re essentially paying rent to yourself and the rental payments are therefore income tax-free.

The initial transfer to the QPRT is a taxable gift of the value of the remainder interest that’s calculated using IRS published minimum rate (Sec. 7520 rate). The higher the interest rate, the higher the value of your right to use the residence as your own during the term interest, and the lower the value of the gift of the future remainder interest. Therefore, as interest rates increase, the taxable gift decreases, which makes a QPRT an effective wealth transfer strategy with higher interest rates.

Timing is critical

Fluctuating interest rates are a reminder to review your estate plan and implement the most favorable estate planning strategies for the environment. If you have a taxable estate, it’s critical that you review your estate plan now and get your strategies in place. In addition to the rate environment, timing matters since the current estate tax exemption sunsets at the end of 2025.

If you have questions about your estate plan or would like to explore which strategy may be best for your personal situation, reach out to a member of your Plante Moran team now.