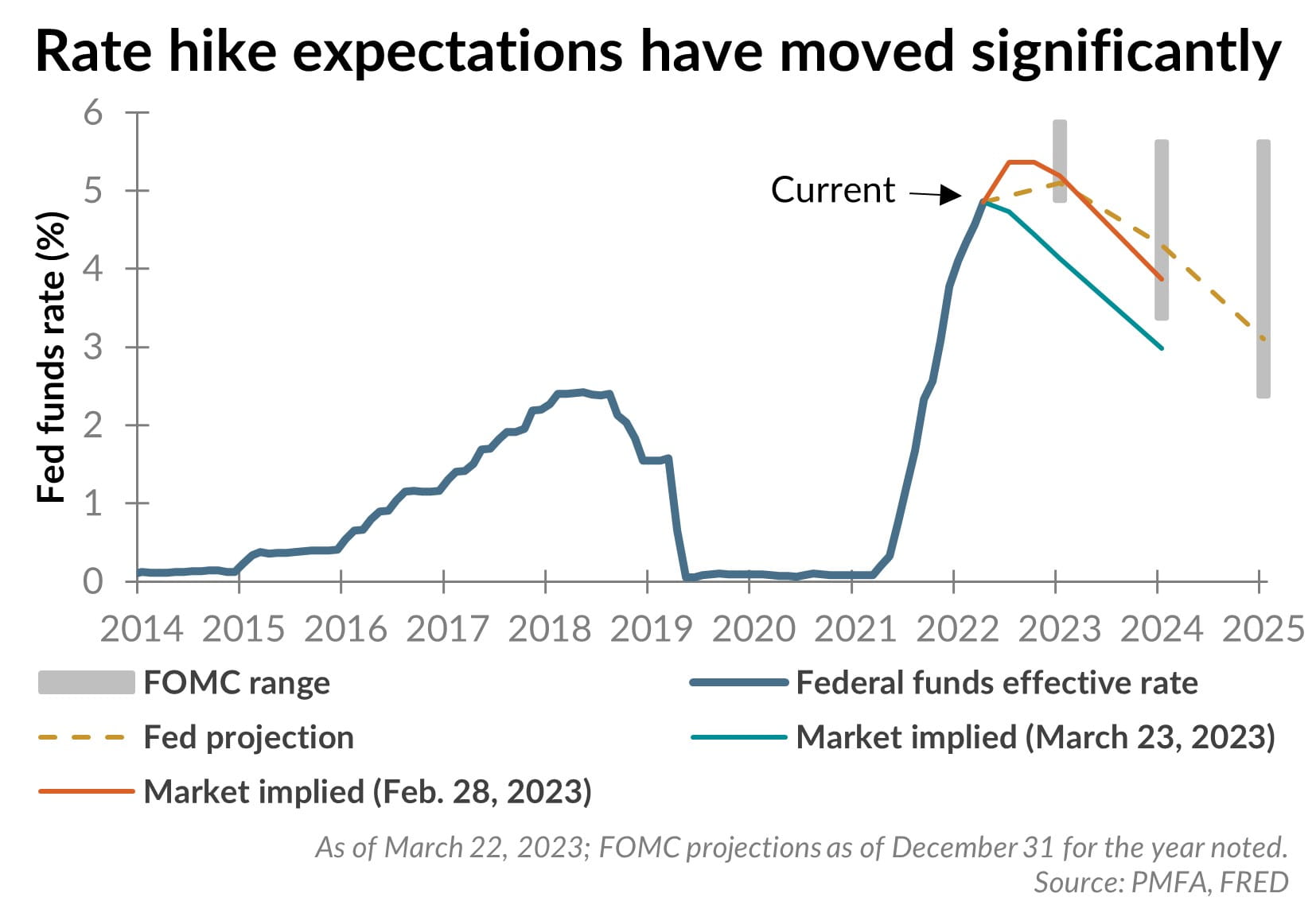

Last week, the Fed announced an additional quarter percent rate hike, confirming what markets had priced in as a virtual certainty in the days leading up to the decision. However, market expectations for Fed policy moved meaningfully in just a short period. Just a few weeks earlier, investors were pricing in a high probability of a 50-basis-point hike, with several more increases anticipated before the end of the year. The combination of sticky inflation and strong labor market data suggested that the cumulative effect of rate increases over the past year was still insufficient and further tightening would be needed. The Silicon Valley Bank failure and related turmoil that rippled through the banking sector quickly changed that view.

Last week, the Fed announced an additional quarter percent rate hike, confirming what markets had priced in as a virtual certainty in the days leading up to the decision. However, market expectations for Fed policy moved meaningfully in just a short period. Just a few weeks earlier, investors were pricing in a high probability of a 50-basis-point hike, with several more increases anticipated before the end of the year. The combination of sticky inflation and strong labor market data suggested that the cumulative effect of rate increases over the past year was still insufficient and further tightening would be needed. The Silicon Valley Bank failure and related turmoil that rippled through the banking sector quickly changed that view.

Policymakers have taken significant steps to stave off a banking crisis and reinforce the stability of financial markets. Still, the full impact of these recent events on financial conditions, the flow of credit, and the broader economy remains to be seen. And while the Fed did raise rates another quarter point last week, it also moderated its guidance, balancing indications that some additional tightening may be necessary with the recognition that faltering financial conditions will have an effect, the extent of which is indeterminable at this point.

The result? A peak Fed fund’s rate that may now be within sight — lower than what had been anticipated just weeks ago. The Fed’s updated projections now call for one more hike in 2023 before reversing course next year. Market expectations have become much more dovish, pricing in meaningful rate cuts before the end of this year.

Tighter credit conditions and a slowing economy wouldn’t reduce inflation overnight but could allow the Fed to stop tightening soon. How soon could the Fed pivot? Not as soon as the market expects, if you take the Fed’s word at face value.

Past performance does not guarantee future results. All investments include risk and have the potential for loss as well as gain.

Data sources for peer group comparisons, returns, and standard statistical data are provided by the sources referenced and are based on data obtained from recognized statistical services or other sources believed to be reliable. However, some or all of the information has not been verified prior to the analysis, and we do not make any representations as to its accuracy or completeness. Any analysis nonfactual in nature constitutes only current opinions, which are subject to change. Benchmarks or indices are included for information purposes only to reflect the current market environment; no index is a directly tradable investment. There may be instances when consultant opinions regarding any fundamental or quantitative analysis may not agree.

Plante Moran Financial Advisors (PMFA) publishes this update to convey general information about market conditions and not for the purpose of providing investment advice. Investment in any of the companies or sectors mentioned herein may not be appropriate for you. You should consult a representative from PMFA for investment advice regarding your own situation.