The gradual softening up in labor market conditions continued in April, as economic momentum continues to moderate under the weight of higher interest rates and consumers that have blown through much of the excess cash that was available to fuel spending over the past few years.

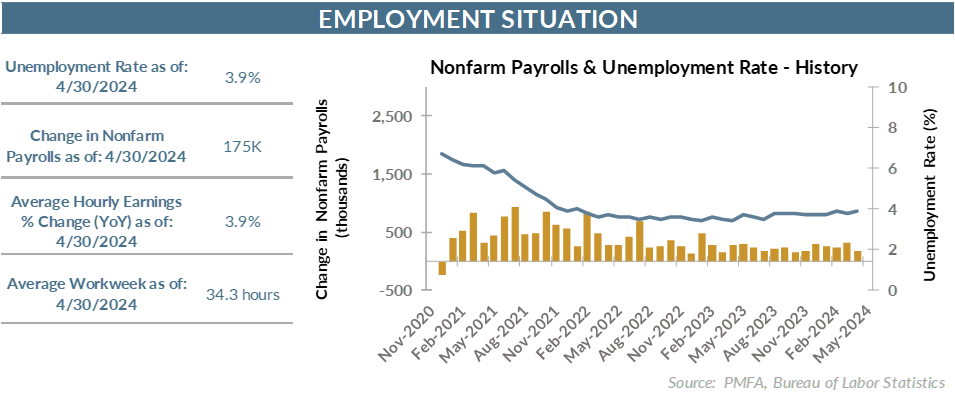

The unemployment rate edged fractionally higher to 3.9%, effectively erasing a comparable decline in March. The jobless rate has been tightly rangebound since late last summer and has been consistently below 4% for 27 consecutive months.

Job creation has also slowed — an unsurprising development as the economy comes off the boil and reverts toward trend growth. Employers added 175,000 new jobs in April — a solid but unspectacular number that reflects the slowdown in growth and resulting easing in demand for workers. That was well below forecasts for around 240,000 new jobs for the month. Revisions to the preceding two months shaved 22,000 from payrolls for a net increase of 153,000.

The economy has created about 2.8 million jobs in the past year, a decline of about 1 million jobs compared to the 12-month period ending in April 2023. That’s still a healthy pace though, easily topping the average annual gains over the latter half of the last expansion.

The material reduction in labor demand is also playing out in wages. The 12-month increase through April slipped to 3.9%, which is still elevated compared to pre-2020 norms but reflective of a continued normalization in employment conditions. That bodes well for the inflation outlook, particularly in the service sector where wages represent a significant portion of the cost structure.

The big question around employment conditions remains outstanding: can the Fed stick the landing? Have policymakers done enough to turn down the heat on the economy allowing inflation to drift back toward the central bank’s 2% target without overdoing it, pushing the economy off the ledge into recession and turning net job creation into net job losses? If they’ve calibrated correctly, it’s possible that the pace of job creation could stabilize in a range consistent with trend growth of 1.5–2.0%. Thus far, that outcome still appears to be squarely on the table.

As reiterated at his press conference earlier this week, Fed Chair Jay Powell continues to strike a cautiously optimistic tone about the path ahead for rate policy. While acknowledging that progress in the path of inflation back to 2% has stalled in recent months, he reiterated that the Fed’s next move was still a likely rate cut, although the timing remains very much in doubt.

Today’s report — with directionally constructive data on job creation and wages — should help to alleviate the concerns that have bubbled up in recent months about the need for the Fed to hike further. Even so, the stickiness of various inflation gauges since last fall in a range well above the central bank’s comfort zone appears likely to keep any rate cuts sidelined for now. Stagflation — even if not extreme — remains a risk as growth slows and inflation gauges remain elevated. Last week’s GDP reinforced that point with growth coming in below expectations simultaneous with various inflation readings heated up in Q1.

The bottom line? In many regards, the April jobs report was just what policymakers and investors needed. A slower but more sustainable pace of job creation coupled with wage growth stair stepping lower reflects a labor market that looks more balanced than has been the case in some time. There was nothing substantive in the report that suggests that the expansion in at risk in the near term but also nothing to suggest that the Fed needs to adopt a more aggressive stance in the pursuit of its dual mandate. It may be cliché to use the term goldilocks, but it was certainly “good enough.”

Past performance does not guarantee future results. All investments include risk and have the potential for loss as well as gain.

Data sources for peer group comparisons, returns, and standard statistical data are provided by the sources referenced and are based on data obtained from recognized statistical services or other sources believed to be reliable. However, some or all of the information has not been verified prior to the analysis, and we do not make any representations as to its accuracy or completeness. Any analysis nonfactual in nature constitutes only current opinions, which are subject to change. Benchmarks or indices are included for information purposes only to reflect the current market environment; no index is a directly tradable investment. There may be instances when consultant opinions regarding any fundamental or quantitative analysis may not agree.

Plante Moran Financial Advisors (PMFA) publishes this update to convey general information about market conditions and not for the purpose of providing investment advice. Investment in any of the companies or sectors mentioned herein may not be appropriate for you. You should consult a representative from PMFA for investment advice regarding your own situation.