The enactment of the One, Big, Beautiful Bill (OBBB) on July 4, 2025, significantly altered the tax landscape. That is especially true for those developing and constructing renewable energy projects that are intended to qualify for tax credits under the Inflation Reduction Act (IRA). The OBBB specifically targeted some of those credits while leaving other rules intact. Importantly, transition rules provide for continued eligibility if construction of solar and wind projects begins within one year of OBBB enactment. Our tax specialists review the changes to energy credits, requirements to satisfy the beginning of construction (BOC) test, and planning steps that can be taken now to provide certainty for future tax credit filings.

What did and didn’t change with the OBBB and IRA energy tax credits?

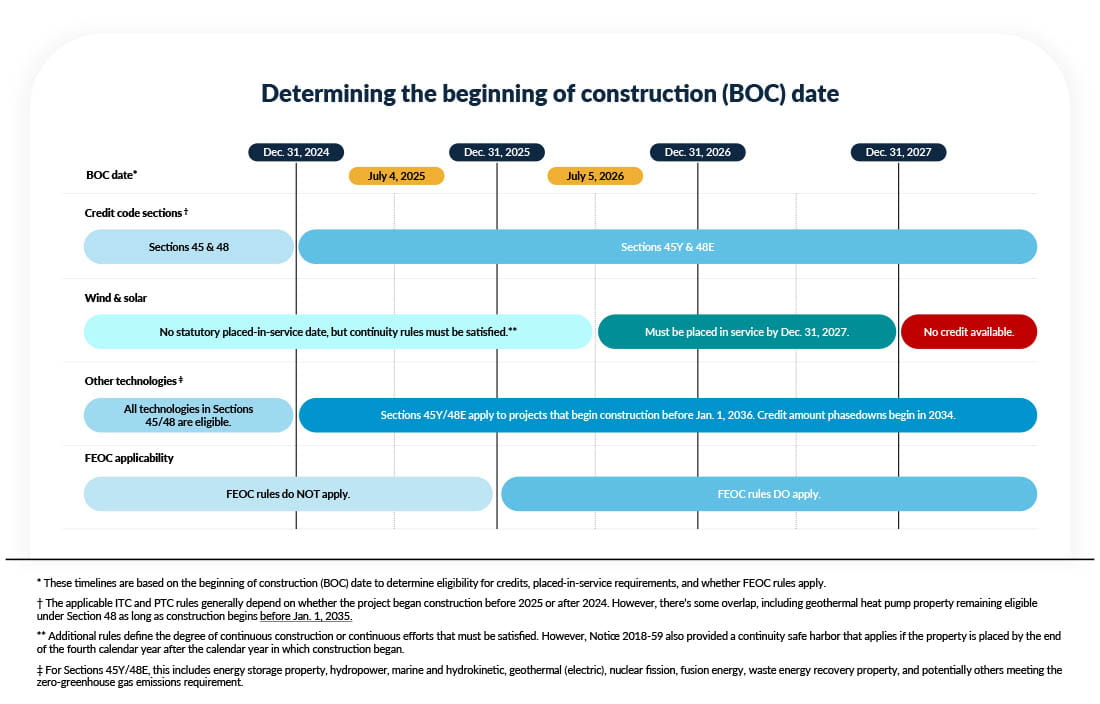

Historically, taxpayers who wished to install renewable energy property (e.g., wind, solar, geothermal) had two alternative paths to choose from. The first, the investment tax credit under Section 48 (ITC), was claimed in the year that the property was placed in service and was calculated as a percentage of the project’s cost basis. The second, the production tax credit under Section 45 (PTC), was claimed annually over 10 years based on the amount of electrical output in such years. The IRA significantly enhanced both the ITC and PTC on a temporary basis, with Dec. 31, 2024, being the operative BOC date. Projects meeting that deadline are generally unaffected by the OBBB.

The IRA also created new versions of the ITC and PTC, under Section 48E (ITC) and Section 45Y (PTC), respectively. Those credits have been available for projects that began construction after Dec. 31, 2024. However, the OBBB modified such rules with varying effective dates. Specific changes include:

- Wind and solar early termination; creation of one-year safe harbor. The general rule is that the ITC and PTC will no longer be available for wind and solar projects that are placed in service after Dec. 31, 2027. However, a special transition rule provides that wind and solar projects that begin construction by July 4, 2026, will still qualify for the ITC or PTC, even if placed in service after 2027. One clarifying exception allows energy storage property that’s installed at a wind or solar facility to continue to qualify.

- Increased ITC domestic content threshold. Bonus credits are available for projects that use U.S. steel and components meeting domestic content thresholds. The OBBB aligns the ITC rules with the PTC rules by applying a 20% threshold for offshore wind and 40% for all others for projects that began construction prior to June 16, 2025. However, those are increased in three sequential increments. First, up to 27.5% for offshore wind and 45% for all others for projects beginning construction after June 15, 2025, and before Jan. 1, 2026. Second, to 35% and 50% for those with BOC dates in 2026. Finally, both are increased to 55% for those beginning construction after Dec. 31, 2026.

- Expanded ITC for qualified fuel cell property. The ITC was also expanded to include eligibility for qualified fuel cell property without applying the zero greenhouse gas emissions test. Qualifying projects must have begun construction by Dec. 31, 2025.

- Material assistance from prohibited foreign entities. he ITC and PTC rules, as modified by the OBBB, disqualify projects that are owned or controlled by prohibited foreign entities or that receive material assistance from prohibited foreign entities. The material assistance restriction is based on a cost ratio measuring the degree of manufactured products used in the facility that are mined, produced, or manufactured by a prohibited foreign entity. Enhanced penalties will also apply to those that make false certification of data for the material assistance test when they know or reasonably should know of the inaccuracy of such certification. The material assistance rules apply to facilities for which construction begins after Dec. 31, 2025.

Shortly after enactment of the OBBB, a July 7 executive order complicated matters even further. That executive order directed the Treasury Secretary to “strictly enforce” the termination of the ITC and PTC for wind and solar facilities. Additionally, the executive order directed Treasury to publish new guidance within 45 days to ensure that policies regarding the beginning of construction aren’t circumvented by “the artificial acceleration or manipulation of eligibility … unless a substantial portion of a subject facility has been built.” In October, Treasury published Notice 2025-42 in response to the July executive order.

Determining the beginning of construction (BOC) date

Historical BOC rules

Establishing a BOC date for ITC and PTC eligible projects isn’t a novel idea with the IRA or OBBB. In fact, since 2013, taxpayers have relied on several Treasury Notices that lay out the guidelines for establishing beginning of construction. Under those previous notices, BOC is deemed to have begun if a project met either one of two tests:

- Physical work test — This test requires commencement of physical work of a significant nature either on-site or off-site. Examples of physical work in the notices include construction and installation of the energy property. However, digging foundations, laying footings or pads, or installing rebar are activities that generally may qualify. Under the physical work test, once the project begins, the taxpayer must also maintain a sufficient level of activity to meet continuous construction rules.

- 5% safe harbor — The 5% safe harbor test considers the taxpayer to have begun construction when it pays or incurs (under tax accounting method principles) at least 5% of the total project costs. Notably, this must be 5% of the total cost, not the budgeted cost, so cost overruns can pose a challenge. The continuous construction rules noted above also apply to this safe harbor.

Notice 2025-42: BOC rules for solar and wind projects

While it was uncertain how much these BOC rules might change for solar and wind projects under new guidance, Notice 2025-42 made meaningful but reasonable modifications to these rules. Under Notice 2025-42, the following methods are available to establish that construction has begun on solar and wind projects:

- Physical work test — The physical work test is still a valid method of establishing that construction has begun for solar and wind projects. While some slight additions were made to the requirements, the physical work test largely still applies exactly the same as it did previously.

- 5% safe harbor test — After Notice 2025-42, the 5% safe harbor is much more limited in its scope. While the mechanics of the 5% safe harbor rule are unchanged, the 5% safe harbor test is only available to establish beginning of construction for solar projects that are 1.5 megawatt (MW) or less. Wind projects may no longer utilize the 5% safe harbor to establish BOC.

The result of this guidance can be very influential to solar and wind projects aiming to begin construction by July 4, 2026. In some cases, the reality of beginning physical work of a significant nature by July 4, 2026, is a long shot. While the failure to do so could be detrimental, it’s important to remember that those projects can still maintain eligibility as long as they are placed in service by the end of 2027. On the other hand, while the 5% safe harbor test would have been a backup option in the past, if a solar project is not 1.5 MW or less, the 5% safe harbor no longer applies.

Finally, it’s worth noting that these new BOC rules under 2025-42 only apply to solar and wind projects for purposes of the 2027 credit termination date. Therefore, if a project utilizing any other eligible technology outside of solar and wind is aiming to establish BOC, those projects can still utilize the historical rules. Similarly, many project owners were aiming to begin construction to avoid the activation of the foreign entity of concern rules mentioned above by Dec. 31, 2025. The BOC rules in Notice 2025-42 don’t apply for foreign entity of concern purposes. The Notice 2025-42 BOC requirements will also not apply for purposes of determining BOC for bonus credits, like the domestic content bonus credit, or any other BOC purpose.

Should you act now?

It was widely anticipated that the tax credits expanded by the IRA would be modified in 2025 as part of broader tax legislation. In that sense, the resulting OBBB approach to the ITC and PTC weren’t necessarily surprising. However, the date of the early termination, one-year safe harbor, potential for enhanced BOC restrictions, and now applicable material assistance testing create a complex environment for planning purposes. The challenges are heightened for significant projects that ordinarily take multiple years to plan, source equipment, and complete. When evaluating the options, a few questions may inform decision-making.

- How critical is the credit to feasibility of the project? Tax credits are vitally important incentives for many renewable energy projects, but they’re not the only consideration. So, a threshold matter would involve considering the impact if the benefits of credits are never fully realized in the future. Such a situation could be presented by failure to meet eligibility or BOC tests, or through additional scrutiny by the IRS.

- Which effective dates will actually matter for this project? This discussion has largely focused on the termination of the credits for wind and solar and the BOC safe harbor. Although projects involving other qualifying technologies (geothermal projects, energy storage technology, and many others) will not face the same challenges. That said, the looming material assistance and prohibited foreign entity ownership rules might have necessitated even earlier work, depending on plans for the project.

- What can reasonably be done now, by the 12-month date? After determining the earliest applicable BOC date, the next task would be to honestly assess what can be accomplished within short timelines. With nationwide changes taking effect, permitting delays, contractor bottlenecks, and supply chain congestion could escalate quickly — potentially jeopardizing project eligibility if action isn’t taken promptly.

- Don’t forget about continuous construction. Easily lost on the shuffle of planning to begin construction is a plan to meet the continuous construction requirements. In general, if a project is placed in service by the end of the fourth calendar year after construction began, it’ll be deemed to have met the continuous construction requirements. If a project will likely exceed that four-year timeline, project owners must ensure work is continuous for the entire construction period. Failure to meet this rule will void an otherwise valid BOC date.

- What level of certainty is required? When considering potential levels of certainty, there are several considerations. The physical work test can be ambiguous when it comes to completing physical work of a significant nature. Projects that try to establish BOC by completing minor or trivial tasks by July 4, 2026, will be ripe to challenge by the IRS. Making sure that a project can not only start significant physical work — but meaningful physical work — will be key. Additionally, documentation and proof that construction began under these rules is vital. Real-time progress reports, construction photographs, invoice details, and more are strongly recommended. Similarly, it’ll be important to define who will be the interested parties to the credit filing, including investors or potential tax credit buyers. To that end, creating a plan to maximize satisfaction of all relevant rules is the best practice to avoid future surprises.

Ultimately, depending on the available options, stakeholders must consider how they can best meet these rules in a short time frame. This may require revisions of project scope, scale, or design to better align with the requisite tax credit dates. With only a few months left to begin construction in order to not be subject to the 2027 termination for solar and wind projects, proactive planning is more critical than ever.