On September 13, the House Ways and Means Committee released a first draft of the tax proposals of the Build Back Better Act (BBBA), the legislation intended to implement President Biden’s social and education reforms. The initial draft of the BBBA signals more moderate tax reform than initially proposed but still has several steps to go through before becoming law.

Private equity has been anticipating changes to the capital gains tax rates — along with the effective date of such changes — and the industry is watching closely since the outcome will directly impact after-tax proceeds in transactions and potentially the calculation of returns on investments. Depending on how it plays out, funds may look to adjust their return calculations to account for an increase in the highest capital gain tax rate, thereby grading their performance more uniformly on investments occurring before and after an increase to the rate.

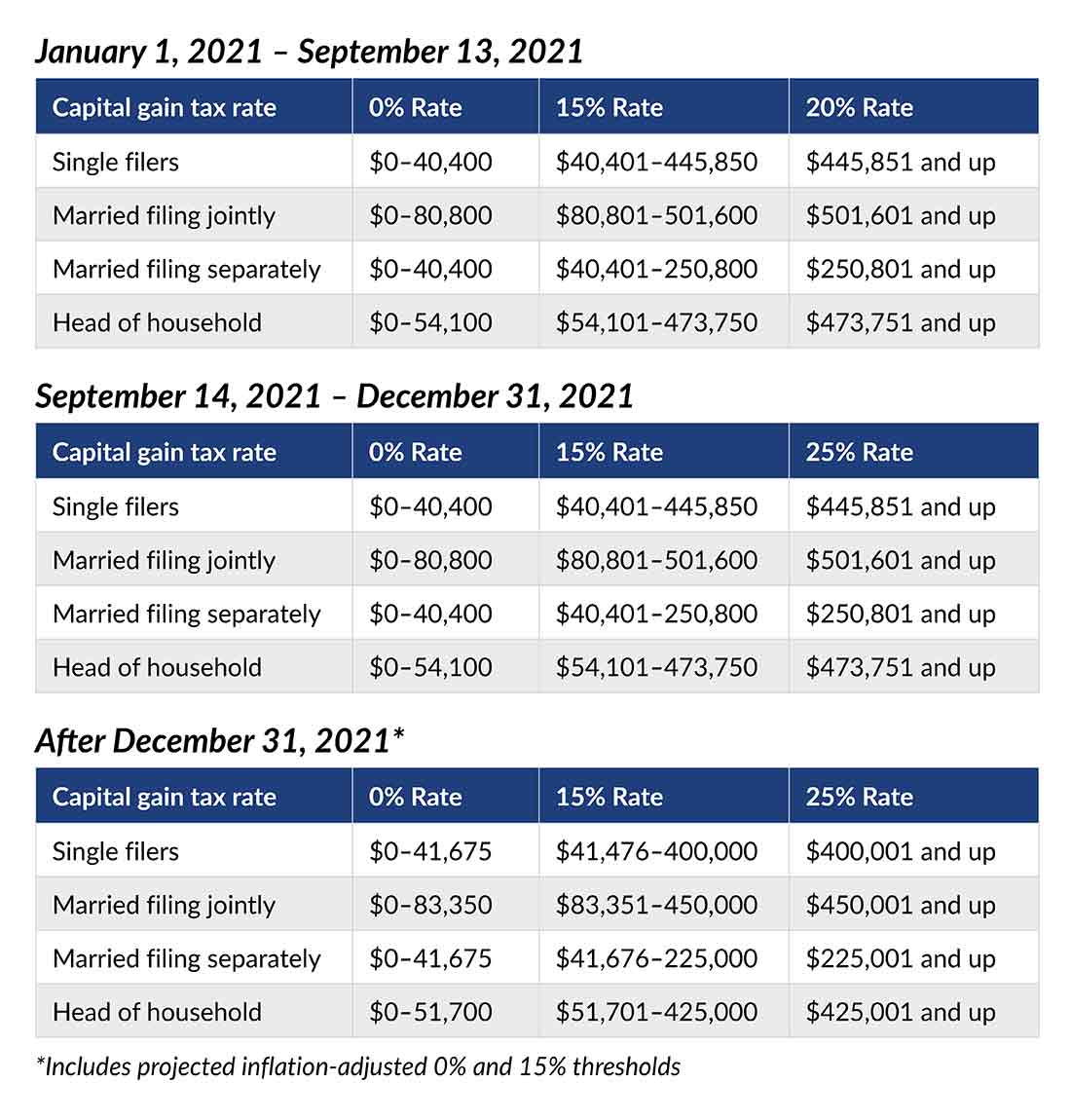

Had the Biden administration’s initial proposal of having the highest tax rate for long-term capital gains equal to the ordinary income tax rate (39.6%) moved forward, capital gain tax rates would have almost doubled without factoring in the impact of net investment income tax (NIIT). Instead, the BBBA, as currently drafted, would increase the highest capital gains tax rate to 25% and maintain a graduated rate structure for 0% and 15% capital gains tax rates. This increase would retroactively apply to capital gains recognized after Sept. 13, 2021. Here’s how the rates may look for 2021 calendar year:

Even though the proposed highest capital gains tax rate would be 25%, there are two key additions to BBBA that may increase the overall effective rate on capital gains for certain individuals:

- High-income surtax: A 3% surtax would apply for high-income individuals on modified adjusted gross income above $5,000,000 for married individuals filing jointly. The threshold for all other individual taxpayers would be $2,500,000, but the threshold for estates and trusts would be $100,000. Modified adjusted gross income would include capital gains as currently drafted. This would become effective for tax years beginning after Dec. 31, 2021.

- Expansion of NIIT: Historically, the 3.8% NIIT only applied to pass-through income of passive owners over certain income thresholds. The BBBA would expand those provisions to apply to taxpayers’ pass-through income even if those taxpayers are active in the business at the same income thresholds. This would become effective for tax years beginning after Dec. 31, 2021.

Combining the capital gains tax rate proposals with the surtax and NIIT proposals essentially creates a tiered increase in the overall effective rate on capital gains for high-income individuals on their business capital gains. From Sept. 14 to Dec. 31, 2021, capital gains would be taxed at 25% as the surtax, and NIIT expansion would not yet be effective. This could create an added incentive to close transactions prior to year-end even if the 25% capital gain tax rate were to apply.

Private equity and other high-income individuals will be substantially impacted by the increase in the highest capital gains tax rate even though it’s lower than President Biden’s initial proposal. We’ll continue to explore the BBBA’s impact on private equity and monitor our tax rates and policy changes resource center for updates as the legislation works its way through Congress. In the meantime, if you have any questions, give us a call.