For decades, alternative investments such as hedge funds, private equity, real estate, real assets, and private credit have been used extensively by larger institutional investors, including public and private pensions, college endowments, and foundations. These investors have maintained a core allocation to these alternative investments to help diversify away from public markets, enhance returns, lower downside risk, generate higher income, broaden the investment opportunity set, and in recent periods deliver protection against a rising inflationary environment.

The private wealth investor base has historically faced limitations for accessing alternative investments, such as high investment minimums, limited fund capacity, and fund managers’ inexperience working with individual investors. Today, many of these historical barriers have eased, and the private wealth channel is now viewed as an attractive source of capital for alternative investment managers.

Alternative investments aren’t a silver bullet, and they’re not suitable for every investment portfolio. But their importance and relevance within an overall asset allocation is growing and should be closely evaluated.

Alternative investment access points

Alternative investments are difficult to access for the average investor, with most strategies structured as private placement offerings, which aren’t widely available. They often require a minimum income and/or investment portfolio value (known as qualified purchaser and accredited investor rules) and are typically accessed through relationships between the prospective investor’s financial advisor and the fund manager. Common access points that a financial advisor may have for their private wealth investors include:

- Direct access: The traditional and most cost-effective way to access private investments is by subscribing directly to a manager’s fund. This can be difficult as many top-quality managers are capacity constrained from existing relationships, and investment minimums often exceed $1 million.

- Investment platforms: These platforms work closely with the financial advisory community to gather assets for alternative fund managers. They may even set up feeder funds (see below). Overall fees tend to be higher to cover feeder, platform, administrative, and sometimes due diligence expenses.

- Feeder funds: These are single fund vehicles that aggregate individual investor commitments into the manager’s underlying fund. It’s a way to offer access to alternative investments at lower minimums and can significantly minimize the administrative burden of fund managers onboarding investors. Feeder expenses can vary greatly across different offerings but generally start at 0.50% per year.

- Interval fund/tender offer funds: These structures provide investors access to alternative investments in a more simplified vehicle. These are closed-end funds, with 1099 tax reporting, daily/monthly subscriptions, improved transparency, lower minimums, and periodic liquidity. Relative to private placement comparable access points, they may come at a higher cost and with strategy limitations.

- Insurance dedicated funds: Offered through private placement life insurance or variable annuity policies, these products have tax-deferred status and can maximize the efficiency of investment growth on an after-tax basis. Product costs will likely exceed those associated with purchasing alternative investments directly and, therefore, the tax benefits should offset the higher costs to justify the purchase.

Evaluating alternative investments

When evaluating alternative investments, the following considerations will help achieve the best access point.

- Fees and expenses: Investment costs can cause a meaningful drag to net returns. Management and performance fees for alternative investments are high, while feeder and administrative expenses drive costs higher. Placement fees, which are paid upfront to some advisors/brokers, can cost another 2% or more at the beginning of the investment. Fee sharing between the fund manager and the advisor/broker, whereby the latter takes a cut of either the management or performance fee to compensate for marketing the strategy to their clients, creates another consideration as it can present a potential conflict of interest between the advisor/broker and client. [“As a fiduciary financial advisor Plante Moran Financial Advisors (PMFA) provides independent and objective advice and doesn’t accept any commissions or third-party compensation.”]

- Quality of offerings: The unique nature of alternative investments has produced variations in performance when compared to traditional asset classes over time. As such, due diligence on the investment manager and the respective offering is even more imperative than for a traditional investment manager. Private placements are not subject to the comprehensive regulatory structure applicable to registered offerings and present greater operational risks that must be understood.

- Taxes: Many alternative investment strategies are highly tax inefficient due to the source of their gains (e.g., trading-oriented hedge funds and credit-focused funds). Investors should evaluate after-fee and after-tax return expectations, as well as the most appropriate account to hold the investment (individual retirement account, taxable trust accounts, etc.). Further, additional tax compliance costs are often associated with alternative investments, given potential requirements for extending returns and supplementary state or foreign filings. Working with a financial advisor and a tax professional that has experience with alternative investments can help with the process.

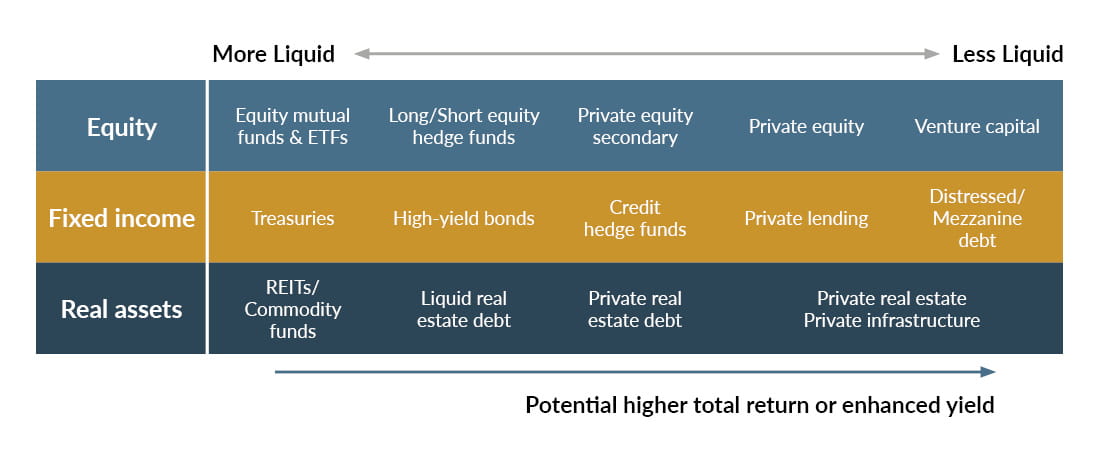

- Liquidity: The ability and timing to liquidate your alternative investment varies with each offering. Interval funds, tender offer funds, and open-end fund structures may allow liquidity on a monthly or quarterly basis, depending on the fund strategy, while private equity “drawdown” fund structures that invest in highly illiquid securities often lock-up capital for over 10 years. The investment manager has significant discretion on liquidity provisions depending on market conditions. It’s critical for investors to understand any and all liquidity constraints or provisions before making an investment in an alternative strategy.

The bottom line

Alternative investments are no longer the sole domain of institutional investors. For the right investor, they can provide diversification, portfolio stability, and enhanced returns. If you’re considering an allocation to alternative investments, it’s critical to understand the universe of strategies and the risks associated with each and choose an independent and objective investment advisor experienced in identifying, evaluating, and allocating to this distinctive class of investments.