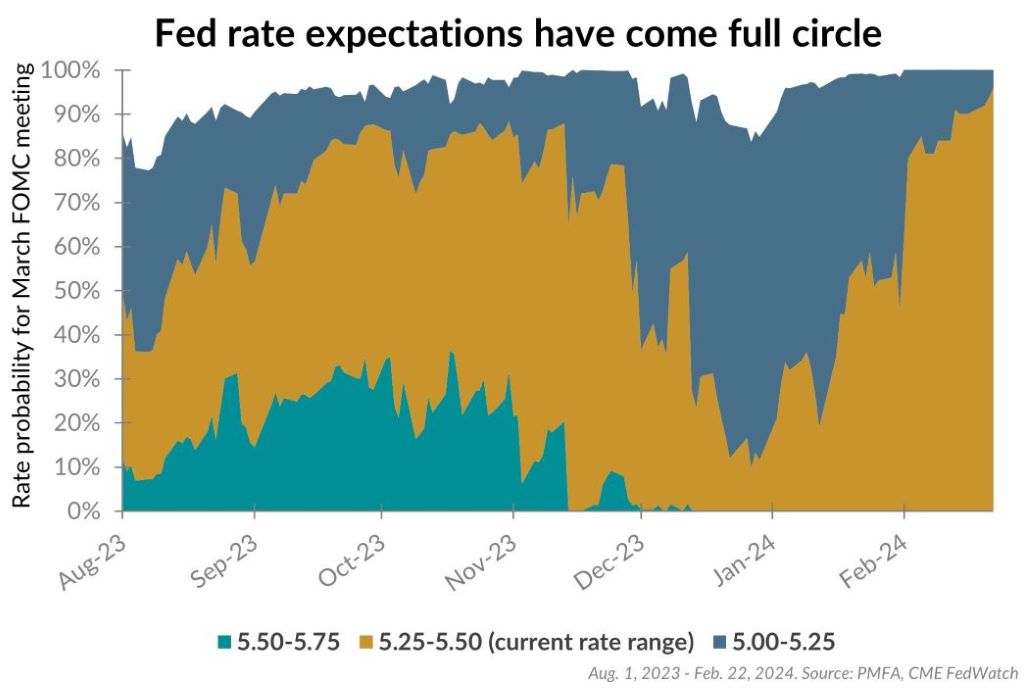

The Fed has been on pause since its last hike in July 2023, marking seven consecutive months that it’s held the benchmark funds rate steady in a 5.25–5.50% range. Markets, however, have continued to search for direction in the near-term outlook for monetary policy.

From mid-summer to last fall, the “higher for longer” narrative dominated rate forecasts, as economic activity continued to defy expectations to the upside. A dramatic shift occurred in October when the Fed explicitly acknowledged that rate cuts could be in their near-term playbook. The probability of a March 2024 rate cut dramatically increased from less than 10% in early October to about 75% by early January, prompting a strong close to the year for bonds as long-term rates fell sharply. In the last six weeks, that narrative has backpedaled amid hotter-than-expected inflation readings and a remarkably steady labor market. The probability for a March cut has consequently fallen back to below 10%, completing a roundtrip in expectations. Rates across the yield curve have edged a bit higher as a result, representing a near-term headwind for bonds.

Why does this matter? With a March cut now seemingly off the table, it’s a reminder of how quickly narratives — and investor sentiment — can change. Monetary policy matters, but it’s just one of many variables impacting markets over time and predicting near-term shifts is as difficult as timing the market. Investors are best served keeping an eye on the longer term. Over time, coupon yield matters much more than short-term rate volatility.

Data sources for peer group comparisons, returns, and standard statistical data are provided by the sources referenced and are based on data obtained from recognized statistical services or other sources believed to be reliable. However, some or all of the information has not been verified prior to the analysis, and we do not make any representations as to its accuracy or completeness. Any analysis nonfactual in nature constitutes only current opinions, which are subject to change. Benchmarks or indices are included for information purposes only to reflect the current market environment; no index is a directly tradable investment. There may be instances when consultant opinions regarding any fundamental or quantitative analysis may not agree.

Plante Moran Financial Advisors (PMFA) publishes this update to convey general information about market conditions and not for the purpose of providing investment advice. Investment in any of the companies or sectors mentioned herein may not be appropriate for you. You should consult a representative from PMFA for investment advice regarding your own situation.