Tax benefits related to renewable energy tax credits have been conditioned upon the satisfaction of complex technical requirements for many years — especially since the Inflation Reduction Act (IRA) expanded many opportunities in 2022. In July 2025, the One, Big, Beautiful Bill (OBBB) made additional significant changes to the Tax Code, including several modifications to energy-based tax credits.

Entering 2026, projects may now be subject to new restrictions based on the degree of foreign investment or material assistance provided by certain foreign entities. When triggered, these foreign entity of concern (FEOC) rules can result in denial of some of the most meaningful energy tax credits, including the Section 48E investment tax credit (ITC), the Section 45Y production tax credit (PTC), the Section 45X advanced manufacturing production credit, and others. With these high stakes in mind, careful analysis of the FEOC rules and evaluation of planning opportunities are crucial considerations when undertaking new projects.

What are the foreign entity of concern (FEOC) restrictions?

The FEOC rules are heavily nuanced in nature. However, in simplistic terms, an otherwise qualified energy project may lose energy tax credit eligibility under the FEOC rules if the project is owned by a prohibited foreign entity or if the project receives material assistance from a prohibited foreign entity. As such, there are three basic ways in which taxpayers can “fail” FEOC — and for that reason be blocked from taking certain key energy tax credits like the ITC or the PTC: (1) the project owner is considered a specified foreign entity; (2) the project owner is considered a foreign-influenced entity; or (3) the project receives material assistance from either a specified foreign entity or a foreign-influenced entity. Each of these categories carries its own, separately defined set of restrictions that are discussed further in this article.

Prohibited foreign entities: Specified foreign entities

The first way a project can fail the FEOC rules is when a project is owned by a specified foreign entity. Per the statutory language, there are five kinds of specified foreign entities:

- A foreign entity of concern. These are, roughly speaking, foreign terrorist organizations and other sorts of entities that present national security or foreign policy risks to U.S. interests.

- Certain Chinese military companies operating in the United States.

- Certain entities tied to Chinese forced labor.

- Certain energy firms listed under the National Defense Authorization Act for the 2021 fiscal year.

- A foreign-controlled entity. These tie to the “covered nations” of China, North Korea, Russia, and Iran. These “entities” may include not only the governments and governmental agencies of these nations, but also these covered nations’ individual citizens and nationals. However, probably the most consequential aspect of this definition is that any business that is a citizen of, or incorporated in any of those nations, will also be considered a specified foreign entity.

Prohibited foreign entities: Foreign-influenced entities

The second way a project may fail the FEOC rules is when the project is owned by a foreign-influenced entity. An entity may be considered a foreign-influenced entity either because: (1) it’s influenced in certain ways by a specified foreign entity; or (2) it has an agreement that calls for payments to a specified foreign entity such that, for FEOC purposes, the entity has ceded away effective control to a specified foreign entity.

- Influence: A U.S. taxpayer is considered influenced by a specified foreign entity if such entity: (1) has direct authority to appoint an officer; (2) owns equity exceeding a triggering threshold (25% or 40%, depending on whether specified foreign entities own separately or in the aggregate); or (3) is the creditor on 15% or more of the taxpayer’s debt obligations.

- Effective control: Effective control may be triggered where an agreement provides a specified foreign entity’s counterparty with authority over key aspects of eligible components, or energy generation and storage. Effective control is itself a deeply technical term that will require guidance from Treasury to flesh out in better detail. As we wait for that guidance, the statute provides interim rules that describe what sort of contractual rights constitute effective control. Beyond these interim rules, there are special provisions that describe how certain kinds of intellectual property licensing agreements can also cause taxpayers to trip into FEOC restrictions by way of the existence of effective control.

One shorthand way of distinguishing between these two is that the first basically relates to the ownership of certain foreign entities (mainly through stock or debt), whereas the second relates to specific sorts of agreements with certain foreign entities.

Material assistance

The third, and final way, that a project may fail the FEOC rules is if the project receives material assistance from a prohibited foreign entity. The material assistance rules prevent specified percentages of certain property tied to qualified energy tax credit projects from being sourced from either specified foreign entities or foreign-influenced entities. In other words, if the percentage of prohibited foreign entity materials included in the qualified project exceeds a threshold percentage, a project will fail the material assistance requirements.

Material assistance is calculated through a material assistance cost ratio (MACR). For purposes of the ITC and PTC, MACR is a fraction with the numerator equal to the total applicable direct costs of manufactured products attributable to the project minus the total applicable direct costs of manufactured products attributable to the project that are mined, produced, or manufactured by a prohibited foreign entity, and the denominator equal to the total applicable direct costs of manufactured products attributable to the project. If the MACR percentage is less than the applicable percentage, the project fails the material assistance requirements. Note, the MACR definition for Section 45X purposes applies with the same principles but instead takes into account direct materials costs paid, or incurred, by the taxpayer in producing an eligible component.

The MACR formula is as follows:

- (total applicable direct costs) – (total applicable direct costs manufactured by prohibited foreign entities) / total applicable direct costs = MACR percentage

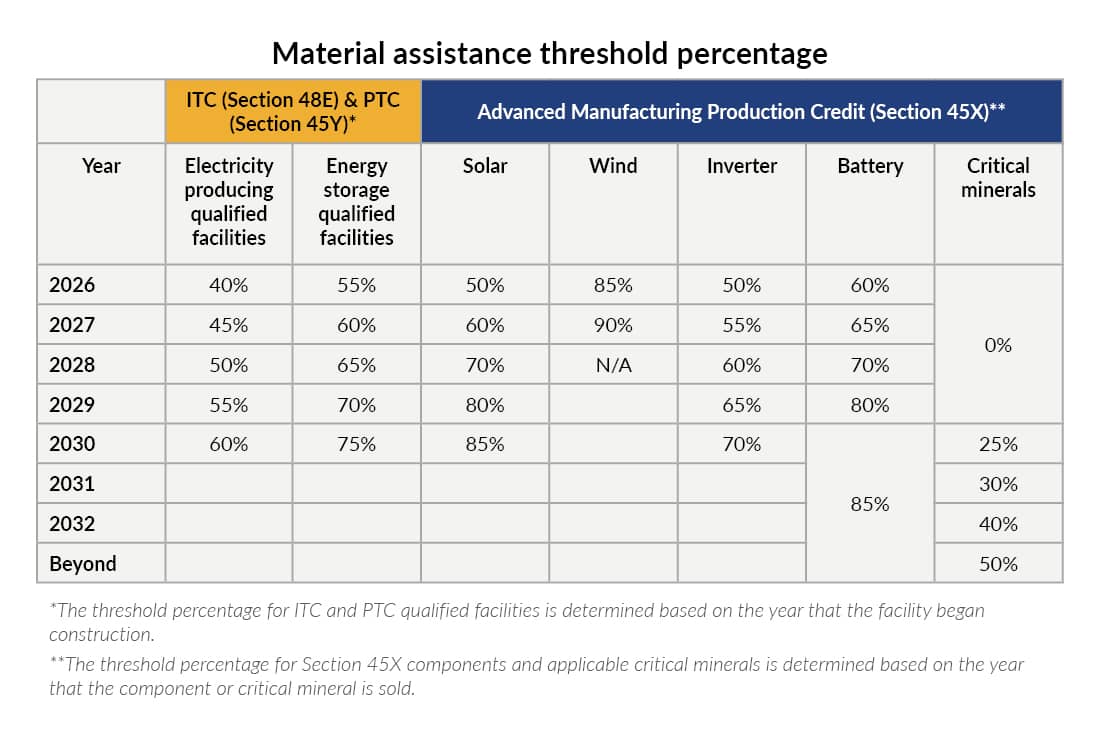

The threshold percentage is largely dependent on a project’s beginning of construction date and can differ depending on the component type. For example, ITC and PTC projects that incorporate technologies other than energy storage (i.e., solar, wind, geothermal, etc.) have a threshold percentage starting at 40% in 2026. That amount increases 5% each year until 2032 when the threshold percentage maxes out at 60% from that point forward. On the other hand, ITC and PTC energy storage projects have a threshold percentage starting at 55% for projects that begin construction in 2026, and that amount increases 5% each year thereafter until 2030 when the percentage maxes out at 75% from that point forward. Note, the threshold percentage for Section 45X applicable components and critical minerals varies by component type.

While the calculation of the MACR itself is fairly straightforward, the actual application may be difficult. This will require extensive information that project owners must request from various vendors and suppliers. For that reason, the OBBB does require Treasury to issue safe harbor tables as to the cost ratios. These tables will prove helpful because many counterparties may be reluctant to share such information, as is commonly the case when analyzing the similar, but different, domestic content rules. In conjunction with the safe harbor tables, taxpayers may also rely on certification statements from suppliers that state that the product or component in question was not produced or manufactured by a prohibited foreign entity. While we expect to see Treasury guidance in the near future on material assistance, and FEOC more generally, interested parties shouldn’t wait to start collecting this data for ongoing projects.

When do FEOC restrictions start to apply? Beginning of construction may be key

As to when FEOC restrictions apply, the answer depends on the specific tax credit involved. As for ITC and PTC projects being claimed under Sections 45Y and 48E, FEOC rules may kick in at different times depending on whether analyzing the prohibited foreign entity restrictions or the material assistance restrictions. As such, prohibited foreign entity restrictions (specified foreign entities and foreign-influenced entities) apply for any tax years that begin after July 4, 2025. Alternatively, the material assistance restrictions kick in for any project that begins construction on Jan. 1, 2026, or later.

Because of the 2026 activation date for material assistance, beginning of construction (BOC) rules are a crucial factor. Taxpayers who have already undertaken other energy tax credit projects are likely already familiar with the BOC concept, which generally provides a safe harbor from the phasedown of certain energy tax credits. In the context of FEOC rules, the BOC test establishes whether the project must satisfy the new rules. While the BOC rules may apply differently depending on the context, for purposes of FEOC, it’s currently understood that the BOC rules are applicable as they have been applied historically under Treasury Notices like Notice 2018-59 and Notice 2013-29.

Finally, as mentioned above, the FEOC rules don’t apply in the same way categorically to all credits. The advanced manufacturing credit at Section 45X provides an example of this. For Section 45X, there are no FEOC-specific BOC rules. Instead, no Section 45X credit is allowed for any tax year as to taxpayers that are specified foreign entities or are certain kinds of foreign-influenced entities. And for tax years beginning after July 4, 2025, there’s no credit for property for which there was any material assistance.

What happens if taxpayers get FEOC wrong?

Penalties, both old and new

Even before the OBBB introduced FEOC restrictions, taxpayers that claimed credits to which they weren’t entitled were exposed to accuracy-related penalties. In general, a 20% accuracy-related penalty can be triggered because of a substantial underpayment, which is the greater of 10% of the tax owed or $10 million. For FEOC, the new rules tighten the 10% threshold to only 1% of tax owed as to taxpayers that are disallowed the ITC, the PTC, or the advanced manufacturing credit because of the material assistance rules.

The OBBB also created new FEOC-specific penalties, which generally tie to the safe harbors that attend the material assistance rules. This new section applies to certification statements made after 2025 under the safe harbor tables. Generally, if a taxpayer should know or has reason to know that a certification statement isn’t valid, they may not rely on such statement and will be subject to greater penalties.

ITC recapture

The OBBB’s FEOC restrictions also include a new recapture provision that applies only to the ITC. Under this new recapture provision, if a taxpayer makes a payment to a foreign-influenced entity that’s considered foreign influenced because of the effective control concept described above, then there is a 100% recapture of the credit as to the tax year in which the payment was made, with the possibility of carryback and carryover adjustments. This 10-year recapture period begins in the year before claiming the credit.

What can taxpayers do now and expect next?

Treasury has work to do

The new FEOC rules are complex enough on their own. But there’s plenty more complexity yet to come, as the new FEOC statutory language in many places requires or allows Treasury to provide additional guidance.

Much of the forthcoming guidance is likely to come in the form of anti-abuse rules. There are several new statutory provisions that direct Treasury to issue rules to prevent abuse by evading or circumventing the restrictions. This sort of anti-abuse guidance is expected, for example, as to what “effective control” means in the context of foreign-influenced entities, as noted above. And when Treasury provides safe harbor tables in the material assistance context, we’ll eventually have rules designed to prevent stockpiling materials or evading the beginning of construction rules in situations where BOC has not, in fact, truly occurred.

Beyond these anti-abuse rules, there are other places where the OBBB allows, but doesn’t require, Treasury to issue guidance. For example, we may see guidance in the context of the possible receipt of material assistance for facilities that produce more than one eligible component, which ties to the advanced manufacturing credit at Section 45X. Additionally, while not necessarily expected, it wouldn’t be surprising to see further guidance on BOC rules as it applies specifically to FEOC considerations.

Plan accordingly

While we wait for additional guidance, taxpayers will need to lean into some of the ambiguity that appears from the statutory language. For now, this statutory language is all taxpayers will have to go on when it comes to maximizing the credits’ potential value without tripping into a FEOC restriction that could result in a complete denial of the credit a taxpayer is targeting.

Entering 2026, FEOC now applies in full force to any new projects. As such, interested parties must ensure they’ll be compliant with these rules or subject their projects to a total loss of tax credit eligibility. At this time, many of the key components of energy tax credit-eligible projects are produced in large quantities in prohibited nations. Therefore, project owners and interested parties must now juggle the ability to source nonprohibited foreign entity materials with strict time frames that will meet other new OBBB timing considerations. It’s vital for project owners to thoroughly analyze FEOC considerations early in a project’s lifespan so that no surprises are realized when it’s potentially too late.