The Financial Accounting Standards Board (FASB) recently finalized anew standard for revenue recognition that moves away from arules-based approach to a much broader principals-based approach.Nonpublic companies are required to implement the new standard onfinancial statements for periods beginning after December 15, 2018.

The new standard represents a major change in financial accounting.Because almost all businesses start with book income to determinetaxable income, this shift will likely have a significant ripple effect on taxreturn preparation and tax liabilities as well. As the final effective date is coming up quickly, planning should be in process now for any entitythat issues GAAP financial statements. In order to have a successfulimplementation, businesses should ensure that tax considerations areincluded in each step of the process.

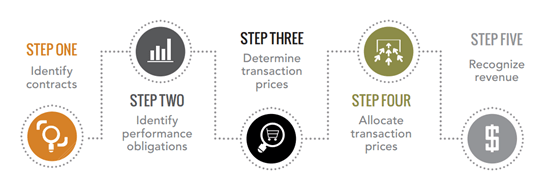

A quick look at the new standard

The new standard requires a business to look at each customer contract todetermine how to recognize revenue. The analysis is a five-step process:

A refresher on tax revenue recognition

Generally, revenue is recognized for income tax purposes when it’s received,when it’s due, or when it‘s earned — whichever comes first. There aremany exceptions to this rule for transactions including long-term contracts,installment sales, and advance payments.

There are three general possibilities for businesses to consider when it comes tothe tax accounting impact of the new financial standard — and the answer may differ for different revenue streams within the same company:

- Book revenue recognition methods change, but tax revenuerecognition methods can’t change.

Tax revenue recognition methodsare determined under tax law, so generally speaking, tax revenue recognition can’t changeunless the tax law changes. So even if the book method changes, theprevious tax method may still have to be used for income tax purposes.This may require additional reporting to be available within theaccounting system or may require the accounting system to maintaintwo different revenue recognition models for each transaction. - Both book and tax revenue recognition methods change.

Tax revenue recognition rules may not always provide a clear black andwhite answer. In these cases, it’s possible that the new book methodmay be used for tax purposes as well. However, tax law generallyrequires that a taxpayer apply for a change in accounting method with theIRS if they are changing the way they account for revenue or expenses from year-to-year. The IRS has preliminarily announced that they expect to allow taxpayers to do this on an "automatic" basis, meaning that it will not cost a separate fee to be paid to the IRS but will still require the taxpayer to file this application with its tax return. This application will still require time and effort. - The tax revenue recognition method directly refers to the financialaccounting method.

Some tax revenue recognition methods directlyincorporate financial accounting methods. If a taxpayer changes the way they account for these itemsfor financial accounting purposes, they must also change the waythey account for them for income tax purposes. In these cases, theIRS will still expect the taxpayer to file for a change in method of taxaccounting. To make matters a bit more complex, the recent tax reform legislation created several new categories of these items for taxpayers with audited financial statements. For instance, taxpayers are now permitted to defer the recognition of revenue related to advance payments only if they defer the recognition on audited financial statements. Similarly, taxpayers are not permitted to defer the recognition of any revenue beyond when that revenue is recognized on their audited financial statements, even if tax law otherwise would have required it to be recognized later. The allocation of a transaction price between performance obligations within a transaction must be followed for tax purposes as well. Taxpayers are still awaiting guidance clarifying the scope and implementation of these new tax laws as they address both the new GAAP and tax revenue recognition guidance.

Many questions remain unanswered

The implementation of the new financial standard is an ongoing process.FASB, accountants, and businesses continue to identify new issues anddevelop solutions to make the transition as smooth as possible. The IRS hasalso sought input from taxpayers on these issues in an effort to understandif tax rules may need to change to provide more flexibility. However, giventhe complexities surrounding financial accounting and the IRS' primary focus on tax reform related items, these rules changes are moving slowly..

As with most significant changes, there are still many questions that must beasked and answered. As businesses prepare for the new revenue recognitionrules from a book accounting perspective, they shouldn’t forget aboutthe tax implications of those changes. Overlooking tax issues during thetransition may result in missed opportunities or future surprises.