Public Act 202 of 2017 (the “Act”) established reporting requirements for all local units of government that offer, or provide, defined benefit pension plans and defined benefit other post-employment benefit plans (OPEB). On Sept. 25, 2018, the Michigan Department of Treasury released the final uniform assumptions for reporting requirements under the Act.

Reporting requirements

The Act requires local units to submit Form 5572 annually, for both pension and OPEB plans, no later than six months after the end of the fiscal year.

A key component of the Act requires the state treasurer, annually, to establish uniform actuarial assumptions. The intent allows retirement systems, across the State of Michigan, to be compared on a standard basis. These uniform assumptions are only required for reporting purposes on Form 5572 and may differ from the assumptions used in the audited financial statements. In the case that the uniform assumptions and the assumptions reported in the financial statements differ, two sets of funded ratios and contributions will be included in the annual Form 5572. While the uniform assumptions aren’t required for funding purposes, local units should consider aligning these two assumptions to avoid the need for a third set of valuations.

Effective date for Michigan Public Act 202

Local units must begin reporting funded ratios and contributions in accordance with the uniform assumptions as follows:

- Fiscal year 2019: If audited financial statements are based on an actuarial valuation issued after Dec. 31, 2018.

- Fiscal year 2020: If audited financial statements are based on an actuarial valuation issued prior Dec. 31, 2018.

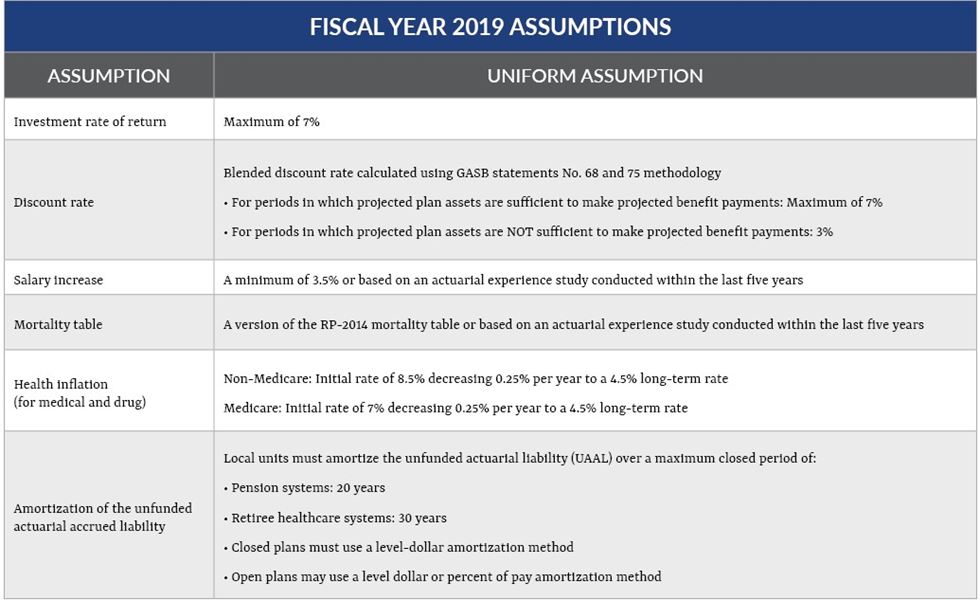

As stated in the Department of Treasury letter, titled “Public Act 202: Selection of the Uniform Assumptions”, the state treasurer has established the following uniform actuarial assumptions: