As part of the implementation process for the American Rescue Plan Act (ARPA), the U.S. Department of Treasury (Treasury) adopted the ARPA final rule for the Coronavirus State and Local Fiscal Recovery Funds (CSLFRF) on Jan. 6, 2022. Plante Moran’s article U.S. Treasury adopts final rule for SLFRF: What you need to know now provides an overview of the significant changes from the interim final rule. This article will look more closely at how communities can distribute relief ARPA CSLFRF funds awarded under the “negative economic impacts” classification of the ARPA final rule.

What can ARPA CSLFRF funds be used for?

The ARPA final rule still includes the following four broad uses for CSLFRF funds:

- Responding to the negative economic impacts of the public health emergency

- Responding to essential workers with premium pay

- Government services to the extent of revenue losses

- Making necessary investment in water, sewer, or broadband services

As communities start to evaluate the uses of the funds, each community will need to consider its local needs and what will be the highest and best use of the funding. One of the broadest possible needs to consider is the first item listed above, responding to negative economic impacts. Millions of American households and businesses were negatively impacted by the pandemic, with some of the most severe impacts hitting households and communities that were already disadvantaged by preexisting disparities. This category of the ARPA CSLFRF funds is intended to bring relief to those communities that were hardest hit by the pandemic and to help ensure that the benefits of any subsequent economic recovery reach all Americans.

As your community works to determine how to spend your ARPA CSLFRF award, here are some key questions to ask that will help determine who qualifies for ARPA CSLFRF funds intended to help alleviate negative economic impacts of the pandemic.

1. Who can benefit from this funding?

Eligible beneficiaries fall into a few categories: households, small businesses, and nonprofits. Eligibility within each of those categories will depend on whether a population within that category was “impacted” or “disproportionately impacted” by the pandemic. To simplify administration, Treasury has presumed certain populations to be eligible. Some of the presumed eligible populations include low- or moderate-income households or communities, households that experience unemployment, small businesses and nonprofits operating in Qualified Census Tracts, and industries within the travel, tourism, or hospitality sectors.

2. What are “eligible resources or services” under the ARPA final rule?

Eligible resources or services are intended to respond to the negative impact that the beneficiary experienced. The ARPA final rule provides an extensive, but not all-inclusive, list of eligible uses within each category. Some of the enumerated projects include food assistance, emergency housing assistance, and loans or grants to businesses to mitigate financial hardship.

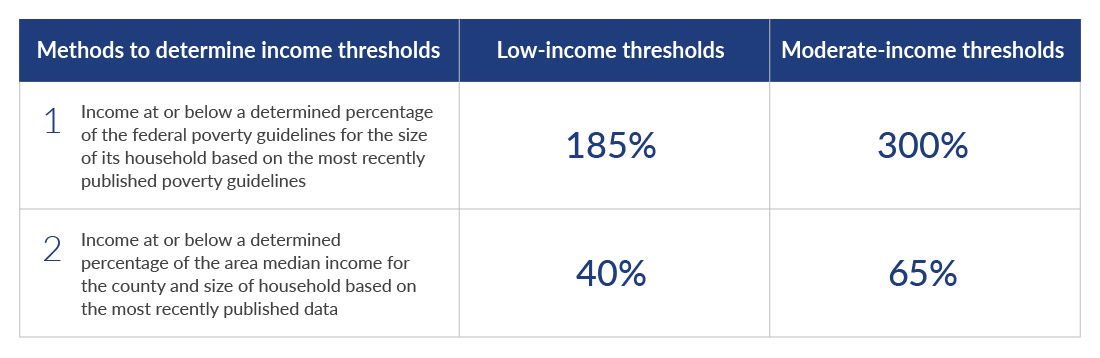

3. How is low versus moderate income determined for eligible households?

Low- or moderate-income households and communities are presumed eligible for benefits.

This table shows the two methods that can be used to determine income thresholds. You can check the Federal Poverty Guidelines and median income levels here.

4. What qualifies as a “small business” under the ARPA final rule?

Two criteria need to be met in order for a small business to qualify for assistance. 1) The business can’t have more than 500 employees, and 2) the business must be a “small business concern,” which means that it must be independently owned and operated and not dominant within its industry. The recipient community is responsible for determining small businesses that were impacted using certain factors, such as decreased revenue or increased costs. The recipient will also need to determine the appropriate course of response, i.e., loans, grants, or technical services to support business planning.

5. How can my community provide assistance to impacted industries?

First, an industry must be designated as impacted. Travel, tourism, and hospitality industries are presumed impacted. Other industries may be deemed impacted if they experienced a decrease in employment by 8% or more. Another determining factor could be if an industry is experiencing economic impacts that are comparable to or worse than those experienced by the travel, tourism, and hospitality industries as a result of the pandemic. Treasury encourages recipients to narrowly define impacted industries using geographic regions or other factors that may have affected the pandemic’s negative impact. In order to avoid any potential conflicts, once an industry is identified as impacted, all business in the impacted industry should be considered eligible to apply for assistance.

6. What nonprofits are eligible?

A nonprofit is defined specifically as those that qualified for tax exemption under Section 501(c)(3) or 501(c)(19) of the Internal Revenue Code. Similar to households and small businesses, a nonprofit beneficiary must also have been negatively impacted by the pandemic in order to be eligible. It’s important not to confuse nonprofit subrecipients with those that are beneficiaries. Subrecipients are not required to be negatively impacted, rather, they are organizations that may carry out eligible uses on behalf of a government recipient.

7. What if my community would like to spend the money on eligible uses beyond those enumerated?

The list of eligible uses suggested by Treasury is not all-inclusive. The program does give communities some flexibility in how they identify and respond to negative economic impacts. It ultimately comes down to two determinations: 1) identifying an individual or population that was negatively “impacted” or “disproportionately impacted” by the pandemic, and 2) designing a response to address the impact. If a community decides to go this route, documentation should be retained to support the negative impact experienced. Individual impacts don’t need to be documented if the impact was determined at the class level, although documentation that identifies each individual recipient as belonging to the affected class should be retained (i.e., they live in a certain geographic area). Assistance provided should be proportional to the impact experienced. For example, “impacted” populations should not receive more assistance than those “disproportionately impacted.”

An overview of the final rule can be found on the U.S. Treasury website. Be sure to subscribe to our alerts for additional in-depth analysis of Treasury’s ARPA final rule.