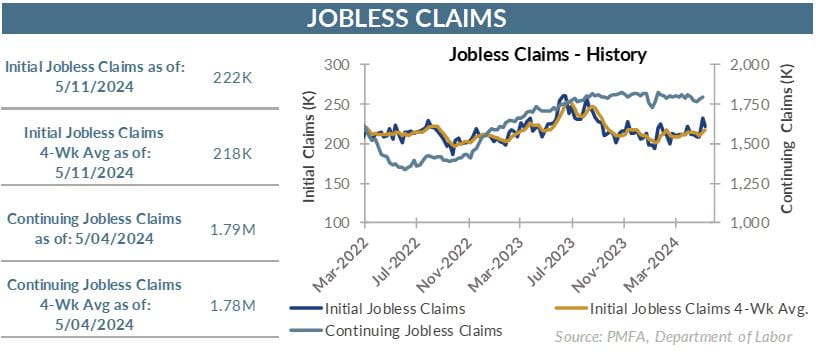

First-time claims for unemployment benefits eased last week, calming any concerns that the prior week’s surge might be a signal of a more sustained increase in layoffs. Claims fell to 222,000 for the week ended May 11 — a decline of 10,000 from the prior week’s revised level of 232,000, a single-week total that was the highest since August 2023.

Although the level of claims has bounced around a bit in the past few months, they remain in a range comparable to a year ago. Job creation has slowed, and the unemployment rate has risen by 0.5% to 3.9% over that period, but the pace of job losses week to week hasn’t meaningfully budged.

Unlike initial claims, continuing claims have increased over the past year from about 1.6 million to nearly 1.7 million. Still, within the context of the overall state of the economy and the labor force, that’s not a meaningful gain; the rate of insured unemployed individuals remains unchanged at 1.2% from a year ago.

The overall narrative on labor conditions remains solid and more consistent with what could be expected given potential growth for the economy. Coming off the boil of the last few years, the economic expansion is still chugging along, but at a pace that’s more consistent with the pre-pandemic period than the explosive growth that accompanied the country’s reopening as COVID-19 era restrictions were lifted.

That’s not to suggest that all is rosy and a definitive “all-clear” can be lifted on recession risk. Most measures of the economy have cooled to varying degrees since last year. The question is whether the economy can comfortably downshift to a more sustainable pace of growth without stalling.

Optimism about the soft-landing (or even no-landing) narrative blossomed since last fall when the Fed’s tone shifted from the need to tighten to the potential for rate cuts. Thus far, the lower-inflation, lower-interest rate, soft-landing theme has paid off for investors given the prevalent risk-on mood.

Yesterday’s data on consumer inflation provided some renewed enthusiasm, but the retail sales data should strike a more cautionary tone. Consumption — a key prop under growth — has shown signs of fading, as households have exhausted much of their previously accumulated cash stockpile and wage growth is edging lower.

Even so, the primary focal point for investors remains the Fed, and any signs of lower inflation reignites anticipation for lower interest rates on the horizon. Through that lens, the April inflation data easily trumped weak retail sector results yesterday.

The bottom line? Labor conditions have eased, but that’s largely been a positive, restoring a better balance between labor demand and the availability of workers. The recent volatility in jobless claims looks more like a blip than a trend.

Data sources for peer group comparisons, returns, and standard statistical data are provided by the sources referenced and are based on data obtained from recognized statistical services or other sources believed to be reliable. However, some or all of the information has not been verified prior to the analysis, and we do not make any representations as to its accuracy or completeness. Any analysis nonfactual in nature constitutes only current opinions, which are subject to change. Benchmarks or indices are included for information purposes only to reflect the current market environment; no index is a directly tradable investment. There may be instances when consultant opinions regarding any fundamental or quantitative analysis may not agree.

Plante Moran Financial Advisors (PMFA) publishes this update to convey general information about market conditions and not for the purpose of providing investment advice. Investment in any of the companies or sectors mentioned herein may not be appropriate for you. You should consult a representative from PMFA for investment advice regarding your own situation.